Budgetary Control

Budget, Budgeting, and Budgetary Control

Budget

A budget is a plan, expressed in monetary or quantitative terms, relating to a definite future period. It's a formal expression of expected incomes and expenditures for a specific timeframe. The Chartered Institute of Management Accountants (CIMA) defines a budget as:

A financial and quantitative statement, prepared prior to a defined period of time, of the policy to be pursued during that period for the purpose of attaining a given objective.

Key Characteristics of a Budget:

-

Planning and Control: A budget serves as a planning device and provides a basis for performance evaluation and control. It sets targets and allows for comparison of actual results against those targets.

-

Monetary and/or Quantitative Terms: Budgets can be prepared in monetary terms (e.g., rupees, dollars), quantitative terms (e.g., units produced, hours worked), or both. This allows for a comprehensive view of the organization's planned activities.

-

Definite Future Period: Budgets are always prepared for a specific future period, such as a month, quarter, year, or even longer term. This timeframe provides a framework for planning and control.

-

Policy Implementation: The primary purpose of a budget is to implement the policies formulated by management to achieve specific organizational objectives. It translates strategic goals into actionable plans.

Budgeting

Budgeting is simply the act of preparing a budget. It's the process of creating the detailed plan that outlines expected income and expenditure.

Budgetary Control

Budgetary control is a system for managing costs through the preparation and use of budgets. It's a process that helps organizations control their finances and achieve their objectives. A comprehensive definition of a budgetary control system is:

A system of controlling costs which includes the preparation of budgets, coordinating the departments and establishing responsibilities, comparing actual performance with the budgeted and acting upon results to achieve maximum profitability.

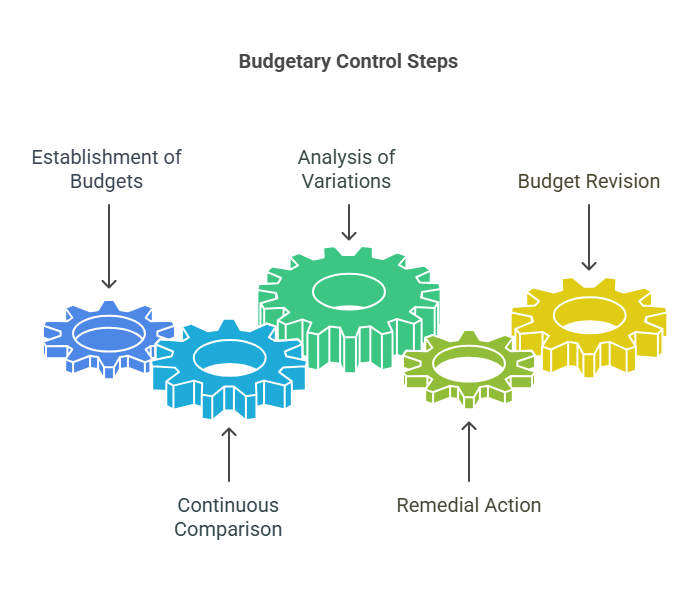

Steps in the Budgetary Control Process:

Steps in the Budgetary Control Process:

-

Establishment of Budgets: Budgets are created for each department or function within the organization. These budgets outline the planned activities and resource allocation for each area.

-

Continuous Comparison: Actual performance is regularly compared against the budget. This ongoing comparison helps identify any deviations from the plan.

-

Analysis of Variations: Any variations between actual and budgeted performance are analyzed to determine the underlying reasons. This analysis is crucial for understanding why performance differed from the plan.

-

Remedial Action: Based on the analysis of variations, appropriate remedial action is taken. This might involve adjusting spending, revising production schedules, or taking other steps to bring performance back in line with the budget.

-

Budget Revision: Budgets are not static documents. They should be reviewed and revised periodically to reflect changes in the business environment, market conditions, or organizational goals. This ensures that the budget remains a relevant and useful tool for planning and control.