Cost Concepts

Basics of Costs

What is Cost?

Cost is the monetary value of resources sacrificed or to be sacrificed for goods and services that are expected to bring current or future benefits/value to a firm. Essentially, it's the price we pay to create value.

Key characteristics of cost:

- Monetary Value: Cost is ultimately measurable in monetary terms.

- Sacrifice: A sacrifice of resources must occur for something to be considered a cost.

- Benefit-Oriented: Costs are incurred with the objective of obtaining a benefit.

- Measurable: Although some costs might be implicit, they should be ultimately measurable.

- Cash or Non-Cash: Costs can involve actual cash outlays or represent non-cash expenses like depreciation.

- Explicit or Implicit: Costs can be explicit (direct, out-of-pocket expenses) or implicit (opportunity costs).

- Context-Dependent: The "cost" of something can vary depending on the purpose for which it's being measured.

A cost is a resource sacrificed or forgone to achieve a specific objective. It's often measured by the monetary amount paid to acquire goods or services. Even costs without a direct cash outlay are considered, especially in decision-making.

Cost is the amount expensed or sacrificed in relation to a specific Cost Object (the item or activity for which the cost is being measured).

Deferred Costs (Assets)

A cost, when incurred, can be either a deferred cost (asset) or an expired cost (expense). Deferred costs are unexpired costs that provide benefits in future periods. They are capitalized as assets on the balance sheet.

- Examples: Plant, equipment, inventory, prepaid rent.

When deferred costs lose their usefulness, they are treated as expenses and written off on the income statement.

Expenses (Expired Costs)

Expenses are expired costs. They represent the costs of resources used up in generating revenue. Expenses are shown on the income statement.

- Examples: Cost of goods sold, selling and distribution expenses.

Losses

A loss is a lost cost, meaning a cost that expires without providing any corresponding benefit. Losses are offset against revenue in the period they occur.

- Examples: Loss on the sale of a fixed asset, loss of stock due to fire.

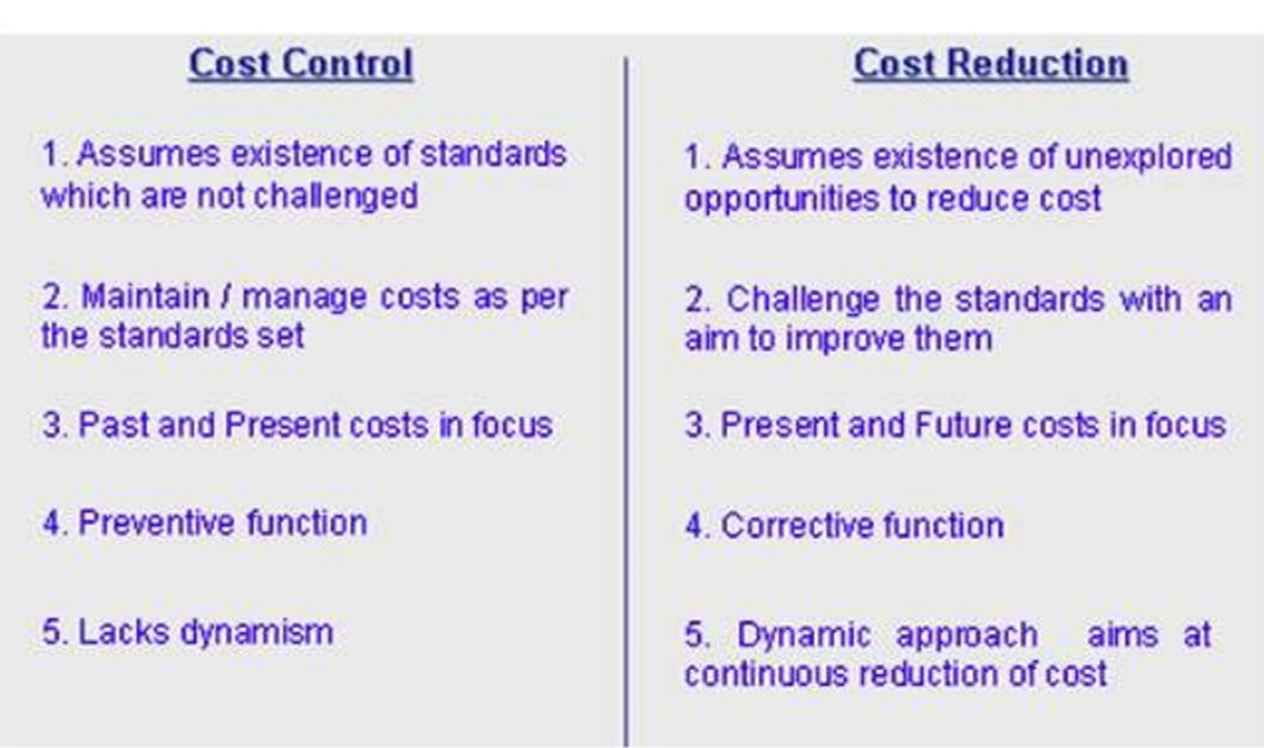

Cost Control and Cost Reduction

Cost control and cost reduction are two distinct but related aspects of cost management. While both aim to optimize costs, they differ in their approach and objectives.

Cost Control

- Definition: Cost control is the regulation of costs by executive action. It involves keeping costs within pre-established limits or standards.

- Process: It's achieved by comparing actual costs with predetermined standard costs or budgets. Differences (variances) are analyzed, and corrective actions are taken to bring costs back in line with the plan.

- Focus: Primarily concerned with preventing costs from exceeding planned levels.

-

Techniques: Common techniques include:

- Inventory Control

- Budgetary Control

- Variance Analysis

Cost Reduction

- Definition: Cost reduction is a continuous and systematic process of achieving real and permanent reductions in the unit cost of goods manufactured or services rendered without impairing their suitability for the intended use.

- Process: It involves actively seeking ways to improve products, methods, procedures, and organizational practices to reduce costs.

- Focus: Aims at permanently lowering costs, not just maintaining them within a target.

Achieving Cost Reduction: The REMI Framework

Cost reduction can be effectively pursued using the REMI framework:

- Reduction: Focus on decreasing resource consumption in areas like production time, waiting time, and inventory levels. Streamlining processes to minimize delays and improve flow.

- Elimination: Identify and remove wasteful activities, bottlenecks, and unnecessary barriers in the production or service delivery process. This might involve process re-engineering or simplifying workflows.

- Modification: Improve existing systems and designs to enhance efficiency and reduce costs. This could involve changes to product design, process layout, or information systems.

- Innovation: Implement new and innovative approaches to production, equipment, tooling, or methods. This could involve adopting new technologies, automating processes, or developing entirely new ways of doing things.

Comparison