Overheads

CostAssignment Unitof Direct and CostIndirect Centre

Costs

-

InDirect Costs: Costs that can be specifically and exclusively identified with a given costaccounting,object.understandingTheythecanconceptsbeofaccurately traced to costunitsobjects.andExample: Direct materials used in producing a specific product. -

Indirect Costs: Costs that cannot be directly traced to a cost

centersobject.isTheycrucialareforassignedaccurateto costtracking,objectsanalysis, and control.Cost UnitA cost unit is a measure of quantity of product or service output. It represents the unit of measurement for which costs are collected and expressed. It's the basis for conveniently allocating expenditure. The selection ofusing an appropriatecostbasis.unitExample:depends on the natureRent of theindustryfactoryandbuilding,thewhichtypebenefitsofmultipleproductproducts.or

Overheads

-

Definition:

TheOverheadsquantityareuponthewhichaggregateexpenditureofcanindirect material costs, indirect labor costs, and indirect expenses that cannot be convenientlyallocated.identified with and directly allocated to a particular cost center or cost object. They are also often called "indirect costs" or "burden." -

Examples:

TextileDepreciationMills:onperfactoryyardbuilding- Salary of

clothstoresmanufacturedsupervisor TransportRentCompanies:ofper passenger-kilometer (passenger-km)factorySteelUtilitiesMills:forperthetonne of steel madeElectricity Companies: per kilowatt-hour (kWh) of electricity generatedCement Industry: per ton of cementHotel: per room-nightHospital: per patient-dayfactory

or meter

Stages of Overhead Distribution (Traditional Cost Accounting)

The traditional cost unitaccounting allows businessesapproach to expressoverhead costsdistribution ininvolves relationthree main stages:

Step 1: Collection and Classification of Overheads

Step 2: Departmentalization of Overheads

This stage involves assigning overheads to a specific, measurable output. This is essential for calculating unit costs, pricing decisions, and performance evaluation.

Cost Centre

A cost centre is a segment or department within an organization for which costs are collected and assigned. Managers ofdifferent cost centers are held accountable for the costs incurred within their respective centers but are not responsible for generating revenue. The focus is on cost control.(departments).

-

Definition:Allocation:AChargingsegmentthe full amount ofanoverheadsorganization for which managersthat areresponsibledirectlyfortraceable to a particular costcontrolcenter.butExample:notDepreciationrevenueofgeneration.a machine used only in the machining department is allocated to that department. -

Examples:Apportionment:- Distributing

Productionoverheads that are common to multiple cost centers on some equitable basis. Example: Factory rent is apportioned to production and service departments(e.g.,basedmachiningondepartment,floorassemblyareadepartment)Service departments (e.g., maintenance department, IT department)Support functions (e.g., human resources, accounting)

CostStep centers3: areAbsorption establishedof toOverheads

Step cost1: managementCollection and control.Classification Byof assigningOverheads

The forfirst costsstep toin specificoverhead managers,distribution organizationsis canthe improve accountabilitycollection and encourageclassification costof efficiency. Performance in cost centers is evaluated by comparing budgeted costs with actualoverhead costs. This varianceinvolves analysisgathering helpsall identify areas whereindirect costs are exceeding targets and allowscategorizing forthem correctivebased action.

Keydifferent Differencescriteria. Summarized

This Understanding both cost units and cost centersclassification is crucial for effective cost management.management Costand allocation.

Overheads are classified according to several key dimensions:

1. Classification by Nature

This classification categorizes overheads based on the type of cost:

-

Indirect Materials: These are materials used in the production process but are not directly part of the finished product. Examples include lubricants, cleaning supplies, and small tools. While necessary for production, they are difficult or impractical to trace to individual units

provideof output. -

Indirect Labor: This refers to the wages and salaries paid to employees who support the production process but are not directly involved in manufacturing the final product. Examples include salaries of supervisors, maintenance staff, and janitors. Their efforts contribute to production but are not directly tied to specific products.

-

Indirect Expenses: These are all other indirect costs that are not materials or labor. Examples include factory rent, utilities (electricity, gas, water), depreciation of factory equipment, property taxes on the factory, and insurance for the factory. These expenses are necessary for the factory to operate but are not directly linked to individual products.

2. Classification by Controllability

This classification distinguishes overheads based on the level of managerial influence:

-

Controllable Overheads: These are overhead costs that a

basisspecificformanagermeasuringcan influence within a given time period. The manager has the authority to make decisions that impact these costs. For example, a production manager might have control over spending on certain supplies or overtime within their department. -

Uncontrollable Overheads: These are overhead costs that a specific manager cannot influence within a given time period. These costs are often determined by higher levels of management or external factors. For example, a production manager may not have control over the rent of the factory building or the depreciation of equipment, as these are often decided at a higher level.

3. Classification by Variability

This classification categorizes overheads based on how they behave in relation to changes in production volume or activity level:

-

Fixed Overheads: These overhead costs remain constant in total, regardless of changes in production or activity levels within a relevant range. Examples include rent, property taxes, and

allocatingsalariescostsoftoadministrativeproductsstaff. The total fixed overhead cost stays the same even if production increases orservices,decreaseswhile cost centers provide a framework for controlling and managing costs(within theorganization.relevantTherange).information -

fromVariable

trackingOverheads: These overhead costsbychangeunitinanddirectcenterproportionisto changes in production or activity levels. Examples include indirect materials, some utilities costs (like electricity used fordecision-making, performance evaluation,machines), and supplies. As production increases, the total variable overhead costcontrol.also increases proportionally. -

Semi-Variable Overheads: These overhead costs have both a fixed and a variable component. They change with production or activity levels, but not in direct proportion. A portion of the cost is fixed, while the other portion varies. An example might be a telephone bill that includes a fixed monthly charge plus charges based on usage.

4. Classification by Function

This classification categorizes overheads based on the functional area of the business:

-

Factory Overheads (Manufacturing Overheads): These are all indirect costs associated with the manufacturing process. Examples include indirect materials, indirect labor, factory rent, utilities for the factory, depreciation of factory equipment, and maintenance of factory buildings.

-

Office and Administrative Overheads: These are indirect costs related to the general administration of the business. Examples include salaries of administrative staff, office rent, office supplies, depreciation of office equipment, and accounting and legal fees.

-

Selling and Distribution Overheads: These are indirect costs associated with marketing, selling, and distributing the products. Examples include advertising expenses, sales commissions, shipping costs, warehouse rent, and salaries of sales staff.

Grouping of Overheads

After overheads are classified, all items within each functional category (factory, administrative, selling) are grouped together. This grouping creates cost pools for each function, which are then used for further allocation and absorption. This step prepares the overhead costs for the next stages of overhead distribution.

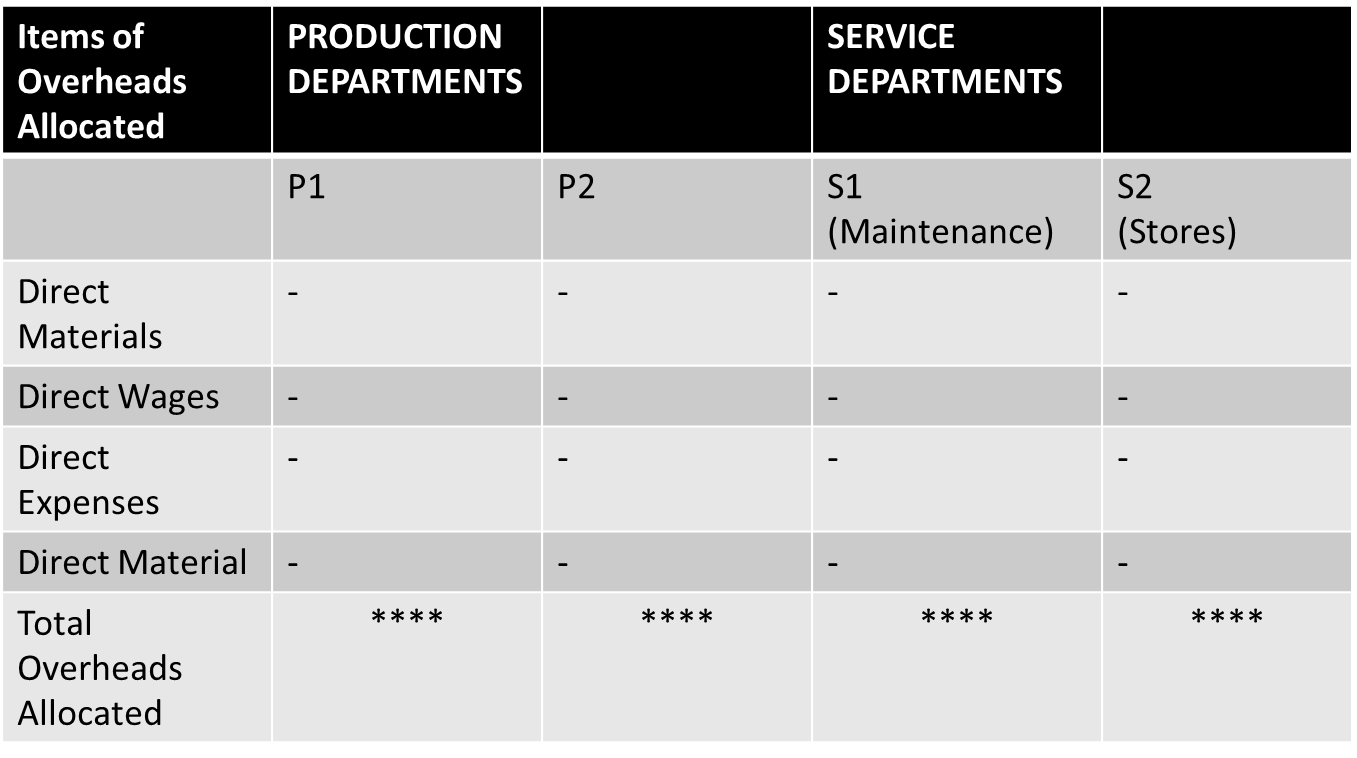

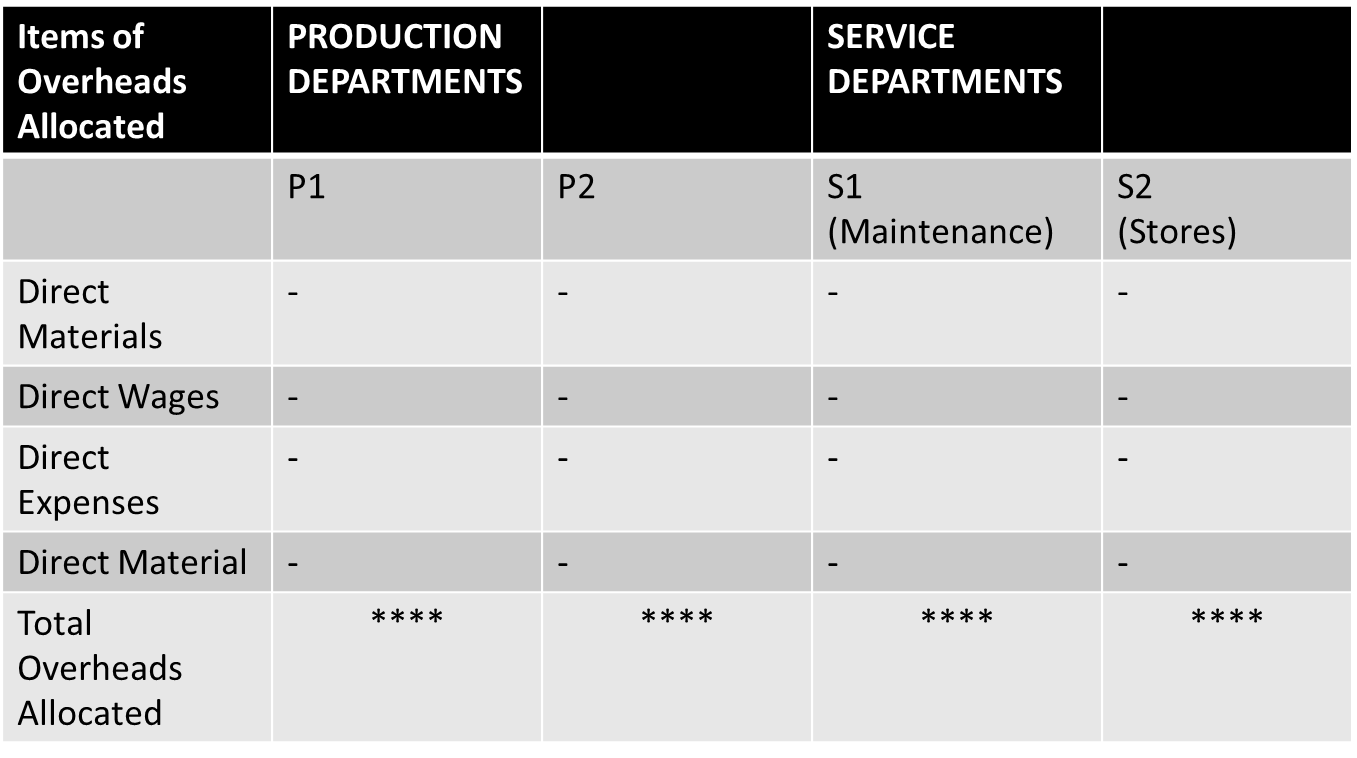

Step 2: Departmentalization of Factory Overheads (Detailed Breakdown)

Departmentalization of factory overheads involves two steps:

-

Step 1: Primary Distribution: Allocation and apportionment of factory overheads to both production departments (directly involved in manufacturing) and service departments (support the production departments). This is the initial assignment of overheads.

-

Allocation: Overheads directly traceable to a department are allocated to that department.

-

Apportionment: Overheads common to multiple departments are apportioned based on suitable bases.

-

-

Step 2: Secondary Distribution: Apportionment of the service departments' overheads to the production departments. This recognizes that service departments provide services to production departments, and their costs should be ultimately borne by the products.

-

Service department overheads are apportioned to production departments based on the services provided. Several methods exist for secondary distribution, including the direct method, the step-down method, and the reciprocal method.

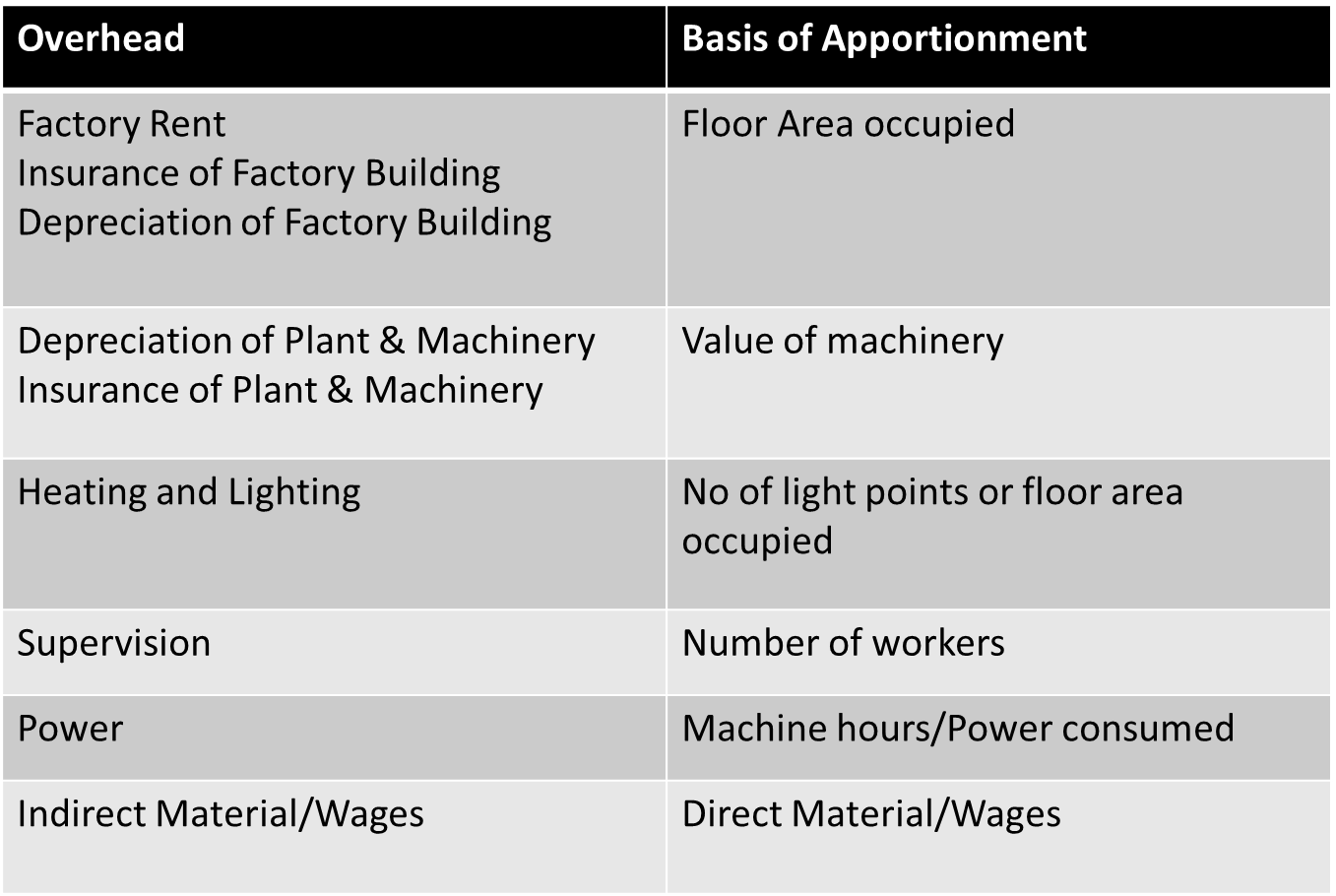

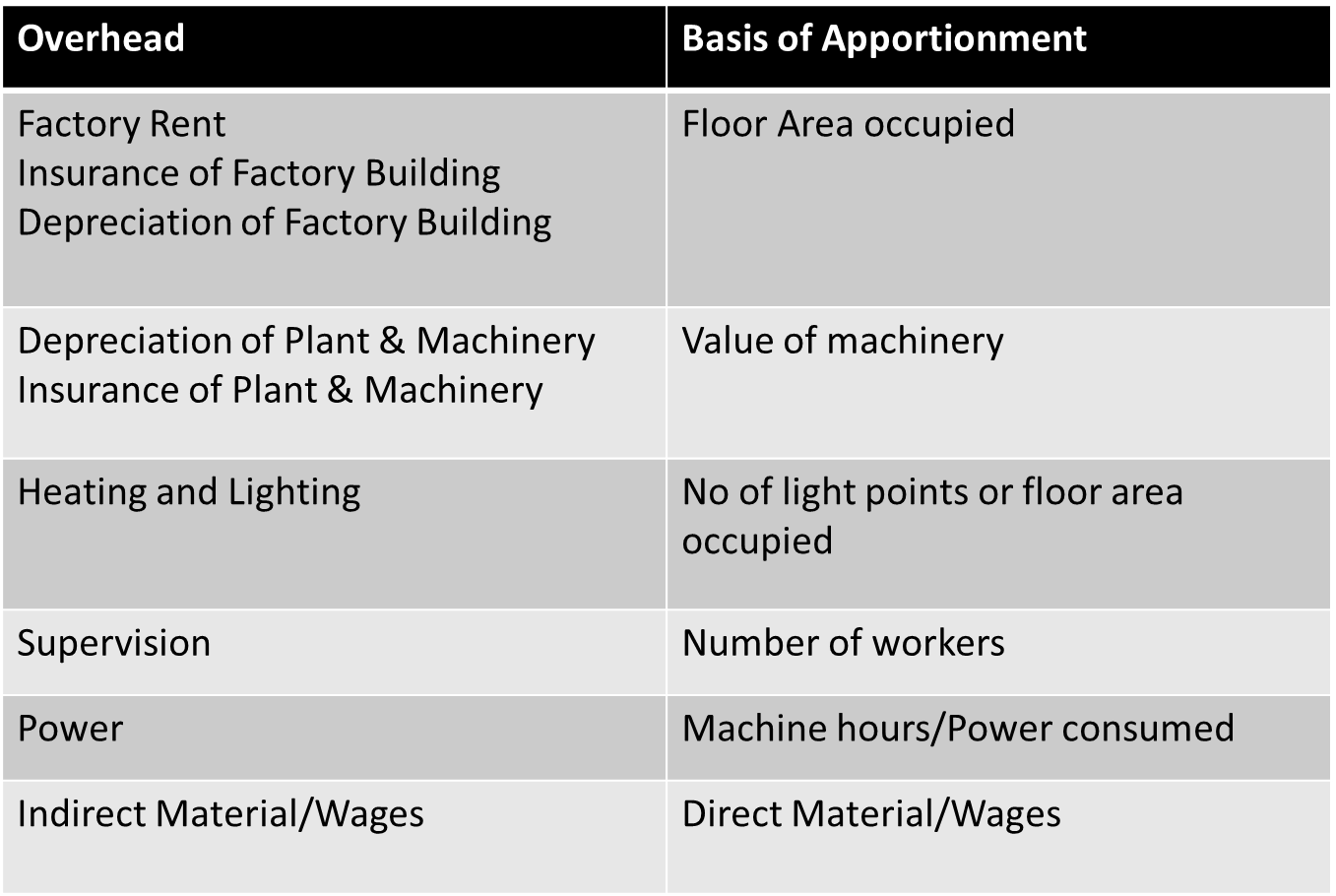

Bases of Apportionment of Overheads

Several bases are used to apportion overheads, depending on the nature of the cost:

- Direct Labor Hours: Used for costs like supervisor salaries, R&D, etc.

- Number of Workers: Used for welfare expenses, canteen expenses, etc.

- Relative Areas of Departments: Used for rent, lighting and heating, building repairs, etc.

- Machine Hour Rate: Used for power, machine repairs and maintenance, depreciation on machinery, etc.

- Asset Value: Used for insurance on buildings, depreciation on buildings, etc.

- Light Points: Used for lighting expenses.

- Direct Wages: Used for PF contribution, insurance premiums, etc.

- Technical Estimates: Used when no other basis is suitable; experts provide estimates (e.g., for works manager's salary, internal transport, steam, water).