Target Costing

Pricing Strategies: Cost-Based vs. Market-Based (Target Costing)

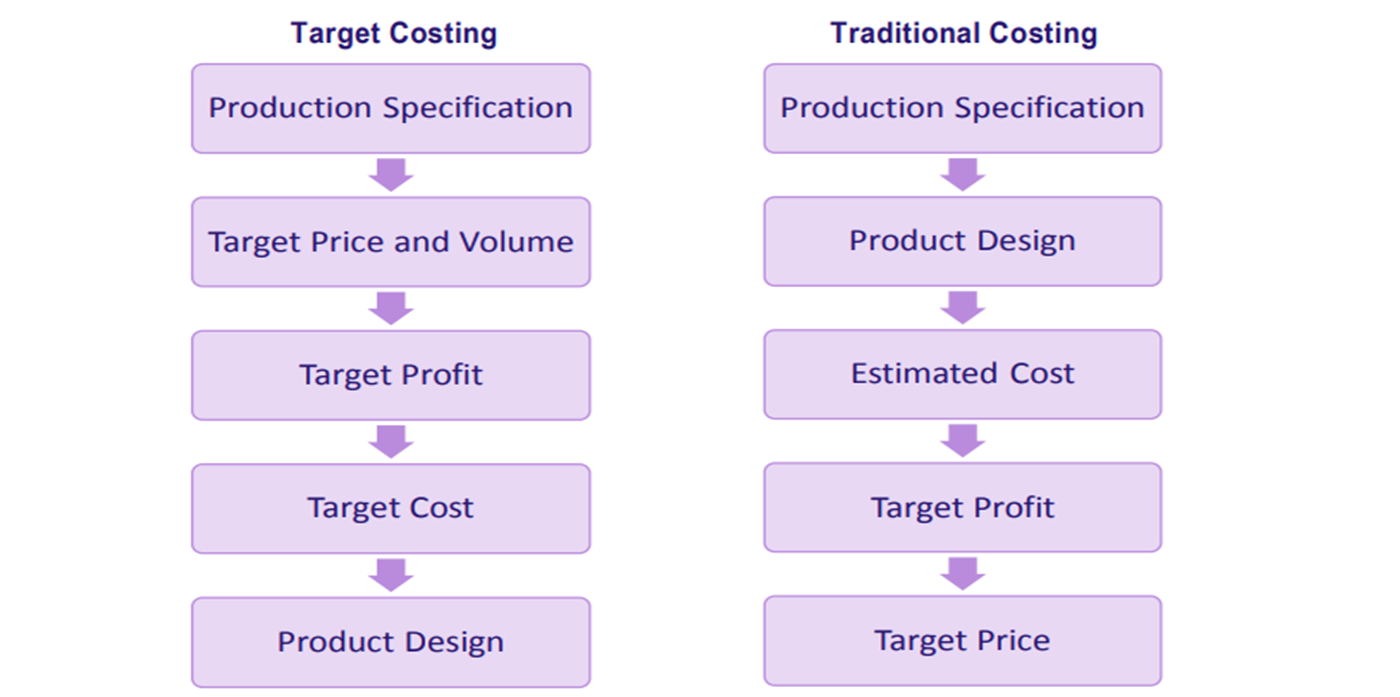

Pricing is a critical aspect of business strategy, and there are two primary approaches: cost-based pricing and market-based pricing. Understanding the differences between these approaches is crucial for effective decision-making.

1. Cost-Based Pricing (Cost-Plus Pricing)

Cost-based pricing is a traditional approach where companies calculate the total cost of producing a product or service and then add a desired profit margin to arrive at the selling price. This method focuses internally, starting with costs and then considering the market. If the calculated selling price is too high for the market, companies may attempt to reduce costs to maintain the desired profit margin.

2. Market-Based Pricing (Target Costing)

Market-based pricing, particularly target costing, takes a different approach. Companies first determine a target price based on market research, competitor analysis, and customer willingness to pay. Then, they deduct the desired profit margin from the target price to arrive at the target cost. This method is externally focused, starting with the market and then working backward to determine the acceptable cost.

Target Costing in Detail

CIMA defines target cost as "a product cost estimate derived from a competitive market price." Originating in Japan in the late 1960s, target costing is credited with contributing to the competitiveness of Japanese companies in the 1980s.

Sakurai (1989) describes target costing as "a cost management tool for reducing the overall cost of a product over its entire life cycle with the help of production, engineering, R&D, marketing, and accounting departments."

Target costing is a structured approach to product development. It involves:

- Understanding Customer Requirements: Thorough market research to identify customer needs and preferences.

- Analyzing Competitor Reactions: Predicting how competitors might respond to a new product or pricing strategy.

- Value Engineering: Focusing on product design and development to achieve the target cost while maintaining quality and meeting market requirements.

Example: Tata Nano

The Tata Nano is a prime example of successful target costing in India. Ratan Tata set a target price of around Rs. One Lakh to create an affordable car for Indian families. Tata Motors achieved this ambitious goal through:

- Understanding target customer needs.

- Innovation in product design.

- Distributed manufacturing and assembly.

- Collaboration with suppliers and vendors.

The Tata Nano demonstrates how target costing can help companies deliver innovative products at competitive prices while fulfilling a vision. It highlights the importance of understanding customer needs, market dynamics, and the power of cross-functional collaboration to achieve cost targets without compromising quality.

Components of a Target Costing System: Value Analysis and Value Engineering

A robust target costing system relies on several key components working together. Two crucial elements are Value Analysis and Value Engineering. While related, they are applied at different stages of the product lifecycle.

1. Value Analysis

Value analysis is a planned, scientific approach to cost reduction. It's applied to existing products and focuses on reviewing the product's material composition and production design. The goal is to identify modifications and improvements that reduce costs without diminishing the product's value to the customer or user.

- Example: Value analysis might examine the materials used in a chair. Could a less expensive but equally durable wood be used? Could the design be slightly modified to reduce the amount of material needed without affecting the chair's strength or comfort?

2. Value Engineering

Value engineering, on the other hand, is the application of value analysis principles to new products before they are produced. It's a proactive approach focused on cost avoidance or cost reduction during the design and development phase. Value engineering is closely linked to target costing because it's the primary mechanism for achieving the target cost.

- Example: During the design of a new car, value engineering might explore different engine designs to find one that meets performance requirements while minimizing manufacturing costs. It might also examine different materials for the car's body to find the best balance of cost, weight, and durability.

Implementing Target Costing: A Step-by-Step Guide

Target costing is a powerful cost management technique that aligns product development with market demands and profitability. Here's a breakdown of the key steps involved in implementing target costing:

1. Market Research and Selecting a Target Price

The foundation of target costing is a deep understanding of the market. This involves:

- Identifying Valued Features: Determining which product features are most important to customers.

- Assessing Willingness to Pay: Understanding how much customers are willing to pay for the desired features.

- Analyzing Competition: Studying competitor products, pricing strategies, and market share.

- Estimating Demand: Forecasting the potential market size and demand for the product.

This comprehensive market analysis informs the finalization of product specifications and design. Crucially, it also provides the basis for determining the target selling price. This price must be competitive and attractive to the target market segment.

2. Determine Target Cost per Unit

Once the target selling price is established, the next step is to calculate the target cost per unit. This is done by subtracting the desired target profit per unit from the target selling price.

Target Cost per Unit = Target Selling Price per Unit - Target Profit per Unit

The target cost represents the maximum cost that can be incurred to produce the product while achieving the desired profit margin. It must be a realistic and achievable figure that considers all costs the firm must recover to maintain long-term profitability.

3. Attain Target Cost through Value Engineering

The most challenging step is achieving the target cost. This is accomplished through value engineering, a systematic and collaborative process involving a cross-functional team of experts. Value engineering aims to identify opportunities to reduce costs without compromising the product's essential functionality or value to the customer.

Benefits and Limitations of Target Costing

Target costing, while a powerful tool, has both advantages and disadvantages. Understanding these is crucial for successful implementation.

Benefits of Target Costing

-

Cost Minimization: Target costing focuses on determining the maximum allowable cost for a product and then strives to meet that cost throughout the value chain. This proactive approach helps eliminate defects, waste, and costly revisions after production, leading to significant cost reductions.

-

Market Orientation: Unlike cost-plus pricing, target costing is driven by market demands, not internal capabilities. It begins with thorough market research to understand customer needs, define product features, and determine the price customers are willing to pay. This market-centric approach ensures that products are designed to meet customer expectations and stay competitive.

-

Profitability: By actively focusing on both costs and prices simultaneously, target costing contributes to improved profitability. It ensures that products are designed and manufactured at a cost that allows for the desired profit margin at the target selling price.

-

Innovation: The constant search for alternative ways to achieve the target cost often sparks innovation. This can lead to product differentiation, process improvements, and a stronger competitive edge for the company.

Limitations of Target Costing

-

Burden on Employees: The pressure to continuously reduce costs can place a significant burden on employees. If targets are unrealistic or the implementation is poorly managed, employees may feel overworked and demotivated. Furthermore, penalties for failing to meet targets can create a negative work environment.

-

Organizational Conflicts: While target costing involves all departments, the manufacturing department often bears the brunt of the cost reduction efforts. This can lead to organizational conflicts and resentment. Coordination challenges may also arise when multiple experts are involved in value engineering teams.

-

Compromise on Quality: In the pursuit of cost reduction, there's a risk that managers may resort to using cheaper substitutes or cutting corners, which can negatively impact product quality. This can damage the company's reputation and lead to customer dissatisfaction in the long run.

-

Inaccurate Estimations: The entire target costing process hinges on the accuracy of the target price. If the target price is not estimated accurately (due to flawed market research, unforeseen competition, or changing market conditions), the entire project can fail. An inaccurate target price can lead to either an uncompetitive product or one that cannot be produced profitably at the target cost.

Addressing the Limitations

To mitigate the limitations of target costing, the following measures are essential:

-

Strong Leadership and Employee Participation: Effective implementation of target costing requires strong leadership support from top management and active participation from employees at all levels. This fosters a sense of ownership and shared responsibility.

-

Team Orientation and Commitment: Cultivating a team-oriented culture and ensuring employee commitment are crucial. This can be achieved through training, communication, and incentives that align individual and team goals with the overall target costing objectives.

-

Realistic Performance Standards: Setting realistic and achievable performance standards is essential to avoid overburdening employees and creating unnecessary stress. Targets should be challenging but attainable.

-

Specific Cost Goals for Departments: Instead of setting only an overall cost goal for the entire team, it's more effective to establish specific cost goals for each department. This clarifies responsibilities and allows for more focused cost management efforts. This also reduces the feeling that one department (typically Manufacturing) is solely responsible for cost reduction.

By addressing these limitations and implementing target costing thoughtfully, organizations can reap the benefits of this powerful cost management technique while minimizing its potential drawbacks.