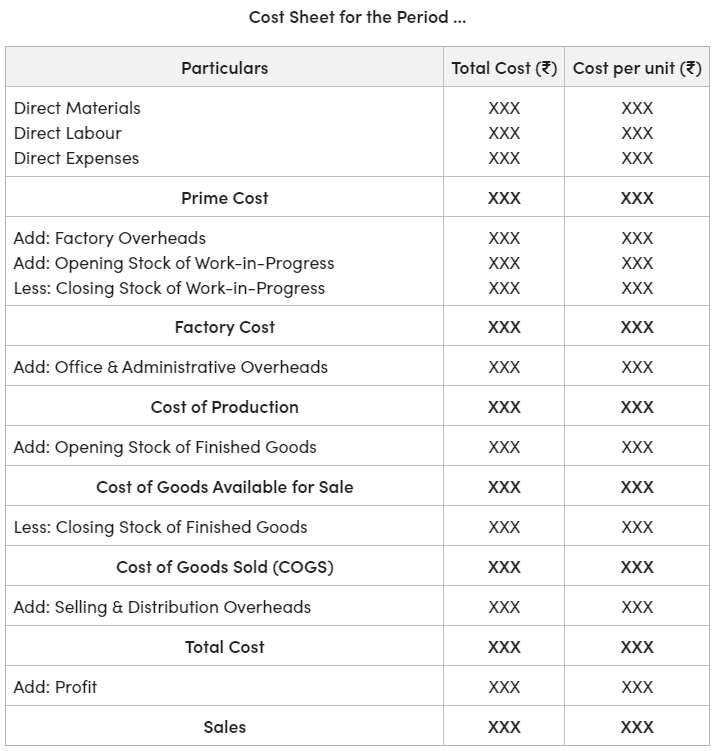

Total Cost and Cost Sheet

Total Cost Calculation

Inventory Adjustments

Several adjustments are made for changes in inventory levels at various stages of the production and sales process:

-

Direct Material Consumed:

- Direct Material Consumed = Opening Stock of Direct Material + Purchases of Direct Material - Closing Stock of Direct Material

-

Work in Progress (WIP): WIP represents partially completed goods. The change in WIP affects the calculation of the works cost.

- Works Cost = Gross Works Cost + Opening Work in Progress –Closing work in progress

- Finished Goods: Finished goods inventory represents completed products ready for sale. The change in finished goods inventory affects the cost of goods sold.

-

Cost of Production = Works Cost + Office & Admn Overheads

-

Cost of Production of Goods sold = Cost of Production + Opening stock of Finished goods – Closing Stock of Finished goods

-

Cost of Production of Goods sold + S&D exp = Cost of sales

Proforma Cost Sheet Explained

A proforma cost sheet is a structured statement that summarizes the various cost elements involved in producing and selling goods or services. It presents a logical flow of costs, starting from direct materials and culminating in the cost of sales. Here's a breakdown of the proforma cost sheet and its components:

Proforma Cost Sheet Structure

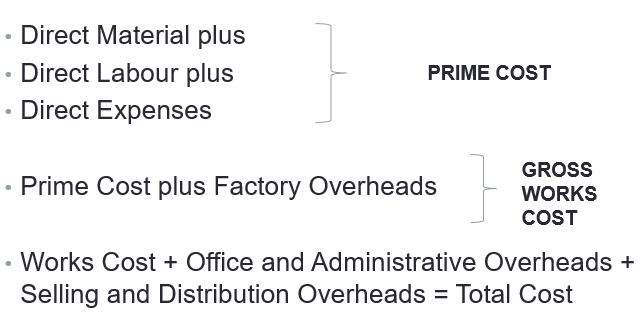

Direct Materials: Opening Stock of Raw Materials(+) Purchases of Raw Materials (-) Closing Stock of Raw Materials = Material Consumed

(+) Direct Labour

(+) Direct Expenses

= Prime Cost

Prime Cost (+) Factory Overheads

= Gross Factory Cost

Gross Factory Cost

(+) Opening Stock of Work-in-Progress (WIP)

(-) Closing Stock of Work-in-Progress (WIP)

= Factory Cost or Works Cost

Factory Cost or Works Cost(+) Office & Administrative Overheads

= Total Cost of Production

Total Cost of Production

(+) Opening Stock of Finished Goods

(-) Closing Stock of Finished Goods

= Cost of Production of Goods Sold (COGS)

Cost of Production of Goods Sold (COGS)(+) Selling and Distribution Overheads

= TotalCost Costof sales

TotalCost costof (sales(Compare with Sales Revenue to obtain Profit/Loss)

Explanation of Cost Elements

-

Direct Materials: The cost of raw materials consumed during the production process. The calculation adjusts for changes in raw materials inventory.

-

Direct Labour: Wages paid to workers directly involved in converting raw materials into finished goods.

-

Direct Expenses: Expenses directly attributable to the production of specific goods or services (e.g., royalties, hire charges for special equipment).

-

Prime Cost: The sum of direct materials, direct labor, and direct expenses. It represents the basic, most direct costs of production.

-

Factory Overheads (Manufacturing Overheads): Indirect costs related to the production process (e.g., factory rent, utilities, depreciation of factory equipment, indirect materials like lubricants, indirect labor like factory supervisor salaries).

-

Gross Factory Cost: The sum of prime cost and factory overheads.

-

Work-in-Progress (WIP): The cost of partially completed goods. Adjustments for opening and closing WIP inventories are made to arrive at the factory or works cost.

-

Factory Cost or Works Cost: The total cost of production within the factory, adjusted for WIP.

-

Office & Administrative Overheads: Indirect costs associated with the general management and administration of the business (e.g., office rent, salaries of administrative staff, office supplies, depreciation of office equipment).

-

Total Cost of Production: The sum of the works cost and office & administrative overheads. It represents the total cost of producing goods, including both manufacturing and administrative costs.

-

Finished Goods: Completed goods ready for sale. Adjustments for opening and closing finished goods inventories are made to calculate the cost of goods sold.

-

Cost of Production of Goods Sold (COGS): The cost of goods that were actually sold during the period.

-

Selling and Distribution Overheads: Indirect costs associated with selling and distributing the finished goods (e.g., advertising, sales commissions, transportation costs, warehouse rent).

-

Cost of Sales: The total cost incurred in producing and selling the goods, including manufacturing, administrative, and selling & distribution costs.

-

Profit/Loss: The difference between sales revenue and the cost of sales.