Concept and Importance of Capital Budgeting

Capital budgeting is a critical financial process that involves evaluating and selecting long-term investments that align with a company’s strategic objectives. These investments may include purchasing machinery, expanding facilities, launching new products, or entering new markets. Since these decisions involve large capital expenditures and impact a company's financial health for years, proper evaluation is necessary.

Concept of Capital Budgeting

Capital budgeting is the process of analyzing potential investment opportunities to determine their profitability and long-term impact on the company. The primary goal is to allocate resources efficiently, ensuring that investments generate positive returns while minimizing financial risks.

Key Features of Capital Budgeting

- Long-Term Perspective – Capital budgeting focuses on investments that will impact a business for several years.

- Large Financial Commitments – Investments require significant capital outlay, often requiring external financing.

- Risk Assessment – Future cash flows and uncertainties must be considered before committing to an investment.

- Impact on Business Growth – Strategic investments determine competitive advantage and operational efficiency.

- Irreversibility – Once made, capital investments are difficult or costly to reverse.

Steps in the Capital Budgeting Process

- Identification of Investment Opportunities – Companies list potential projects requiring capital investments, such as expanding production capacity or adopting new technology.

- Project Evaluation – Different capital budgeting techniques (like Net Present Value (NPV) and Internal Rate of Return (IRR)) are used to assess financial viability.

- Project Selection – The most profitable and strategically beneficial projects are chosen.

- Financing the Investment – Companies determine how to fund the investment through equity, debt, or retained earnings.

- Implementation and Monitoring – Projects are executed, and their performance is tracked to ensure they meet expected financial and operational outcomes.

Importance of Capital Budgeting

Effective capital budgeting is crucial for businesses as it ensures optimal investment of financial resources, minimizes risk, and enhances profitability. Below are the key reasons why capital budgeting is important:

1. Strategic Business Growth and Expansion

- Capital budgeting helps businesses expand operations, enter new markets, and invest in innovative technologies.

- It ensures that resources are allocated to projects that align with the company’s long-term vision and growth strategy.

2. Maximizing Shareholder Wealth

- Capital investments directly impact earnings and stock prices.

- Projects with positive NPV and high IRR contribute to increased shareholder value.

3. Efficient Allocation of Financial Resources

- Businesses have limited capital and must prioritize investments that yield the highest returns.

- Capital budgeting ensures that funds are allocated efficiently to the most profitable projects.

4. Risk Management and Long-Term Stability

- Investing in capital-intensive projects involves long-term financial commitments.

- Capital budgeting evaluates the potential risks and uncertainties associated with each project to minimize losses.

5. Cost Control and Cash Flow Management

- Investments in assets like machinery and infrastructure affect a company’s cost structure and cash flow.

- Capital budgeting ensures that companies invest in projects that generate stable and sufficient cash inflows over time.

6. Competitive Advantage

- Companies that invest wisely in technology, automation, and research & development (R&D) gain a competitive edge.

- Strategic capital investments allow businesses to increase efficiency, reduce production costs, and improve product quality.

Capital Budgeting Techniques

Capital budgeting decisions rely on quantitative financial techniques to evaluate investment options. The most common methods include:

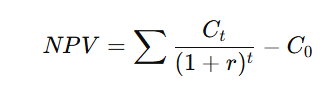

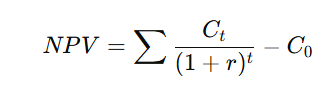

1. Net Present Value (NPV)

- Measures the difference between present cash inflows and outflows.

- A positive NPV means the project is expected to be profitable.

-

Formula:

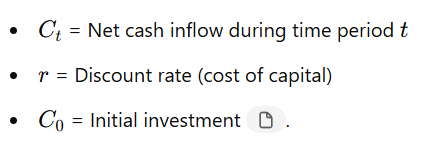

Where:

Where:

-

2. Internal Rate of Return (IRR)

- Determines the discount rate that makes NPV = 0.

- Projects with IRR higher than the required rate of return are considered profitable.

- Helps compare multiple investment options.

3. Payback Period

- Calculates how long it takes to recover the initial investment.

- A shorter payback period indicates a quicker return on investment but does not consider cash flows beyond that period.

4. Profitability Index (PI)

- Measures the ratio of present value of cash inflows to the initial investment.

- PI > 1 indicates a profitable project.

-

Formula:

5. Discounted Payback Period

- Similar to the payback period but accounts for time value of money.

- Ensures that future cash inflows are discounted before determining the break-even point.

Conclusion

- Capital budgeting is a vital financial decision-making process that determines a company’s long-term growth and profitability.

- By using capital budgeting techniques like NPV, IRR, and Payback Period, businesses can efficiently allocate resources, minimize risks, and maximize shareholder value.

- Effective capital budgeting ensures that companies invest in projects that generate sustainable returns, enhance operational efficiency, and secure long-term financial stability.