Introduction to Modelling Volatility

Volatility, a measure of the dispersion of returns for a given security or market index, is a key concept in financial econometrics. It reflects the degree of uncertainty or risk associated with an asset's price movements. High volatility implies that the price can fluctuate dramatically over a short period, while low volatility suggests more stable price behavior.

Importance of Volatility Modeling

Accurate volatility modeling is crucial for various financial applications, including:

-

Risk Management: Volatility is a primary input for Value at Risk (VaR) and Expected Shortfall (ES) calculations, which are used to measure and manage market risk.

-

Option Pricing: Option prices are highly sensitive to volatility. The Black-Scholes model and its extensions rely on volatility estimates to determine fair option prices.

-

Portfolio Optimization: Volatility is a key factor in portfolio construction and asset allocation. Investors often seek to minimize portfolio volatility for a given level of expected return.

-

Trading Strategies: Many trading strategies are based on volatility. For example, volatility arbitrage strategies aim to profit from discrepancies between implied volatility (derived from option prices) and realized volatility (historical volatility).

-

Financial Regulation: Regulatory bodies use volatility models to assess the capital adequacy of financial institutions and to monitor systemic risk.

Challenges in Volatility Modeling

Volatility is not directly observable. It must be estimated from historical data or implied from market prices (e.g., option prices). Several challenges arise in volatility modeling:

-

Time-Varying Volatility: Volatility is not constant over time. It tends to fluctuate, exhibiting periods of high volatility (volatility clustering) and periods of low volatility.

-

Asymmetric Effects: Negative shocks (e.g., bad news) often have a greater impact on volatility than positive shocks (e.g., good news) of the same magnitude. This is known as the leverage effect.

-

Fat Tails: Financial returns often exhibit fat tails, meaning that extreme events occur more frequently than predicted by a normal distribution. This can lead to underestimation of risk if volatility models are based on normality assumptions.

-

Data Frequency: The choice of data frequency (e.g., daily, weekly, monthly) can affect volatility estimates. Higher-frequency data can capture short-term volatility fluctuations but may be more susceptible to noise.

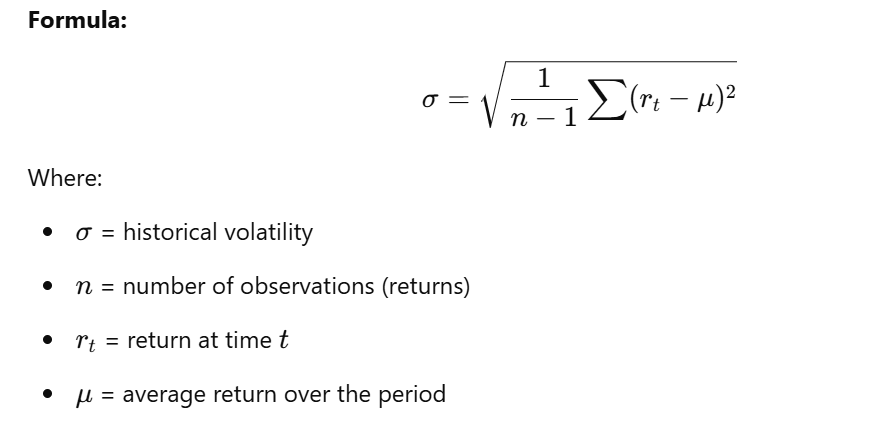

Traditional Volatility Measures

- Historical Volatility: Calculated as the standard deviation of historical returns over a specified period.

Limitations: Assumes volatility is constant over the estimation period, which is often unrealistic.

-

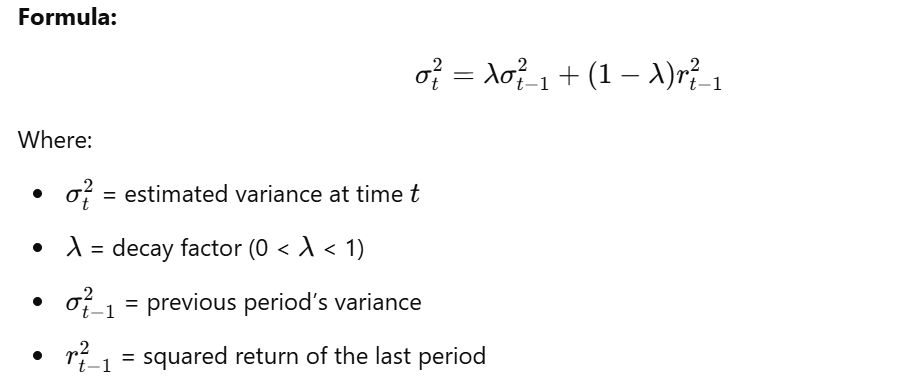

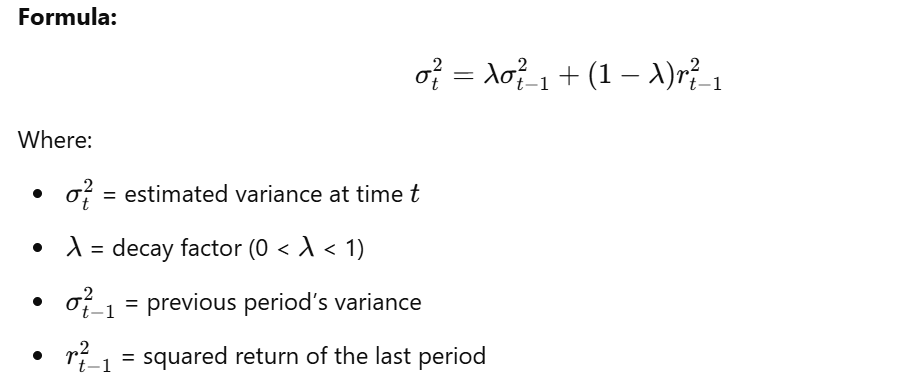

Exponentially Weighted Moving Average (EWMA): Assigns greater weight to more recent observations, allowing volatility to respond more quickly to changing market conditions.

Limitations: Still relatively simple and may not capture all the complexities of volatility dynamics.

Conditional Heteroscedastic Models

Conditional heteroscedastic models provide a more sophisticated approach to volatility modeling by allowing the variance of the returns to depend on past information. These models are particularly well-suited for capturing volatility clustering and other stylized facts of financial returns.

- Heteroscedasticity: Refers to the situation where the variance of the error term in a regression model is not constant.

- Conditional Heteroscedasticity: Refers to the situation where the variance of the error term depends on past values of the error term or other variables.

The most widely used conditional heteroscedastic models are:

- ARCH (Autoregressive Conditional Heteroscedasticity) Models: The variance depends on past squared error terms.

- GARCH (Generalized Autoregressive Conditional Heteroscedasticity) Models: The variance depends on both past squared error terms and past variances.

These models will be discussed in detail in the following sections. They provide a framework for understanding and forecasting volatility, which is essential for managing risk and making informed investment decisions.