Theories of M&A; Process of M&A

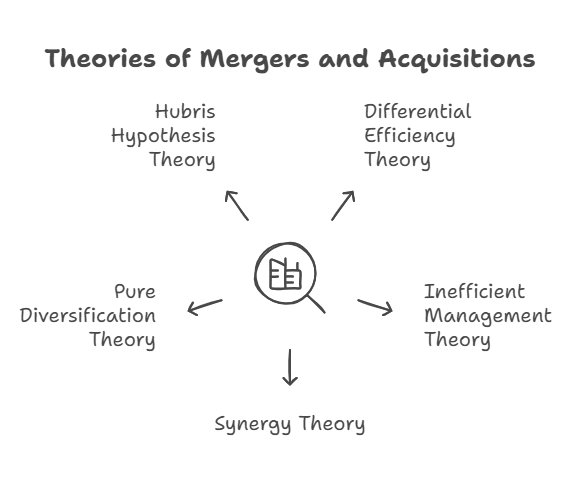

Theories of Mergers and Acquisitions

-

Differential Efficiency Theory: This theory posits that acquisitions happen when a more efficiently managed firm (A) acquires a less efficient firm (B). The idea is that A's superior management practices will improve B's performance, leading to increased overall efficiency. Inefficient firms become targets for more capable ones.

-

Inefficient Management Theory: Similar to the differential efficiency theory, this focuses specifically on management inefficiency. It suggests that poorly managed companies are prime targets for acquisition. The acquirer believes it can unlock greater value by replacing the existing management team.

-

Synergy Theory: Synergy is the core concept where the combined value of two firms is greater than the sum of their individual values ("2+2=5"). This can arise from:

- Operational Synergy: Combining operations, eliminating redundancies, and achieving economies of scale.

- Financial Synergy: Access to cheaper capital, improved cash flow, and tax advantages.

-

Pure Diversification Theory: This theory suggests that companies pursue mergers to diversify their operations. Diversification can reduce risk and open up new markets. Acquiring another company can be a faster route to diversification than internal growth.

-

Hubris Hypothesis Theory: This theory argues that managers sometimes pursue acquisitions for personal reasons (e.g., increased power, prestige) rather than purely financial ones. This is especially true in competitive takeover situations. The "winner's curse" describes how the winning bidder in an auction often overpays due to inflated valuations driven by the desire to win, a form of hubris.

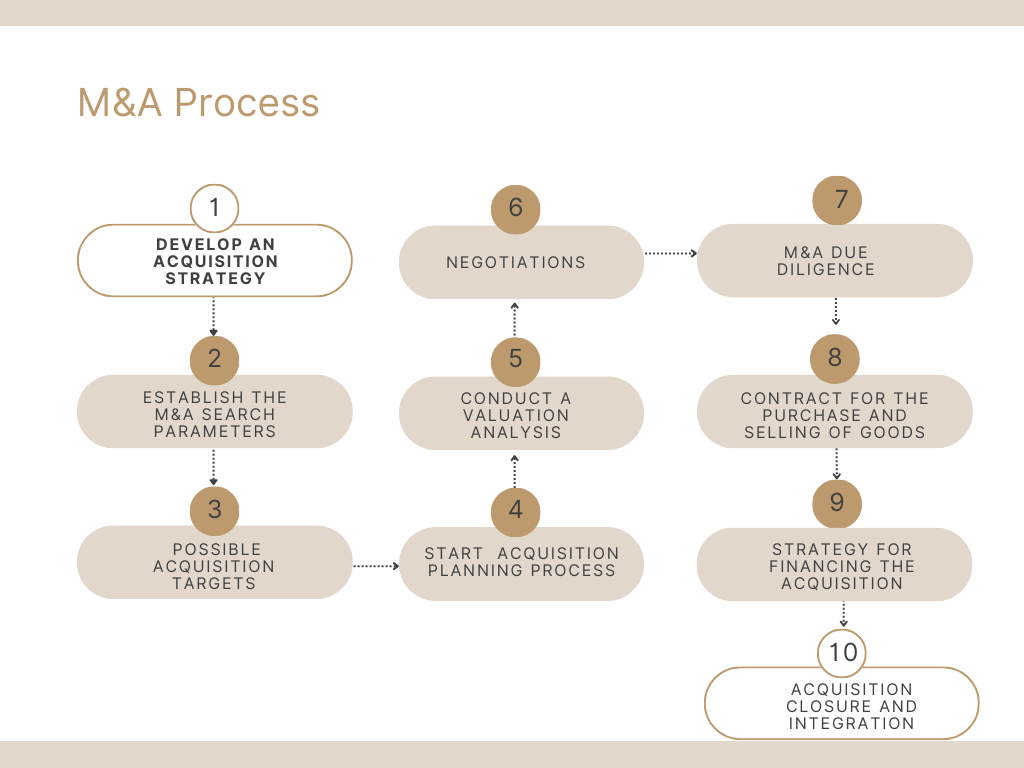

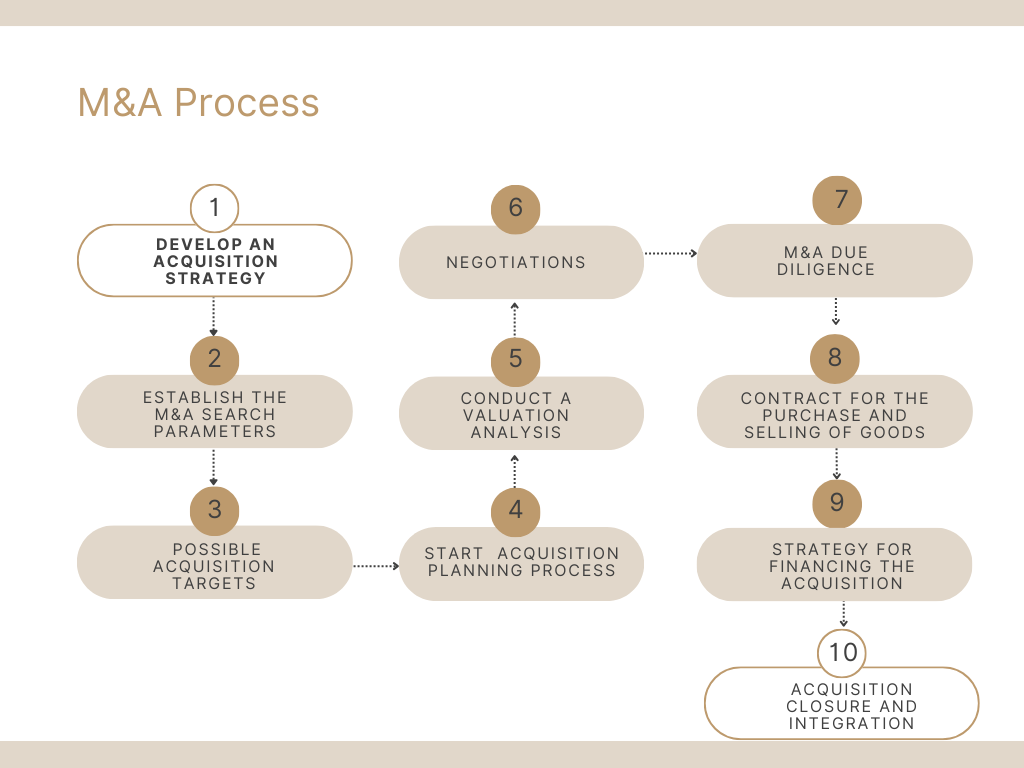

The Merger and Acquisition Process

Develop an Acquisition Strategy:The acquiring company defines its objectives for the M&A transaction. What are they hoping to achieve? (e.g., new products, market access, increased scale). This strategy guides the entire process.Establish M&A Search Parameters:Specific criteria are defined to identify potential target companies. These might include financial metrics (profit margins, revenue), industry, geographic location, customer base, or technological capabilities.Look for possible Acquisition Targets:Based on the defined parameters, the acquirer researches and evaluates potential target companies. This might involve using databases, industry contacts, or investment bankers.Start Acqusition Planning Process:The acquirer contacts promising targets to gauge their interest in a merger or acquisition. Initial discussions explore strategic fit and potential deal terms.Conduct a Valuation Analysis:If the initial discussions are positive, the acquirer requests detailed information from the target company (financial statements, contracts, etc.) to conduct a thorough valuation. This analysis determines a fair price for the target.Negotiations:Based on the valuation, the acquirer makes an initial offer. Negotiations ensue between the two parties to finalize the deal terms, including price, payment method, and other conditions.M&A Due Diligence:A comprehensive investigation of the target company is conducted to verify the information provided and uncover any potential risks or liabilities. This includes financial, legal, operational, and customer due diligence.Contract for the purchase and selling of goods:Assuming due diligence reveals no major issues, a legally binding purchase agreement is drafted and signed. This agreement outlines the terms and conditions of the acquisition, including the type of transaction (asset purchase or stock purchase).Strategy for Financing the Acquisition:The acquirer secures the necessary financing for the acquisition. This could involve a combination of cash, debt, and equity. Financing arrangements are typically finalized around the time the purchase agreement is signed.Acquisition Closure and Integration:The acquisition is finalized (closed), and the integration process begins. This involves combining the operations, systems, and personnel of the two companies to achieve the desired synergies and strategic goals. This is often the most challenging phase of the M&A process.