Investment Evaluation Technique

Non-Discounting Methods

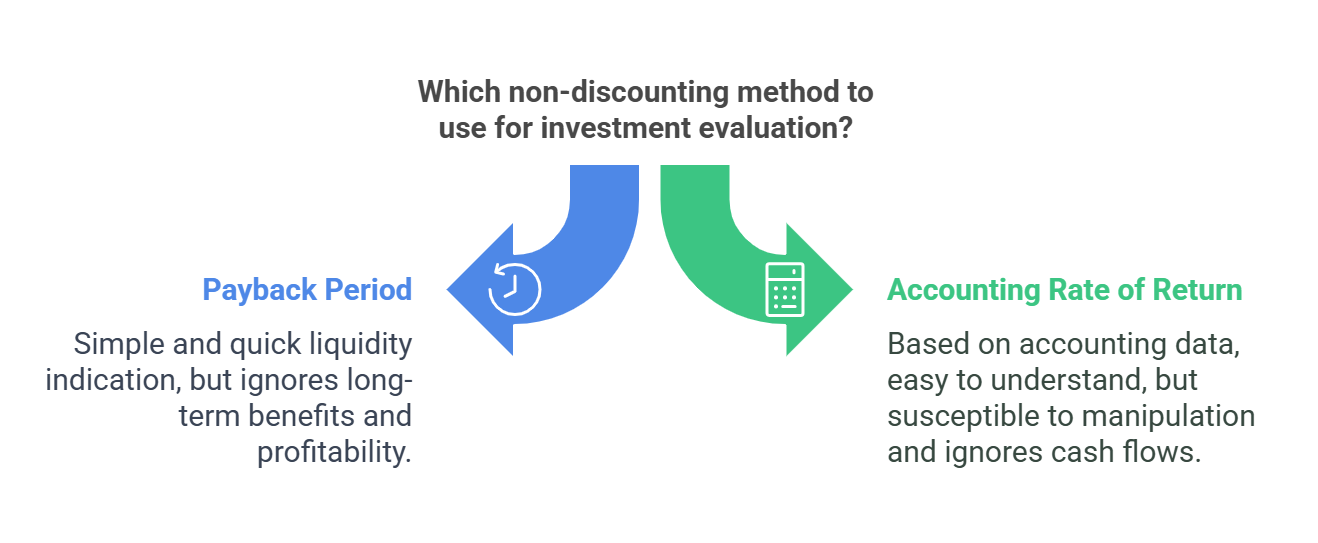

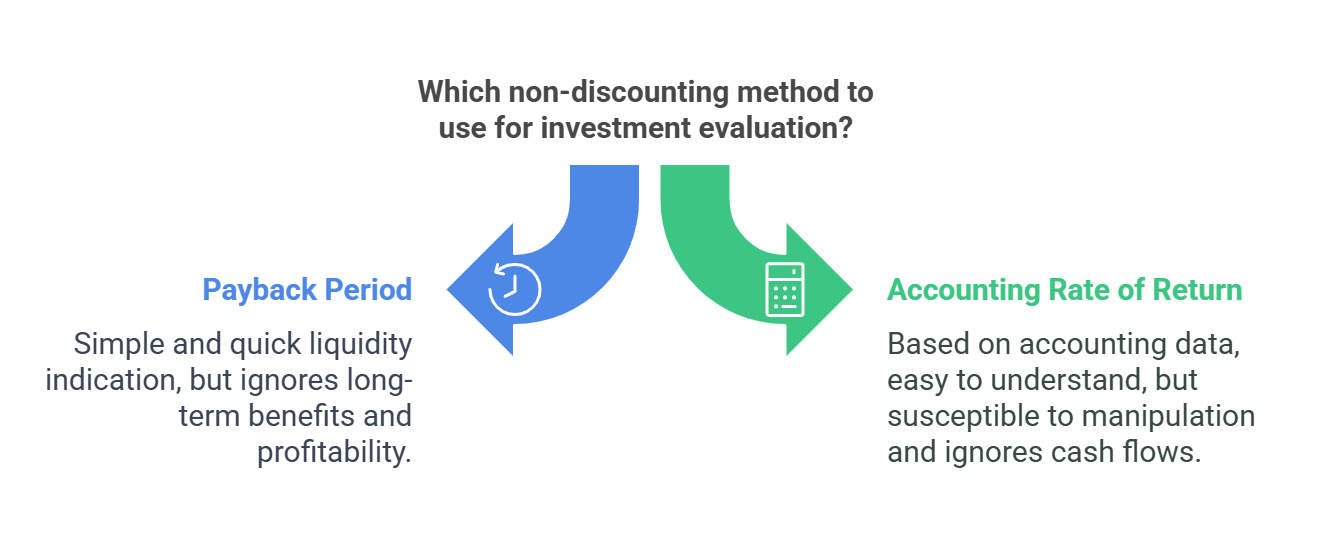

Non-discounting methods, also known as traditional methods, do not consider the time value of money. They are simpler to calculate but less accurate than discounting methods. Two common non-discounting methods are:

-

Payback Period (PBP):

-

Definition: The payback period is the length of time required for the cumulative cash inflows from a project to equal the initial investment. It measures how quickly the project recovers its initial cost.

-

Calculation:

- If cash inflows are uniform: Payback Period = Initial Investment / Annual Cash Inflow

- If cash inflows are non-uniform: The payback period is calculated by accumulating the cash inflows until they equal the initial investment.

-

Decision Rule: A project is acceptable if its payback period is less than a pre-determined maximum payback period (cutoff period) set by the company.

-

Advantages:

- Simple to understand and calculate.

- Provides a quick indication of the project's liquidity.

- Useful for projects in rapidly changing industries where speed of return is critical.

-

Disadvantages:

- Ignores the time value of money.

- Ignores cash flows beyond the payback period, potentially leading to the rejection of profitable projects with longer-term benefits.

- Does not consider the profitability of the project.

- The cutoff period is arbitrary.

-

-

Accounting Rate of Return (ARR):

-

Definition: The accounting rate of return, also known as the average rate of return, is the average annual profit (after tax) from a project expressed as a percentage of the average investment.

-

Calculation:

- ARR = (Average Annual Profit After Tax / Average Investment) * 100

- Average Investment = (Initial Investment + Salvage Value) / 2 (Often, Salvage Value is assumed to be 0, making Average Investment = Initial Investment / 2)

-

Decision Rule: A project is acceptable if its ARR is greater than a pre-determined minimum rate of return set by the company.

-

Advantages:

- Simple to understand and calculate.

- Uses readily available accounting data.

-

Disadvantages:

- Ignores the time value of money.

- Based on accounting profits, which can be subject to manipulation, rather than cash flows.

- Does not consider the project's entire life.

- The minimum rate of return is arbitrary.

- Can be affected by the depreciation method used.

In summary, while the Payback Period and Accounting Rate of Return are easy to compute, their failure to account for the time value of money makes them less reliable than discounted cash flow methods for evaluating investment opportunities.

In summary, while the Payback Period and Accounting Rate of Return are easy to compute, their failure to account for the time value of money makes them less reliable than discounted cash flow methods for evaluating investment opportunities.

-

No Comments