Crowdfunding

Introduction: The Digital Revolution and Financial Transformation

The past two decades have ushered in a profound transformation in how people connect and interact, largely driven by the explosive growth of the internet and the diverse services it enables. This digital revolution has permeated virtually every aspect of our lives, from shopping and travel to dining and, critically, financial transactions.

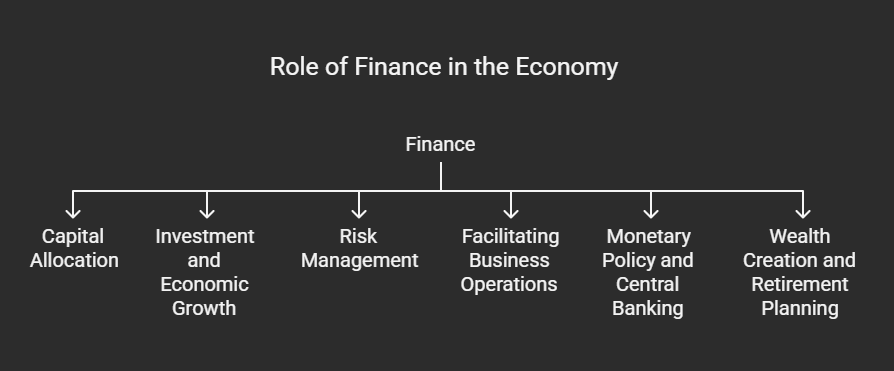

Role of Finance in the Economy

Finance is a cornerstone of any economy, facilitating the flow of funds and supporting economic activities at various levels. Here's a breakdown of its critical roles:

1. Capital Allocation:

- Finance enables the efficient allocation of financial resources, directing funds from savers to borrowers.

- Financial institutions act as intermediaries, channeling excess capital from savers to those needing it for investment.

- This process transforms small savings into large capital pools, supporting business and individual investments.

- Efficient capital allocation is crucial for promoting economic growth.

2. Investment and Economic Growth:

- Finance provides the capital necessary for investments in productive assets, such as infrastructure, machinery, and technology.

- These investments drive economic growth by increasing productivity, creating jobs, and stimulating consumption.

- Financial institutions and markets mobilize savings and direct them towards high-return productive activities.

3. Risk Management:

- Finance helps individuals and businesses manage various risks through insurance policies, derivatives, and hedging strategies.

- These tools mitigate financial risks associated with unforeseen events, market fluctuations, and natural disasters.

- Effective risk management contributes to stability and confidence in the economy.

4. Facilitating Business Operations:

- Businesses require financial resources to operate, expand, and innovate.

- Finance supports capital raising through equity financing (issuing shares) and debt financing (issuing bonds or loans).

- Adequate financing enables businesses to invest in R&D, hire employees, purchase inventory, and expand operations.

- This fosters entrepreneurship, innovation, and job creation, creating a resilient economic environment.

5. Monetary Policy and Central Banking:

- Finance intersects with monetary policy through central banks, which regulate the money supply, interest rates, and financial stability.

- Central banks use tools like interest rate adjustments and open market operations to manage inflation and stabilize financial markets.

- Effective monetary policy contributes to price stability, sustainable economic growth, and efficient capital allocation.

6. Wealth Creation and Retirement Planning:

- Finance enables individuals to build and preserve wealth through investments and wealth management services.

- It supports saving for retirement, education, home purchases, and other long-term financial goals.

- Access to investment opportunities and financial advice empowers individuals to achieve financial security and improve their standard of living.

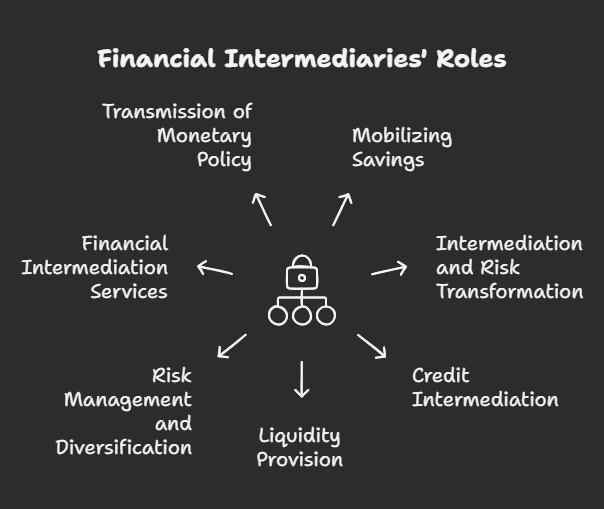

Role of Financial Intermediaries

Financial intermediaries are crucial players in the financial system, acting as a bridge between those with surplus funds (savers) and those who need funds (borrowers). They channel funds, manage risks, and facilitate various financial transactions, contributing to the overall efficiency and stability of the economy.

Here's a breakdown of their key roles:

1. Mobilizing Savings

- Function: Financial intermediaries, such as banks, credit unions, and mutual funds, collect savings from individuals, businesses, and other entities.

- Explanation: They attract deposits and investments, pooling small amounts of savings from many individuals into significant capital. This aggregation allows for efficient capital allocation for productive purposes.

- Example: A commercial bank gathers deposits from numerous individuals and businesses, creating a pool of funds available for lending.

2. Intermediation and Risk Transformation

- Function: They transform short-term, low-risk deposits into longer-term, potentially higher-risk loans and investments.

- Explanation: This process involves accepting deposits with immediate withdrawal options and providing loans with longer repayment periods. Intermediaries diversify and manage risks, making the financial system more efficient.

- Example: A bank accepts short-term deposits and provides long-term mortgage loans. The bank manages the risk by diversifying its loan portfolio.

3. Credit Intermediation

- Function: Financial intermediaries provide credit to borrowers.

- Explanation: They evaluate the creditworthiness of borrowers and extend loans to individuals, households, businesses, and governments. This credit provision finances diverse activities, from business expansion to home purchases.

- Example: A credit union lends money to a small business owner to expand their operations.

4. Liquidity Provision

- Function: They offer liquidity services by providing access to funds when needed.

- Explanation: Banks allow depositors to withdraw funds on demand and provide short-term borrowing options. This ensures the smooth functioning of financial markets and facilitates economic transactions.

- Example: A person withdraws cash from their checking account at an ATM.

5. Risk Management and Diversification

- Function: They manage risks by diversifying their portfolios.

- Explanation: By holding a diversified portfolio of loans, securities, and other assets, intermediaries mitigate the risk associated with individual borrowers or investments. This enhances the stability of the financial system.

- Example: A mutual fund invests in a wide range of stocks and bonds, reducing the impact of any single investment's poor performance.

6. Financial Intermediation Services

- Function: They offer a wide range of financial services.

- Explanation: These services include deposit accounts, payment systems, investment products, insurance, advisory services, and asset management. They provide expertise and convenience in facilitating financial transactions.

- Example: An investment bank provides financial advisory services to a corporation issuing bonds.

7. Transmission of Monetary Policy

- Function: They play a vital role in transmitting monetary policy.

- Explanation: Changes in interest rates and other monetary policy measures impact the cost of borrowing and lending. Through their lending and deposit activities, intermediaries help transmit these policies to the broader economy.

- Example: A central bank raises interest rates, leading commercial banks to increase their lending rates, thus slowing down borrowing and economic activity.

Crowdfunding

Crowdfunding is a method of raising capital by collecting small amounts of money from a large number of people, typically via the internet. It leverages the power of collective contributions to fund various projects, ventures, or causes.

No Comments