Due diligence; Methods of payment and financing options in M&A.

Due Diligence in Mergers and Acquisitions

Due diligence is the process of gathering and analyzing information before making a decision, particularly in investment and M&A contexts. It's a crucial risk assessment tool, involving a thorough examination of the target company to evaluate its potential and identify any red flags.

Purpose of Due Diligence

The primary purpose of due diligence is to mitigate risk. It ensures that all parties involved in a transaction are fully aware of its terms and potential consequences. For example, in a financial context, a broker-dealer will conduct due diligence on an investment product and share the report with the investor, ensuring informed decision-making and limiting liability for potential losses. In M&A, due diligence helps the acquirer understand the true value and risks associated with the target company.

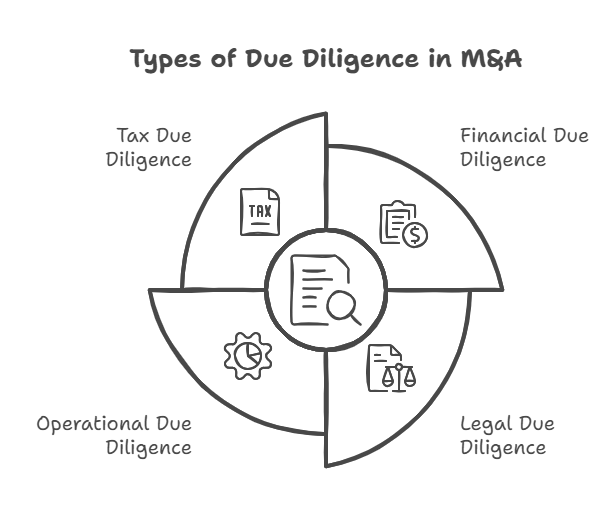

Types of Due Diligence in M&A

-

Financial Due Diligence: This involves analyzing the target company's historical financial performance, verifying the accuracy and reliability of its financial statements, and assessing its future financial prospects. It includes reviewing financial statements, tax returns, and other relevant financial documents.

-

Legal Due Diligence: This focuses on the legal aspects of the target company and its interactions with stakeholders. It includes examining licenses, regulatory compliance, contracts, litigation, and any outstanding legal liabilities.

-

Operational Due Diligence: This examines the target company's operations, focusing on how it converts inputs into outputs. It involves understanding the company's processes, technology, supply chain, and management structure. This is often considered the most critical type of due diligence as it provides insights into the target's actual functioning.

-

Tax Due Diligence: This reviews all tax-related matters of the target company, ensuring compliance and identifying any potential tax liabilities. It also considers the tax implications of the merger or acquisition for the combined entity.

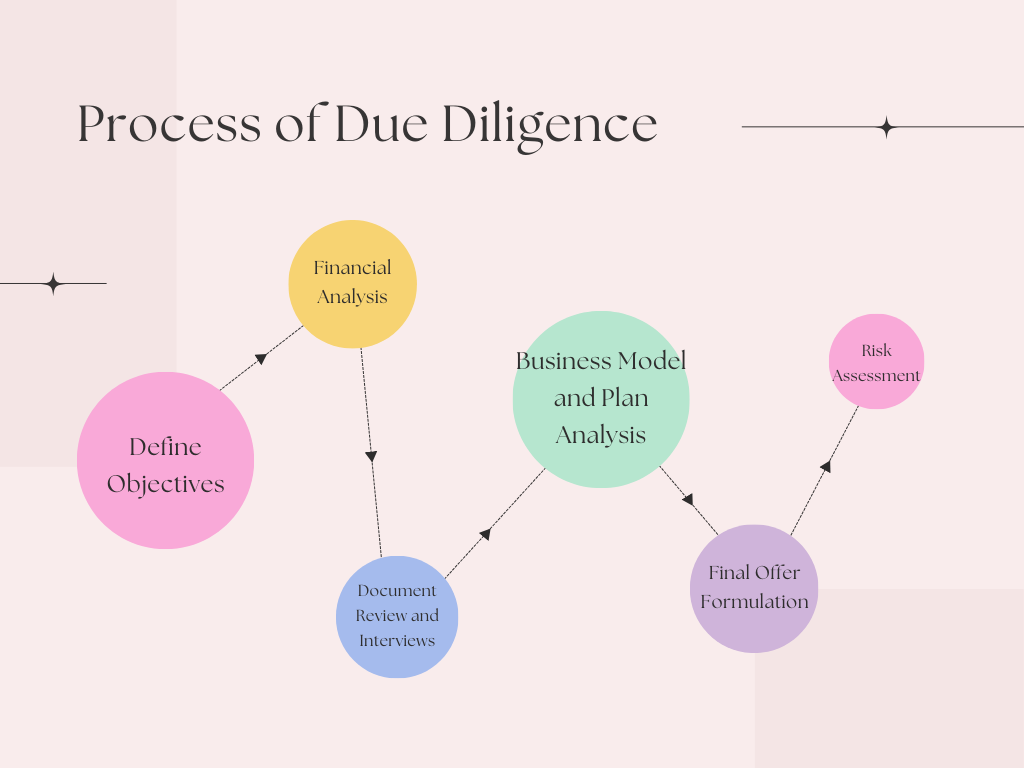

Process of Due Diligence

-

Define Objectives: Clearly define the goals of the transaction. This could include entering a new market, acquiring new technology, or increasing market share. Having clear objectives helps focus the due diligence efforts and identify the necessary resources.

-

Financial Analysis: Scrutinize the target company's financial records for accuracy and reliability. This involves reviewing financial statements, income statements, tax returns, and debt schedules. The goal is to assess the company's financial health, performance, and identify any potential financial risks.

-

Document Review and Interviews: Request relevant documentation from the target company and conduct interviews with key personnel. This provides a deeper understanding of the company's operations, culture, and management. It also helps verify the information provided in the documents and identify any inconsistencies.

-

Business Model and Plan Analysis: Evaluate the target company's business model and plan to assess its viability and alignment with the acquirer's strategic objectives. This step helps understand the target's long-term sustainability and its fit within the acquiring organization.

-

Final Offer Formulation: Based on the information gathered, develop a final valuation and offer. This step involves collaboration between different teams to ensure a fair and reasonable offer.

-

Risk Assessment: Identify and assess potential risks associated with the acquisition. This includes financial, operational, and market-related risks. Effective risk management strategies should be developed to mitigate these risks.

Methods of Payment in Mergers and Acquisitions

The methods of payment in mergers and acquisitions (M&A) are the financial strategies used by corporations to carry out these commercial transactions. Choosing the right payment method is crucial for the success of the deal. Here's a breakdown of common payment options:

1. Payment in Cash

- Description: The acquiring company pays the target company's shareholders in cash.

-

Advantages:

- Simplicity and Transparency: Cash offers a straightforward and easily understood payment method.

- Certainty: Sellers receive a guaranteed amount, eliminating the risk associated with fluctuating stock prices.

-

Disadvantages:

- Large Outlay: Requires a significant upfront cash reserve for the acquirer.

- Tax Implications: Sellers may face immediate capital gains taxes on the cash received.

- Opportunity Cost: Tying up large amounts of cash can limit the acquirer's ability to pursue other investments.

2. Security Payment

This method involves the acquirer issuing new securities to the target company's shareholders. It can take two primary forms:

- Description: The acquirer issues its own shares to the target company's shareholders in exchange for their shares or assets. A common form is a share exchange.

-

Advantages:

- Preserves Cash: Conserves the acquirer's cash reserves.

- Potential Tax Deferral: Shareholders may be able to defer capital gains taxes until they sell the newly acquired shares.

-

Disadvantages:

- Dilution: Issuing new shares can dilute the ownership of existing shareholders in the acquiring company.

- Valuation Challenges: Determining the fair value of the shares being exchanged can be complex.

- Price Volatility: The value of the shares received can fluctuate, impacting the overall value of the deal for the seller.

(b) Bond Payment (Debt Securities):

- Description: The acquirer issues bonds (debt obligations) to the target company's shareholders in exchange for their shares or assets. These bonds typically have a high credit rating.

-

Advantages:

- Flexibility: Can be structured with varying maturities and interest rates.

- Tax Deductibility: Interest payments on the bonds are often tax-deductible for the acquirer.

-

Disadvantages:

- Debt Burden: Increases the acquirer's debt load.

- Interest Payments: Requires ongoing interest payments, which can impact profitability.

3. Leveraged Buyout (LBO)

- Description: The acquiring company (often a private equity firm) uses a significant amount of borrowed money (debt) to finance the acquisition. The target company's assets and future cash flows are often used as collateral for the debt.

-

Advantages:

- Limited Equity Investment: Allows for large acquisitions with a relatively small amount of the acquirer's own capital.

-

Disadvantages:

- High Debt Levels: Creates a substantial debt burden for the acquired company.

- Financial Risk: Increases the risk of financial distress if the acquired company's performance does not meet expectations.

- Higher Capital Costs: Interest rates on LBO debt are typically higher than other forms of financing.

4. Debt Financing (Assumption of Debt)

- Description: Instead of paying cash or stock, the acquirer agrees to assume the existing debt of the target company.

-

Advantages:

- Alternative to Cash or Stock: Provides another option for structuring the deal.

- Can be Attractive to Distressed Sellers: Useful when the target company is struggling with debt.

-

Disadvantages:

- Increased Debt Load: Adds to the acquirer's financial obligations.

- Financial Risk: Can be risky if the assumed debt is substantial or if the target company's financial situation deteriorates.

5. Earnout

- Description: A portion of the purchase price is contingent on the target company achieving specific performance targets after the acquisition. This is often used when there is a disagreement about the valuation of the target company.

-

Advantages:

- Bridges Valuation Gaps: Allows buyers and sellers to reach an agreement when they have different views on the target's value.

- Incentivizes Performance: Motivates the target company's management to achieve agreed-upon goals.

-

Disadvantages:

- Complexity: Can be complex to structure and administer.

- Potential for Disputes: Disagreements can arise over whether the performance targets have been met.

Choosing the appropriate payment method in a merger or acquisition requires careful consideration of various factors, including the financial positions of both companies, tax implications, market conditions, and the specific goals of the transaction.

No Comments