Provisions of Companies Act 2013

Analysis of Mergers and Acquisitions under the Companies Act, 2013

This essay analyzes the impact of the Companies Act, 2013 on mergers and acquisitions (M&A) in India, focusing on the changes introduced and comparing them with the previous Companies Act of 1956. Specifically, it examines the provisions related to arrangements, compromises, and amalgamations (Sections 230-240) within Chapter XV of the 2013 Act.

Introduction

The Companies Act, 2013 represented a significant shift in Indian corporate law. Initially, it comprised 479 clauses, 29 chapters, and 7 schedules, gradually replacing the Companies Act of 1956. A crucial step in this transition occurred on December 7, 2016, when the Ministry of Corporate Affairs notified 90 sections of the 2013 Act, bringing them into effect on December 15, 2016. This notification included Chapter XV (Sections 230-240), dedicated to arrangements, compromises, and amalgamations. Furthermore, the Companies (Arrangements, Compromises, and Amalgamations) Rules, 2016, also came into force on the same date.

Focus of the Analysis

This analysis delves into the effects of these new M&A related laws introduced by the Companies Act, 2013. It explores the new concepts introduced and examines the changes made to existing provisions compared to the 1956 Act. The analysis will proceed as follows:

-

Analysis of Altered Concepts: This section will dissect the key changes introduced by the 2013 Act concerning M&A, specifically focusing on the provisions within Chapter XV (Sections 230-240). It will explain how these provisions differ from their counterparts in the 1956 Act.

-

Comparison with the 1956 Act: This section will provide a detailed comparison of the corresponding provisions related to arrangements, compromises, and amalgamations under the Companies Act of 1956. This comparison will highlight the evolution of the legal framework governing M&A in India.

Comparison of M&A Provisions: Companies Act 1956 vs. 2013

This document compares the provisions related to Mergers and Acquisitions (M&A) under the Companies Act, 1956 and the Companies Act, 2013, highlighting the key changes introduced by the newer legislation.

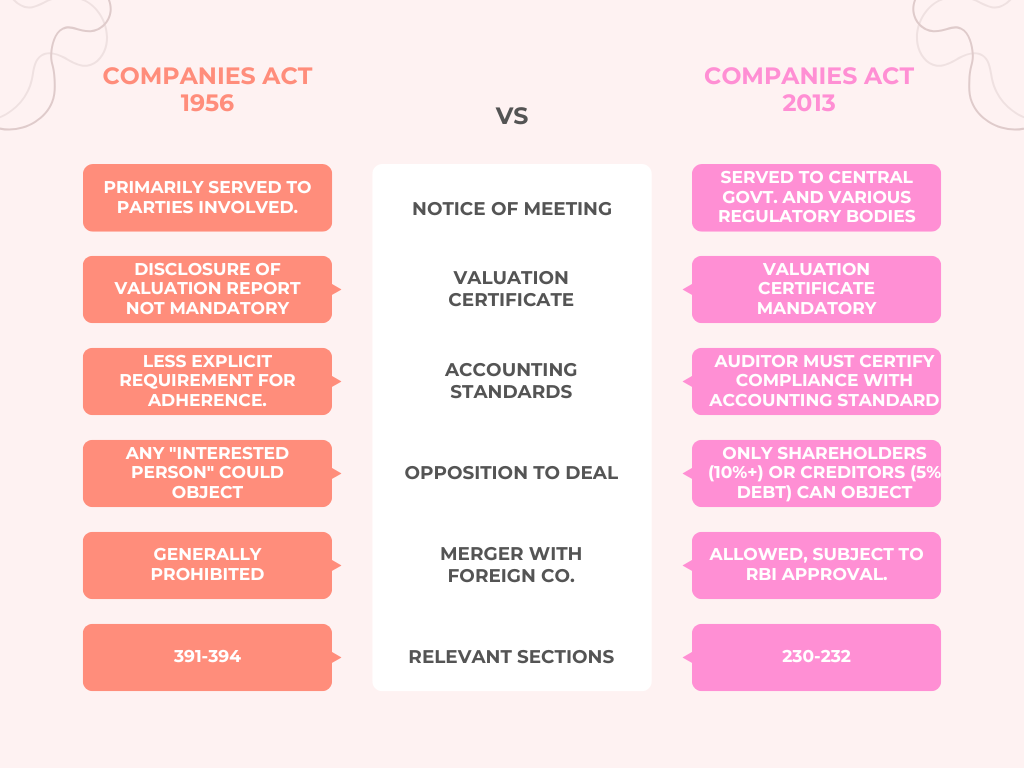

Relevant Sections

- Companies Act, 1956: Sections 391 to 394 governed M&A.

- Companies Act, 2013: Sections 230 to 232 now govern M&A.

Key M&A-Related Changes under the 2013 Act

The 2013 Act introduced several significant changes to the M&A landscape. These include:

1. Notice of Meeting

- 1956 Act: Notice of the meeting to approve the compromise or arrangement was primarily served to parties involved.

- 2013 Act: In addition to the Central Government, notice must be given to various regulatory bodies potentially affected by the scheme.

- Interpretation & Consequences: This shift from a one-party process to a multi-party one, involving various regulatory bodies, may increase the complexity and paperwork involved in M&A transactions.

2. Annexed Valuation Certificate

- 1956 Act: Disclosure of the valuation report to shareholders was not mandatory.

- 2013 Act: The valuation certificate is now a mandatory part of the scheme and must be annexed to the notice of the meeting.

- Interpretation & Consequences: This enhances transparency, empowering shareholders to make informed decisions. Companies must ensure robust valuations due to increased scrutiny.

3. Adherence to Accounting Standards

- 1956 Act: Less explicit requirement for adherence to accounting standards in scheme approvals.

- 2013 Act: The company's auditor must certify that the proposed scheme complies with applicable accounting standards. This certificate must be submitted to the tribunal.

- Interpretation & Consequences: This aligns with SEBI requirements for listed companies and applies them to all companies, preventing creative accounting and ensuring greater financial transparency.

4. Opposition to a Deal or Compromise

- 1956 Act: Any "interested person" could object to a compromise or arrangement.

- 2013 Act: Only shareholders holding at least 10% of shares or creditors with at least 5% of total debt (based on the latest audited financial statements) can object.

- Interpretation & Consequences: This threshold limits frivolous litigation and protects schemes from unnecessary delays caused by minor stakeholders.

5. Amalgamation/Merger with a Foreign Company

- 1956 Act: Generally prohibited mergers of Indian companies with foreign companies (the resulting entity had to be Indian).

- 2013 Act: Allows mergers between Indian and foreign companies (from notified jurisdictions), subject to RBI approval. Consideration can be in cash, depository receipts, or both.

- Interpretation & Consequences: This facilitates cross-border M&A, enabling Indian companies to expand globally and attract foreign investment. The specific jurisdictions allowed for such mergers are subject to notification.

6. Fast-Track Merger

- 1956 Act: All amalgamations and mergers required court approval.

- 2013 Act: Exempts mergers and amalgamations between small companies, holding companies and their wholly-owned subsidiaries, and other prescribed companies from court approval. Requires approval by members holding at least 90% of shares and creditors representing 90% of the value of debt. Notification to various authorities is still required.

- Interpretation & Consequences: This streamlines the M&A process for eligible companies, reducing time and costs associated with court proceedings. However, clarity is needed on transitional provisions and the application of other requirements (like auditor certificates and valuation reports) to fast-track mergers.

Conclusion

The Companies Act, 2013 has significantly modernized the M&A framework in India. The changes aim to increase transparency, expedite processes, and align Indian regulations with international best practices. The introduction of the National Company Law Tribunal (NCLT) further contributes to a more streamlined and efficient M&A landscape. While the 2013 Act has brought about positive changes, some areas, such as the specifics of fast-track mergers, may require further clarification and guidance to ensure smooth implementation.

Quick Revision

No Comments