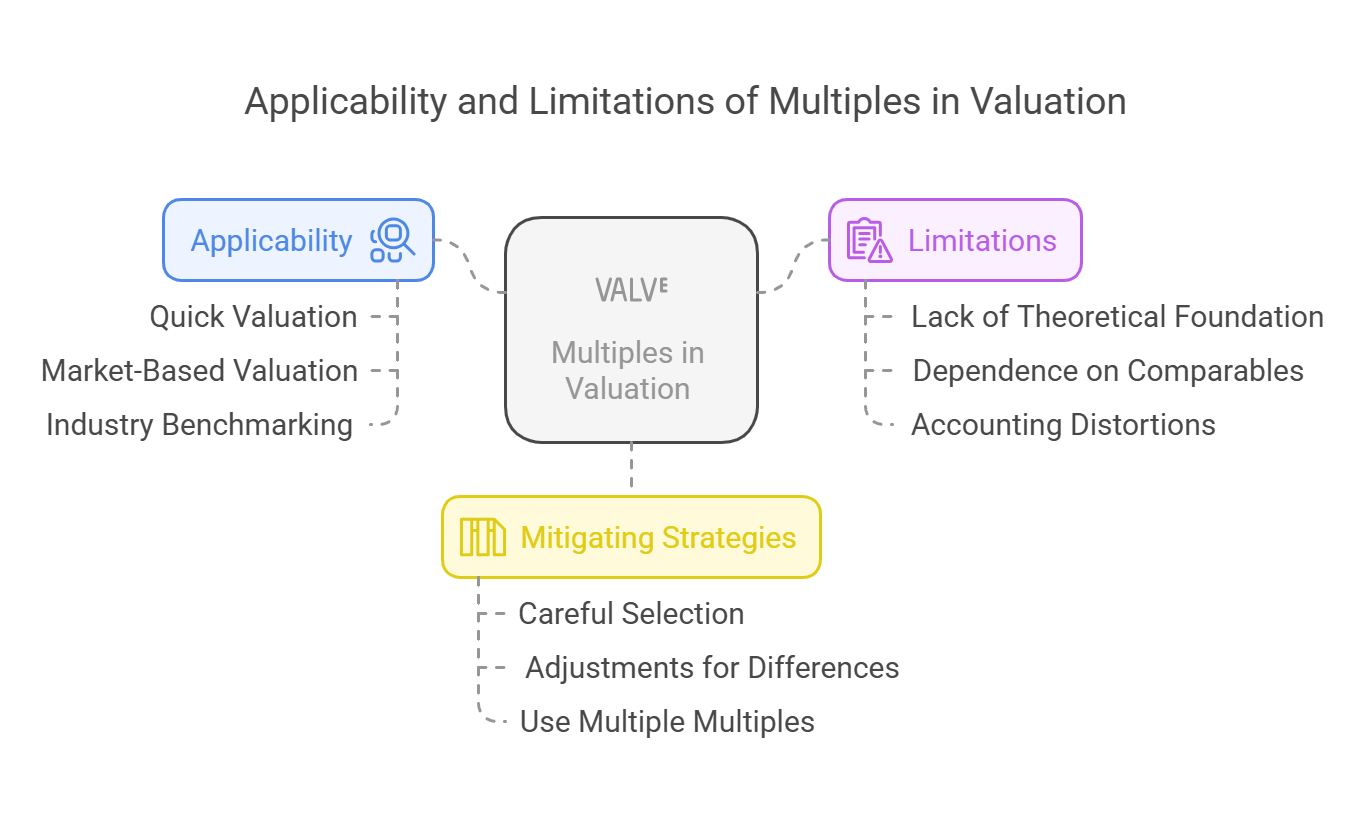

Applicability and Limitations of Multiples

Multiples are a widely used tool in relative valuation, offering a quick and easy way to assess value by comparing a company to its peers. However, their simplicity comes with limitations that must be carefully considered.

Applicability of Multiples:

- Quick and Easy Valuation: Multiples are relatively easy to calculate and interpret, making them a convenient tool for preliminary valuation analysis.

- Market-Based Valuation: Multiples reflect market sentiment and the collective wisdom of investors, providing a reality check against purely theoretical valuations.

- Valuing Companies with Limited Information: Multiples can be useful when limited information is available about a company's future cash flows.

- Comparable Companies Available: Multiples are most applicable when there are a sufficient number of comparable companies or transactions available.

- Industry Benchmarking: Multiples are widely used for industry benchmarking, allowing companies to compare their performance and valuation to their peers.

- Private Company Valuation: Multiples are often used to value private companies, where DCF valuation may be more challenging due to a lack of publicly available data.

- M&A Transactions: Multiples are commonly used in M&A transactions to determine the fair price to pay for a target company.

- "Reality Check" for DCF Valuations: Comparing multiple-based valuations to DCF valuations can reveal if the DCF is relying on overly optimistic assumptions.

Limitations of Multiples:

- Lack of Theoretical Foundation: Multiples are based on empirical observation rather than a strong theoretical foundation. They do not explicitly consider the time value of money or the riskiness of future cash flows.

-

Dependence on Comparable Companies: The accuracy of multiples depends heavily on the selection of comparable companies. If the comparables are not truly comparable, the valuation can be misleading.

- Finding Truly Comparable Companies: Difficult to find companies exactly similar in business model, risk profile, and growth prospects.

- Industry Classifications: Relying on broad industry classifications may include companies that are not directly comparable.

-

Accounting Distortions: Multiples can be distorted by differences in accounting practices.

- GAAP vs. IFRS: Different accounting standards can affect financial metrics and multiples.

- Aggressive Accounting: Companies may use aggressive accounting practices to inflate earnings and boost their multiples.

-

Ignoring Growth Potential: Multiples often fail to fully account for differences in growth potential between companies.

- Static Snapshot: Multiples are a snapshot in time and may not reflect future growth opportunities.

-

Ignoring Risk Differences: Multiples do not explicitly account for differences in risk between companies.

- Risk Premium: Higher-risk companies should trade at lower multiples, but this is not always reflected in market prices.

- Circular Reasoning: Using market data to value a company implicitly assumes that the market is efficient, which may not be the case.

- Potential for Misinterpretation: Multiples can be easily misinterpreted if they are not used in conjunction with other valuation techniques and a thorough understanding of the company and its industry.

- Oversimplification: Multiples can oversimplify the valuation process by focusing on a single financial metric and ignoring other important factors.

- Backward Looking: Many multiples rely on historical data, which may not be representative of future performance.

- Sensitivity to Outliers: Multiples can be heavily influenced by outliers in the data.

- No Clear Guidance: Multiples can indicate undervaluation or overvaluation, but they provide no clear guidance on what the "right" value should be.

- Vulnerable to Market Sentiment: Multiples can be driven by market sentiment rather than fundamental value.

Mitigating the Limitations:

- Careful Selection of Comparables: Choose comparable companies that are as similar as possible to the target company in terms of industry, business model, risk profile, and growth prospects.

- Adjustments for Differences: Adjust the multiples of comparable companies to account for differences in size, growth, risk, accounting practices, or other factors.

- Use Multiple Multiples: Consider using a variety of different multiples to get a more comprehensive view of the company's valuation.

- Consider Industry-Specific Multiples: Use industry-specific multiples that are relevant to the company's business.

- Cross-Check with Other Valuation Techniques: Compare the multiple-based valuation to other valuation techniques, such as DCF valuation or asset-based valuation.

- Sensitivity Analysis: Conduct sensitivity analysis to assess the impact of different assumptions on the multiple-based valuation.

-

Consider the Context: Always consider the context in which the multiples are being used. Industry-specific factors and market conditions can affect multiples.

In conclusion, multiples are a useful tool for relative valuation, but they should be used with caution. Understanding their limitations and taking steps to mitigate those limitations is essential for making informed investment decisions.

In conclusion, multiples are a useful tool for relative valuation, but they should be used with caution. Understanding their limitations and taking steps to mitigate those limitations is essential for making informed investment decisions.

No Comments