Introduction to Valuation

Philosophical Basis, Generalities, and Role

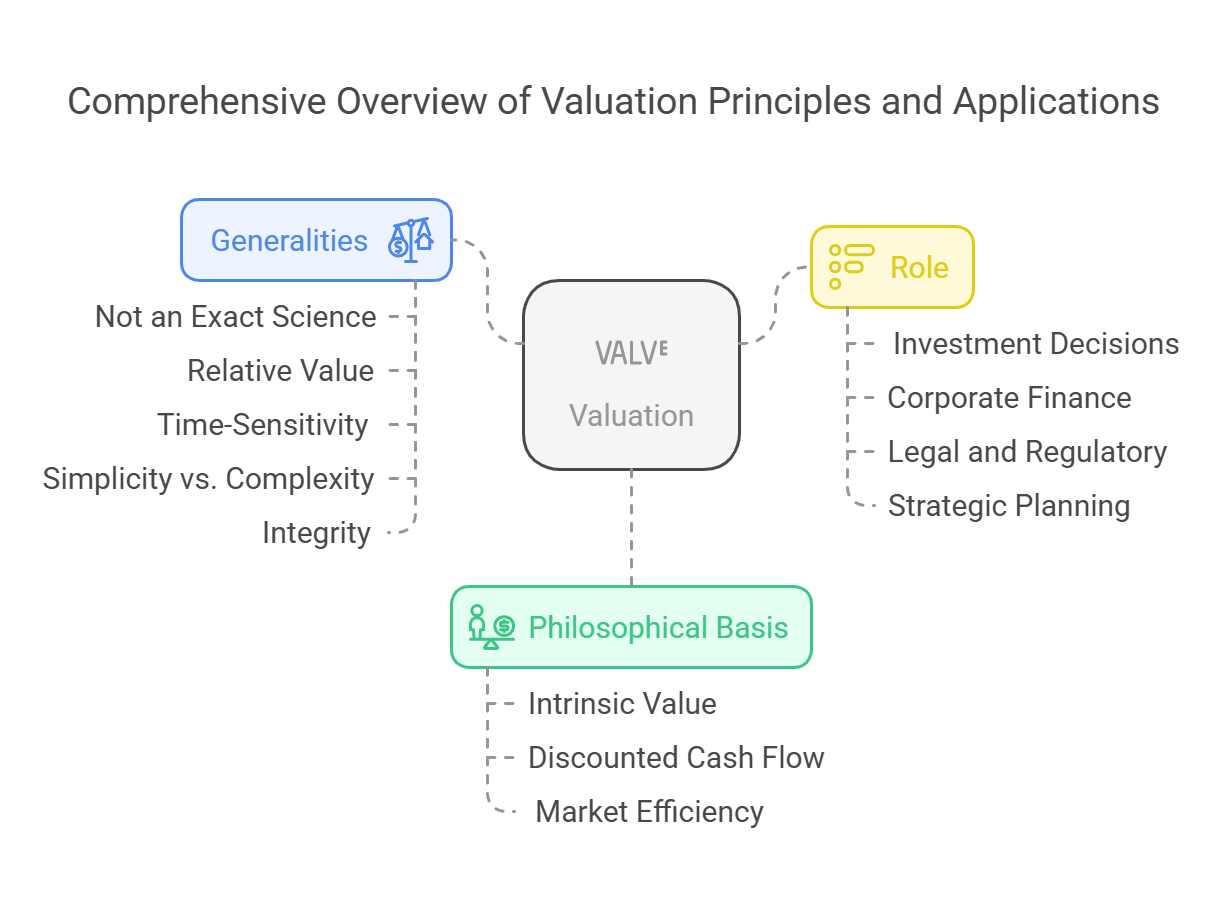

This topic introduces the fundamental concepts underpinning valuation, covering its philosophical underpinnings, general principles, and practical applications.

1. Philosophical Basis for Valuation:

1. Philosophical Basis for Valuation:

-

Intrinsic Value: Valuation is rooted in the concept of intrinsic value - the true, underlying value of an asset, independent of its market price.

- Objective vs. Subjective: While intrinsic value aims to be objective, its estimation inevitably involves subjective assumptions about future cash flows, growth rates, and risk.

- Margin of Safety: Investors seek to buy assets at a price below their estimated intrinsic value, creating a "margin of safety" to protect against errors in valuation.

-

Discounted Cash Flow (DCF) Principle: The most fundamental principle is that the value of an asset is the present value of its expected future cash flows, discounted at a rate that reflects the riskiness of those cash flows.

- Time Value of Money: A dollar today is worth more than a dollar tomorrow due to the potential for earning interest or returns.

- Risk and Return: Investors demand a higher return for taking on more risk. The discount rate reflects this required return.

-

Market Efficiency: The degree to which market prices reflect all available information.

- Efficient Market Hypothesis (EMH): Different forms exist (weak, semi-strong, strong), suggesting the difficulty of consistently "beating the market" through valuation. Valuation is most valuable in less efficient markets.

- Valuation Opportunities: Valuation is most useful when markets are inefficient, allowing for the identification of undervalued or overvalued assets.

2. Generalities about Valuation:

-

Valuation is Not an Exact Science: It is an art as much as a science, relying on judgment and assumptions. Different analysts will arrive at different valuations.

- Range of Values: A valuation should be viewed as a range of possible values rather than a single, precise number.

- Sensitivity Analysis: It is essential to perform sensitivity analysis to understand how the valuation changes with different assumptions.

-

Valuation is Relative: The value of an asset is often determined relative to the value of comparable assets.

- Comparable Companies: Comparing valuation ratios (e.g., P/E, P/B) to those of similar companies.

- Transaction Multiples: Analyzing the prices paid for similar assets in recent transactions.

-

Valuation is Time-Sensitive: Values change over time as new information becomes available and market conditions evolve.

- Dynamic Process: Valuation is an ongoing process that should be updated regularly.

- Event-Driven: Significant events (e.g., earnings announcements, mergers, regulatory changes) can trigger reassessments of value.

-

Simplicity vs. Complexity: Simpler valuation models are often more reliable than complex ones, especially when dealing with limited or uncertain data.

- Occam's Razor: The simplest explanation is usually the best.

- Data Availability: The complexity of the model should be appropriate for the available data.

-

Valuation Requires Integrity: Valuations can be manipulated to achieve a desired outcome. Objectivity and intellectual honesty are paramount.

- Avoiding Bias: Consciously avoiding biases that can influence the valuation process.

- Transparency: Clearly disclosing all assumptions and methodologies used in the valuation.

3. Role of Valuation:

-

Investment Decisions:

- Stock Selection: Identifying undervalued or overvalued stocks for investment.

- Portfolio Management: Constructing and managing a portfolio of assets based on valuation principles.

-

Corporate Finance Decisions:

- Capital Budgeting: Evaluating investment projects to determine whether they will create value for the company.

- Mergers and Acquisitions (M&A): Determining the fair price to pay for a target company.

- Divestitures: Deciding whether to sell a business unit and at what price.

-

Legal and Regulatory Purposes:

- Tax Reporting: Determining the fair market value of assets for tax purposes.

- Bankruptcy Proceedings: Valuing assets and liabilities in bankruptcy proceedings.

- Litigation Support: Providing expert testimony on valuation matters in legal disputes.

-

Strategic Planning:

- Resource Allocation: Valuing different business units to make informed decisions about resource allocation.

- Performance Measurement: Evaluating the performance of business units based on their value creation.

In summary, valuation provides a framework for making informed decisions about the allocation of capital, whether for investment, corporate finance, legal, or strategic purposes. It rests on the principles of intrinsic value and discounted cash flow, while acknowledging the inherent subjectivity and uncertainties involved.

No Comments