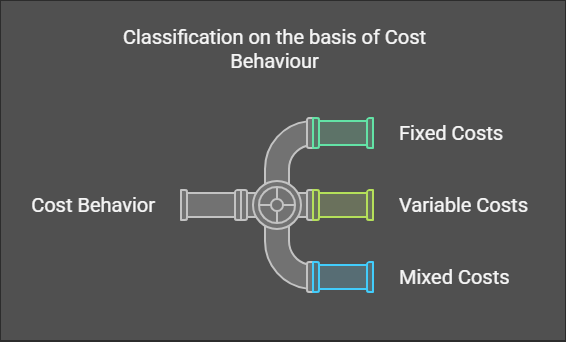

Classification of Cost

Fixed Costs

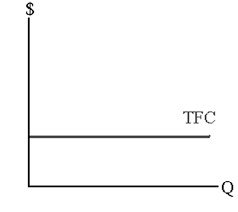

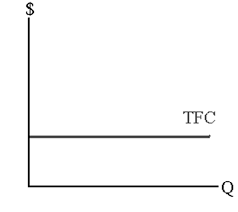

Fixed costs are those costs that remain constant in total amount regardless of changes in the level of activity or production within a relevant range. They are related to the passage of time rather than the level of output.

-

Definition: Costs that do not change with the level of activity within a relevant range.

-

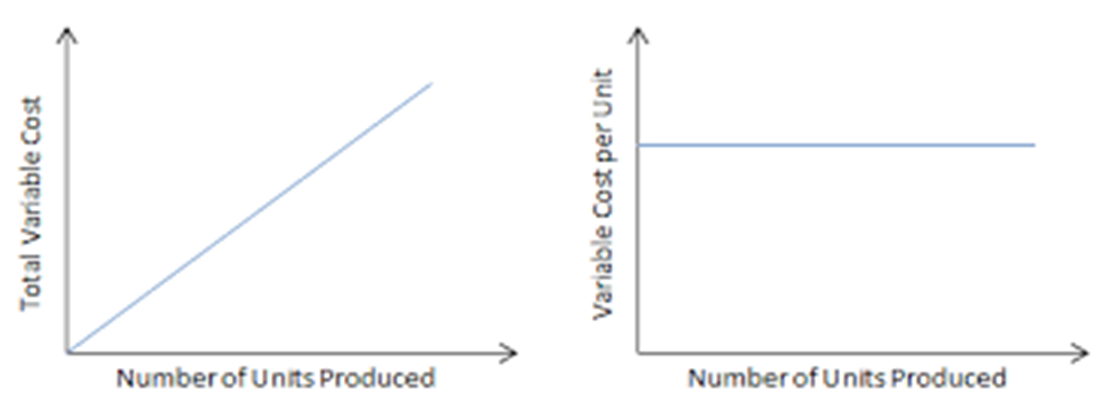

Total Fixed Costs: Remain constant regardless of output changes (within the relevant range).

-

Total Fixed Costs: Remain constant regardless of output changes (within the relevant range).

-

Examples:

- Rent of facilities

- Property taxes

- Insurance premiums

- Salaries of administrative and supervisory staff (unless they are directly tied to production volume)

- Depreciation of fixed assets (using the straight-line method)

Types of Fixed Costs

-

Committed Fixed Costs: These are long-term fixed costs required to maintain the company's basic operating capacity. They are difficult to change in the short term, and management has little discretion over them.

- Examples: Mortgage payments, lease agreements, salaries of key personnel under long-term contracts.

-

Discretionary Fixed Costs (Managed Fixed Costs): These fixed costs are determined by management's decisions and can be adjusted more easily in the short term. They are often part of the annual budgeting process.

- Examples: Advertising expenses, research and development costs, employee training programs.

Variable Costs

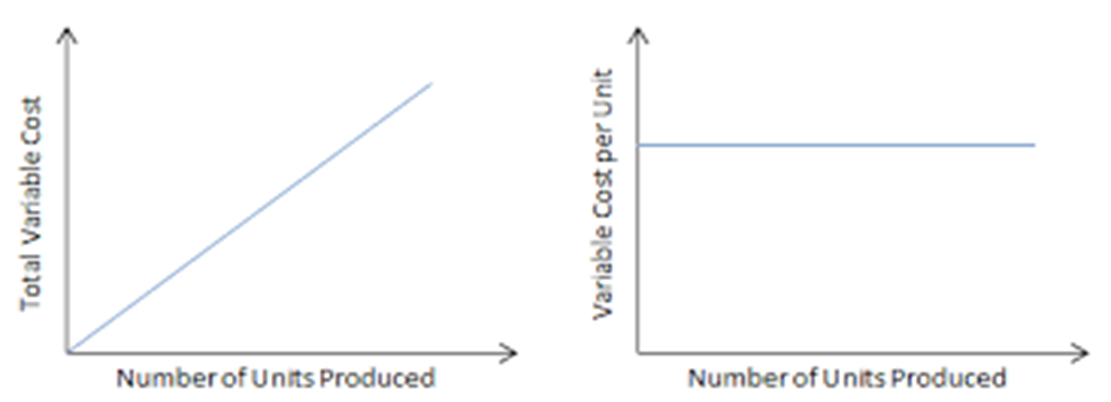

Variable costs are costs that change in direct proportion to changes in the level of activity or production. The total variable cost increases or decreases as output increases or decreases, respectively. However, the variable cost per unit remains constant.

-

Definition: Costs that vary directly and proportionally with changes in the level of activity or output.

-

Examples:

- Direct materials (raw materials used in production)

- Direct labor (wages of workers directly involved in production)

- Sales commissions (if based on sales volume)

- Shipping costs (if based on the number of units shipped)

- Variable manufacturing overhead (e.g., electricity used in production if it varies directly with output)

Mixed Costs (Semi-Variable Costs)

Mixed costs, also known as semi-variable costs, contain both fixed and variable components. This means they change with the level of activity or output, but not in direct proportion. Unlike purely variable costs, they don't increase or decrease at a constant rate with production changes due to their fixed cost element.

Examples of Mixed Costs

- Electricity Bills: May have a fixed charge for connection and a variable charge based on kilowatt-hours consumed.

- Salaries with Commissions: A salesperson might receive a fixed base salary plus a commission based on sales volume. The fixed salary is the fixed component, and the commission is the variable component.

Cost Classification Based on Timing of Charges Against Sales Revenue

Costs can be classified based on when they are charged against sales revenue. This classification helps in understanding the relationship between costs and revenue generation. The two main categories are Product Costs and Period Costs.

Product Costs

-

Definition: Product costs are those costs that are directly associated with the production of goods. They are considered inventoriable costs, meaning they are included in the value of inventory and are expensed only when the inventory is sold (Cost of Goods Sold - COGS).

-

Examples:

- Direct Materials: Raw materials that become part of the finished product (e.g., wood for furniture, fabric for clothing).

- Direct Labor: Wages paid to workers directly involved in the production process (e.g., assembly line workers, machine operators).

- Factory Overhead: All indirect costs associated with manufacturing

2. Period Costs

-

Definition: Period costs are costs that are not directly related to the production of goods. They are expensed in the period in which they are incurred, regardless of the level of production.

-

Examples:

- Selling and Distribution Overheads: Costs associated with marketing, selling, and delivering the product to customers (e.g., advertising expenses, sales commissions, shipping costs).

- Office and Administrative Overheads: Costs related to the general administration of the business (e.g., salaries of administrative staff, rent for office space, utilities for the office).

Cost Classification Based on Traceability to Cost Object

Costs can be categorized based on how easily they can be traced to a specific cost object.

Cost Object:-

- A cost object is anything for which we want to measure the cost, such as a product, service, project, or department.

- An activity, contract, customer, process, product, project, service or any other object for which costs are ascertained.”

1. Direct Costs

-

Definition: Direct costs are costs that can be easily and directly traced to a specific cost object. There is a clear and measurable cause-and-effect relationship between the cost and the cost object.

-

Examples:

- Direct Materials

- Direct Labor

2. Indirect Costs

-

Definition: Indirect costs are costs that cannot be easily and directly traced to a specific cost object. These costs are often shared by multiple cost objects, making it difficult or impractical to directly assign them to a single cost object.

-

Examples:

- Indirect Materials

- Indirect Labor

- Manufacturing Overhead

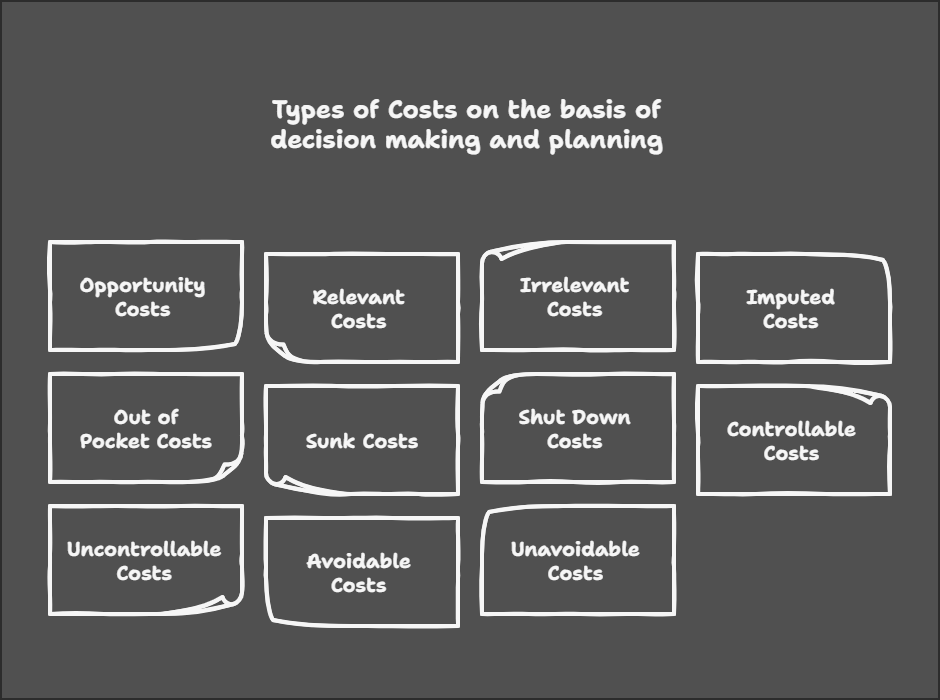

1. Opportunity Costs

-

Definition: Opportunity cost represents the potential benefit that is forgone by choosing one alternative over another. It's the value of the next best alternative use of resources.

-

Example: A company can invest $100,000 in either Project A or Project B. Project A is expected to yield a return of $15,000, while Project B is expected to yield a return of $12,000. The opportunity cost of choosing Project A is the $12,000 return that is forgone by not choosing Project B.

2. Relevant Costs

-

Definition: Relevant costs are those costs that are directly affected by a specific management decision. They are also known as avoidable costs or differential costs.

-

Example: A company is deciding whether to manufacture a component in-house or outsource it. The relevant costs are the costs that would be incurred only if the company manufactures the component in-house (e.g., direct materials, direct labor, variable overhead). Fixed overhead that will be incurred regardless of the decision is not relevant.

3. Irrelevant Costs

-

Definition: Irrelevant costs are costs that are not directly affected by a specific management decision. They are also known as sunk costs, committed costs, or overhead (if the overhead doesn't change with the decision).

-

Example: A company is deciding whether to replace an old machine with a new one. The cost of the old machine (its book value) is a sunk cost and therefore irrelevant to the decision. The relevant costs are the future costs associated with each option (e.g., the cost of the new machine, the operating costs of both machines).

4. Imputed Costs

-

Definition: Imputed costs are hypothetical costs that are specifically calculated outside the formal accounting system for decision-making purposes. They do not involve actual cash outlays.

-

Examples:

- Interest on Internally Generated Funds: The cost of using the company's own funds for a project, rather than investing them elsewhere.

- Rental Value of Own Property: The cost of using the company's own building for business operations, rather than renting it out.

5. Out-of-Pocket Costs

-

Definition: Out-of-pocket costs are costs that involve a direct cash outlay.

-

Example: The cost of raw materials purchased for production, salaries paid to employees, and rent paid for office space are all out-of-pocket costs.

6. Sunk Costs

-

Definition: Sunk costs are costs that have already been incurred and cannot be recovered. They are the result of past decisions and are irrelevant to future decisions.

-

Sunk Cost Dilemma: Sometimes, individuals or organizations may be reluctant to abandon a project or investment, even if it is failing, because they have already invested significant resources in it. This is known as the "sunk cost fallacy." Rational decision-making requires ignoring sunk costs and focusing on future costs and benefits.

-

Example: A company invested $100,000 in developing a new product. Market research now suggests that the product is unlikely to be successful. The $100,000 is a sunk cost. The company should decide whether to continue development based on the future costs and potential future revenues, not on the money already spent.

7. Shutdown Costs

-

Definition: Shutdown costs are the costs that a company must incur if it shuts down a department, product line, or even the entire business.

-

Examples:

- Severance pay for employees.

- Lease cancellation penalties.

- Costs of disposing of assets.

- Security and maintenance costs for a closed facility (e.g., guard's salary, property taxes).

-

Use in Decision-Making: Shutdown costs are important when deciding whether to continue operating or shut down. They should be compared to the costs of continuing operations and the potential future revenues.

8. Controllable Costs

-

Definition: A controllable cost is a cost that can be influenced by a specific manager within a given time period. The manager has the authority to make decisions that affect the cost.

-

Example: A production manager can typically control direct material costs and direct labor costs within their department. However, they may not be able to control the depreciation of factory equipment (which might be controlled at a higher level).

9. Uncontrollable Costs

-

Definition: An uncontrollable cost is a cost that cannot be influenced by a specific manager within a given time period.

-

Example: A production manager may not be able to control the cost of factory rent, as this is usually determined by top management or a lease agreement. Similarly, a department manager may not be able to control the allocation of corporate overhead costs.

10. Avoidable Costs

-

Definition: Avoidable costs are costs that can be eliminated by making a specific management decision. If a particular activity or operation is discontinued, the associated avoidable costs will no longer be incurred.

-

Examples:

- Direct Materials: If a company stops producing a particular product, it will no longer incur the cost of the raw materials used to make that product.

No Comments