Types of Budget: Cash Budget and Master Budget

Cash Budget

The cash budget is a critical financial document, often one of the last budgets to be prepared, as it integrates information from various other budgets. It provides a detailed projection of cash inflows and outflows, along with the resulting cash balance, over a specific budget period.

Purpose and Importance:

The primary purpose of a cash budget is to ensure that the business has sufficient cash available to meet its obligations as they arise. It serves as a tool for:

- Liquidity Management: Ensuring sufficient cash is on hand to cover expenses.

- Financial Planning: Identifying potential cash surpluses or shortages, allowing for proactive measures like investments or borrowing.

- Credit Management: Establishing a sound basis for credit policies.

- Capital Expenditure Planning: Determining whether capital expenditures can be financed internally.

- Cash Position Control: Providing a framework for monitoring and controlling the cash position.

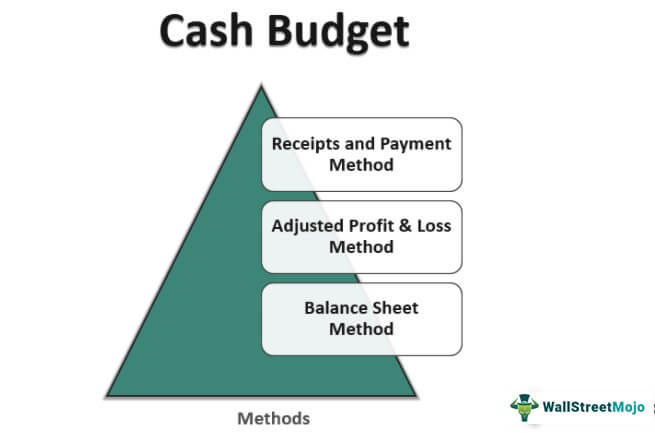

Methods of Preparing a Cash Budget:

There are three main methods for preparing a cash budget:

-

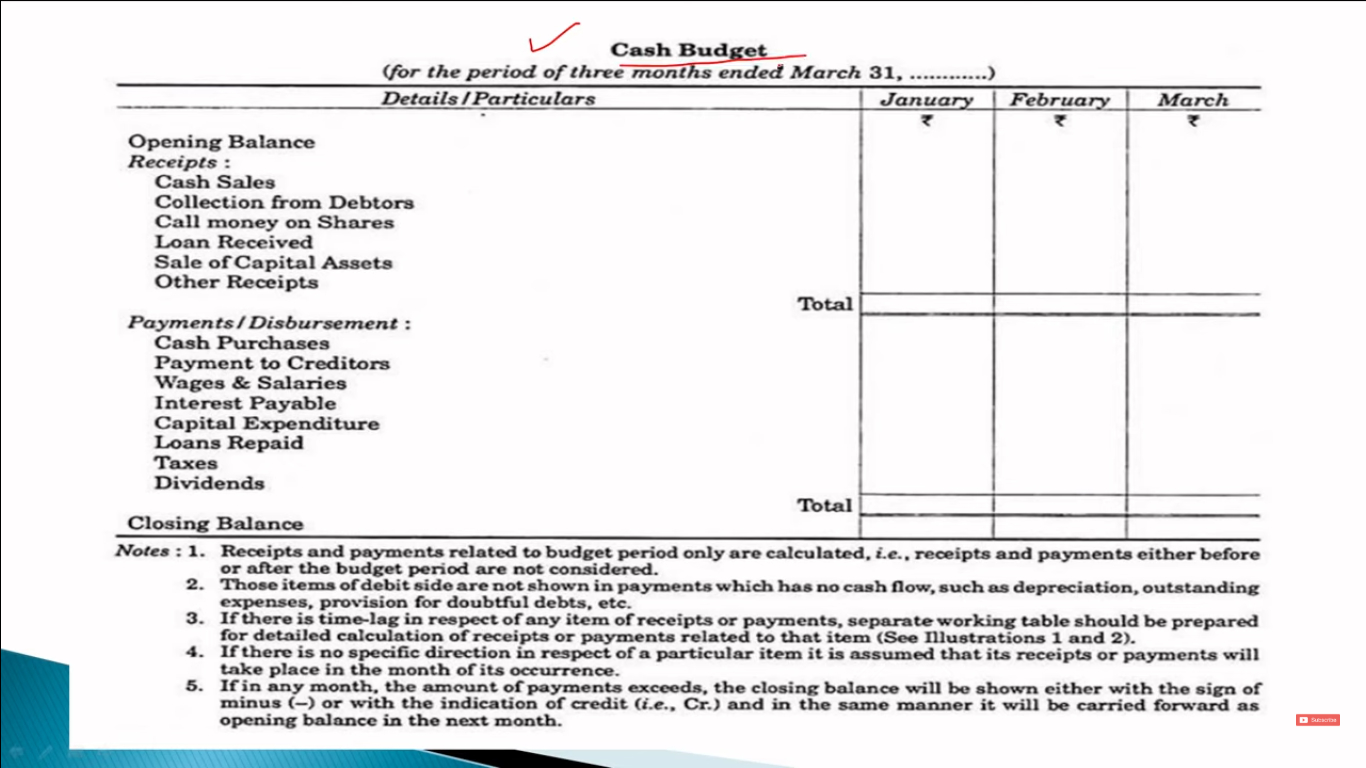

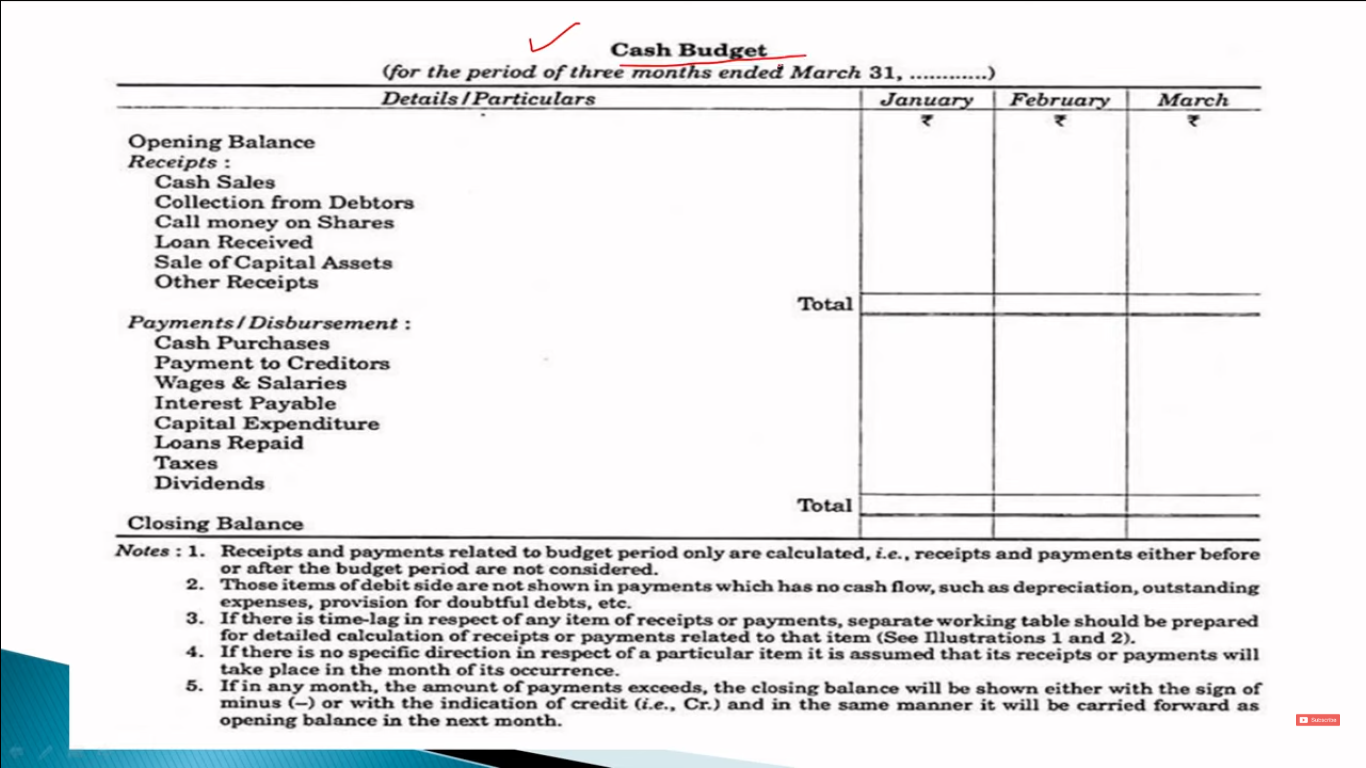

Receipts and Payments Method:

- Short-term focus: This method is generally used for short-term cash forecasts, often monthly or quarterly.

- Detailed approach: It provides a highly detailed view of cash inflows and outflows.

-

Process:

-

Start with the opening cash balance (cash on hand and in the bank).

-

Add all expected cash receipts from various sources (e.g., cash sales, collections from debtors, interest income, asset sales). For credit sales, adjust for the time lag between the sale and cash collection.

-

Deduct all planned cash payments (e.g., raw material purchases, direct labor, operating expenses, capital expenditures, dividends).

-

The result is the closing cash balance for the period.

-

-

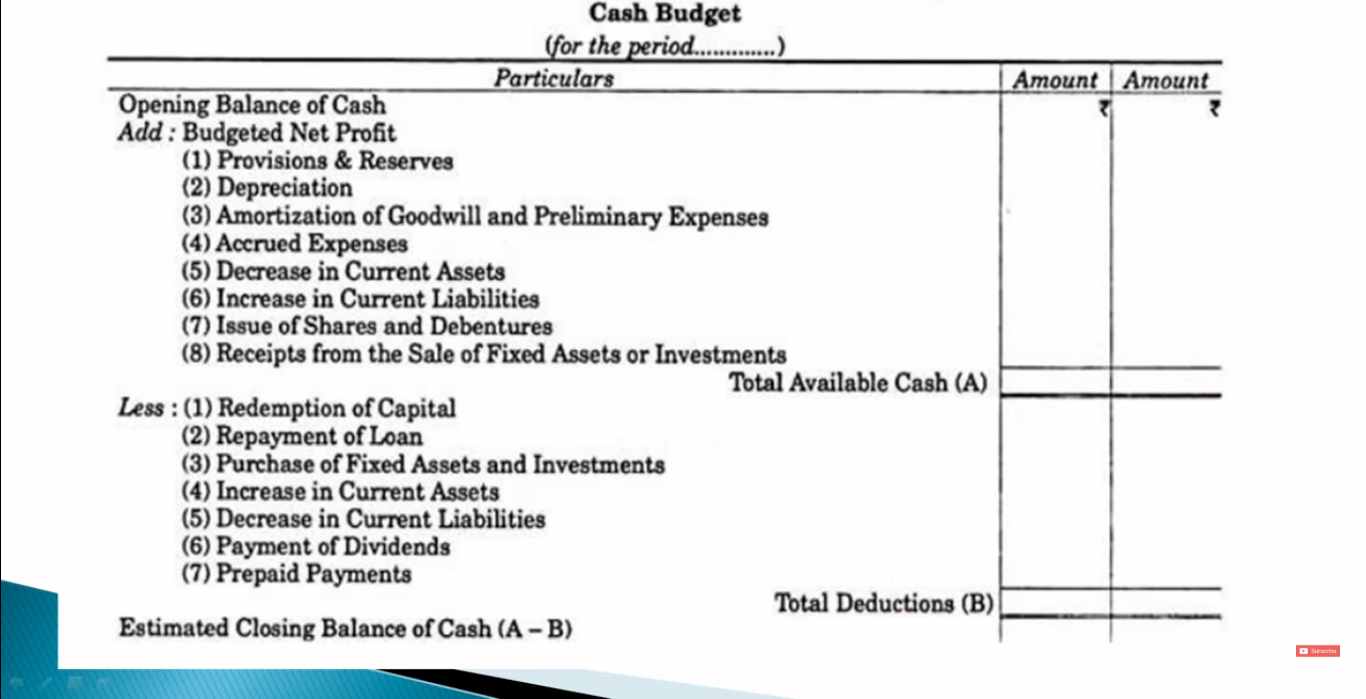

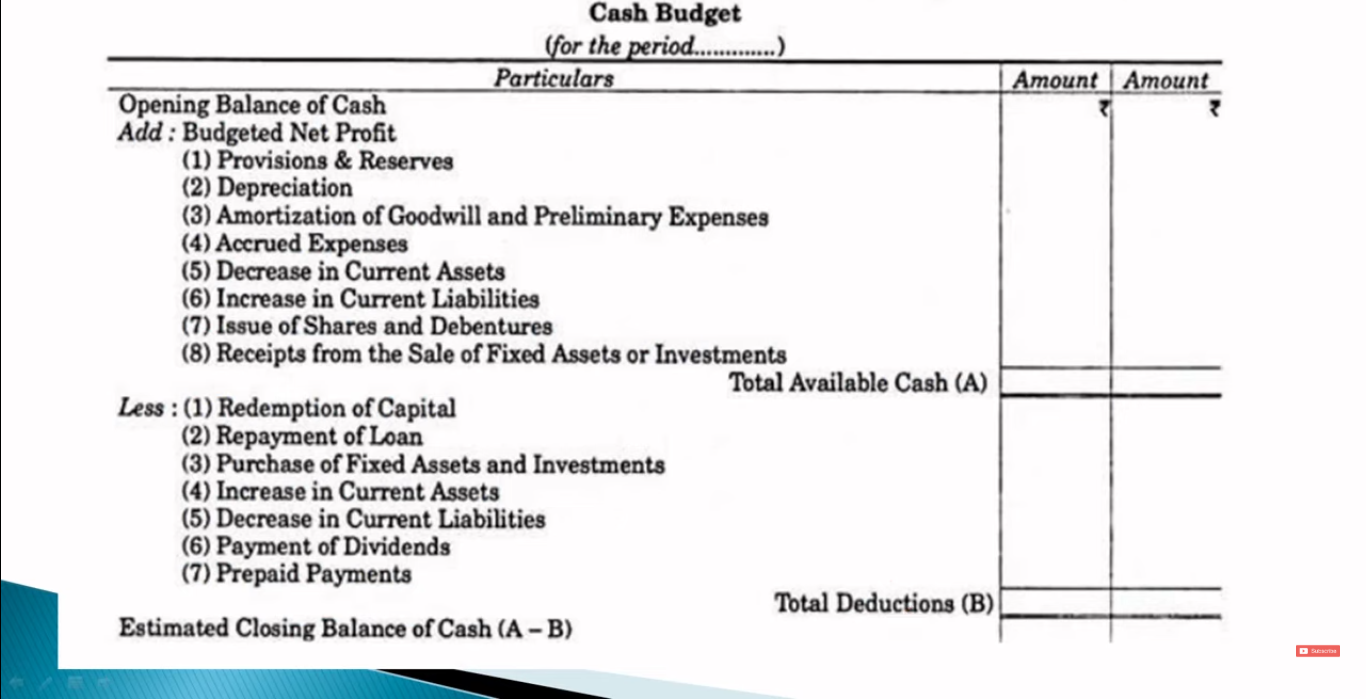

Adjusted Profit and Loss Method (Cash Flow Statement Method):

-

Long-term focus: This method is more suitable for long-term cash flow forecasting.

-

Profit as the starting point: It's based on the idea that profit is the ultimate source of cash in a business.

-

Process:

- Begin with the forecasted profit from the Profit & Loss Account.

- Adjust the profit figure for non-cash items:

- Add back: Depreciation, provisions, stock/WIP adjustments (if decreased), capital receipts, decrease in debtors, increase in creditors.

- Deduct: Dividends, capital payments, increase in debtors, increase in stock/WIP (if increased), decrease in creditors.

- The adjusted profit is considered the closing cash balance.

-

Key difference from Receipts and Payments: This method focuses on adjusting profit for non-cash transactions, while the Receipts and Payments method focuses on actual cash inflows and outflows.

-

-

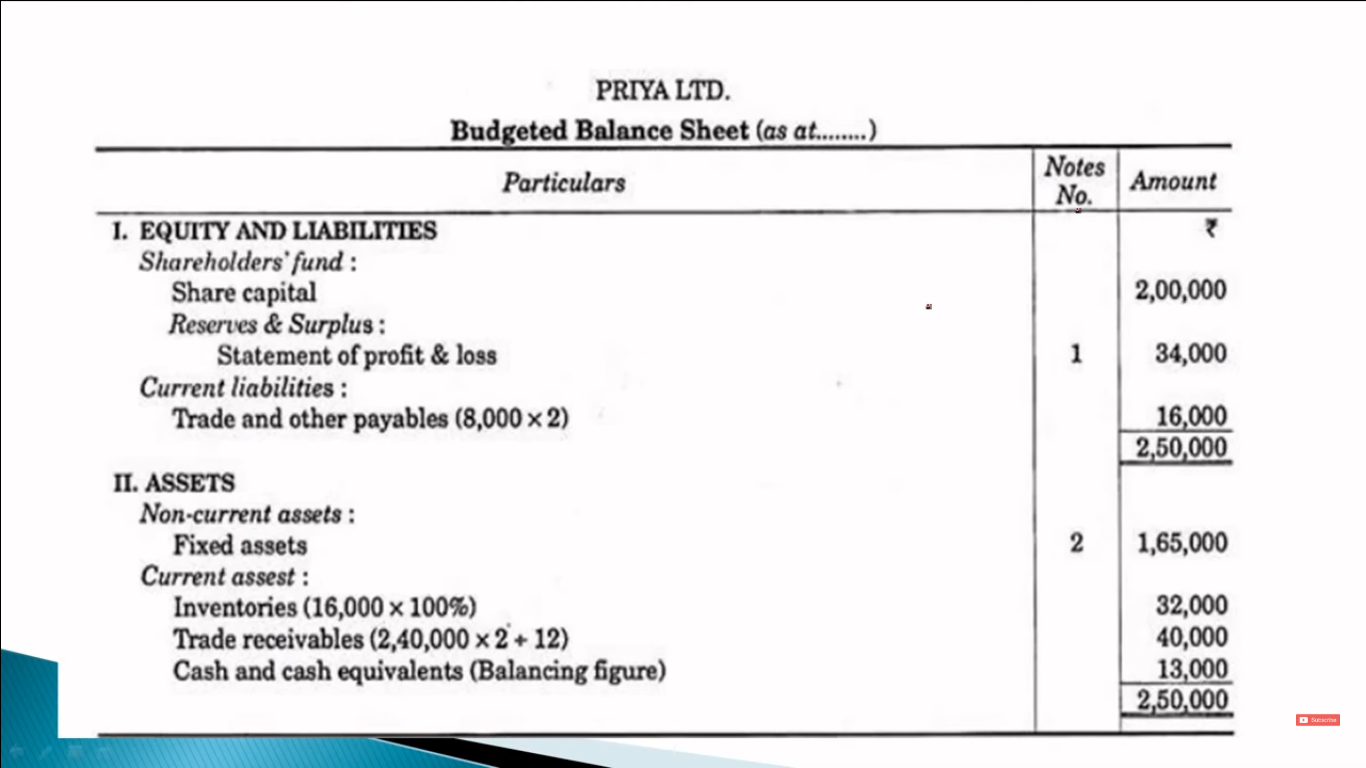

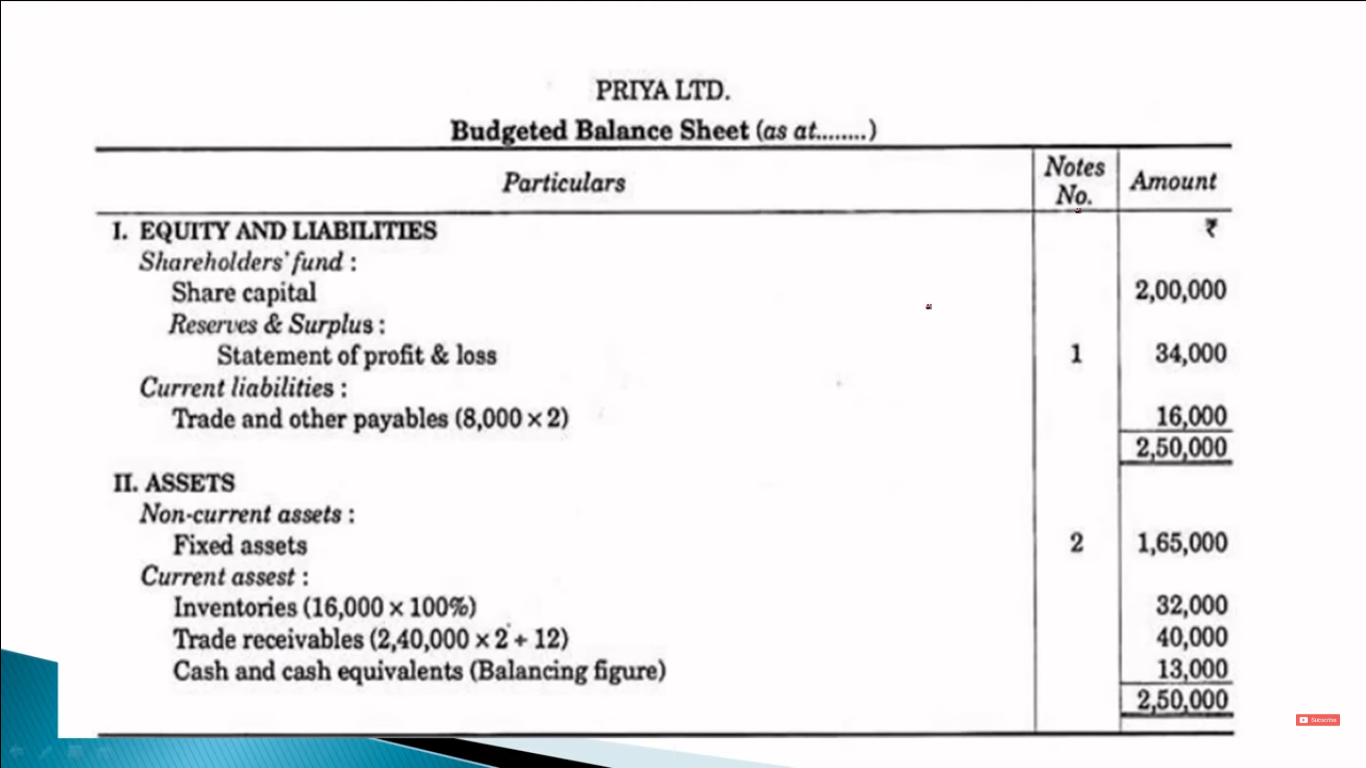

Balance Sheet Method:

- Long-term focus: Similar to the Adjusted Profit & Loss method, it's used for long-term cash forecasting.

- Balance sheet approach: A budgeted balance sheet is prepared, excluding the cash/bank balance.

-

Process:

- Prepare a budgeted balance sheet with all asset and liability accounts except cash/bank.

- Total the asset side and the liability side.

- The difference between the two totals represents the implied cash/bank balance.

- If Liabilities > Assets, the difference is a positive cash balance.

- If Assets > Liabilities, the difference is a bank overdraft (negative cash balance).

Choosing the Right Method:

Choosing the Right Method:

The choice of method depends on the purpose of the cash budget and the time horizon. The Receipts and Payments method is best for detailed short-term cash management, while the other two methods are more appropriate for long-term financial planning.

Master Budget

The master budget is a comprehensive financial plan that consolidates all the individual functional budgets into a single, unified document. It provides a high-level overview of the organization's planned financial performance for a specific period.

Definition:

According to the Chartered Institute of Management Accountants (CIMA), a master budget is:

A summary budget incorporating its component functional budgets and which is finally approved, adopted and employed.

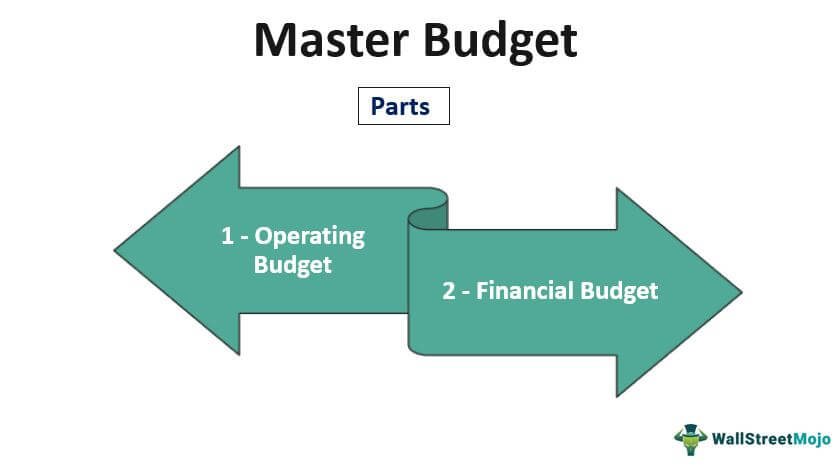

Components of a Master Budget:

A master budget typically consists of two main parts:

- Operating Budget (Budgeted Profit and Loss Statement): This part projects the organization's revenues, expenses, and resulting profit or loss for the budget period.

- Financial Budget (Budgeted Balance Sheet): This part forecasts the organization's financial position at the end of the budget period. It projects the assets, liabilities, and equity of the business.

Preparation and Approval:

- The master budget is usually prepared by the budget director or budget officer, who compiles the information from all the functional budgets.

- The draft master budget is then presented to the budget committee for review and approval.

- After the budget committee's approval, it is submitted to the Board of Directors for final approval.

- Once approved by the Board, the master budget becomes the official financial plan for the organization.

No Comments