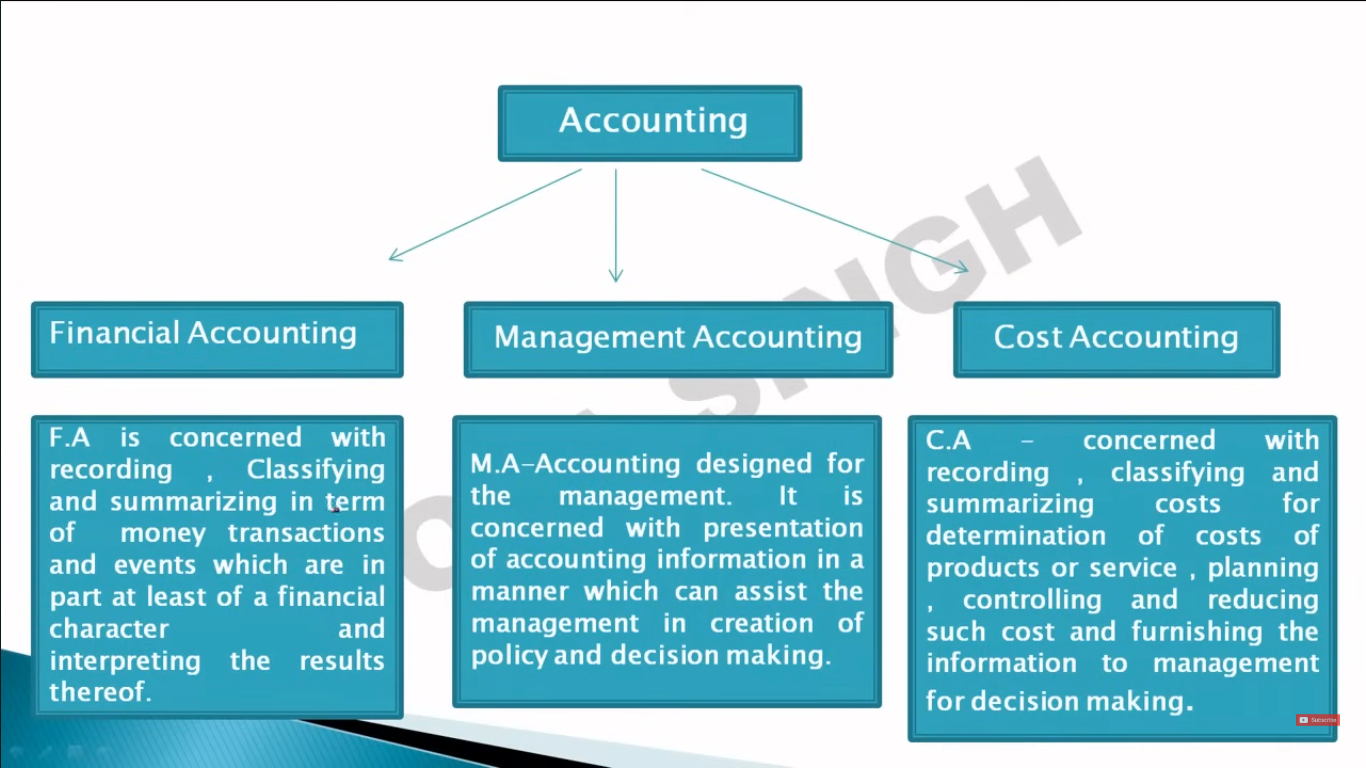

Cost Accounting and Financial Accounting

Types of Accounting

Cost Accounting

- Cost accounting is a crucial part of any accounting system, focusing on measuring costs for managerial decision-making and financial reporting.

- It's the process of accounting for costs, specifically the economic resources used in producing goods or services.

- This involves classifying, recording, and allocating expenditures to determine the cost of products or services, providing information to managers for cost control.

Who Needs Cost Accounting?

Organizations of all types – manufacturing firms, service companies, and non-profit organizations – require some form of cost accounting.

Need for Cost Accounting: Overcoming Limitations of Financial Accounting

Financial accounting, while essential, has limitations that cost accounting addresses:

- Past Data Focus: Financial accounting primarily provides historical data.

- Overall Results: It covers the overall business results, lacking detailed insights.

- Limited Control: It doesn't effectively control resources.

- Insufficient Management Data: It fails to provide adequate data for management functions.

- No Cost Comparison Basis: It doesn't offer a basis for comparing costs.

- Lack of Key Analyses: It doesn't facilitate analyses like Cost-Volume-Profit.

- Hindrance to Efficiency: It may not contribute directly to achieving overall efficiency.

Cost accounting overcomes these limitations by providing detailed, relevant, and timely information for decision-making and control.

Objectives of Cost Accounting

The primary objective is to provide accurate and relevant cost information to management for planning, controlling, and decision-making. Specific objectives include:

- Cost Determination: Determining the cost of products, services, or activities.

- Budgeting and Forecasting: Assisting in preparing budgets and forecasts.

- Pricing Basis: Providing a basis for setting selling prices.

- Cost Savings and Efficiency: Identifying areas for cost savings and efficiency improvements.

- Management Decisions: Supporting management in decisions related to product mix, pricing, and operations.

Cost Accountancy

The Chartered Institute of Management Accountants (CIMA), London, defines Cost Accountancy as:

"The application of costing and cost accounting principles, methods, and techniques to the science, art, and practice of cost control and the ascertainment of profitability. It includes the presentation of information derived therefrom for managerial decision-making."

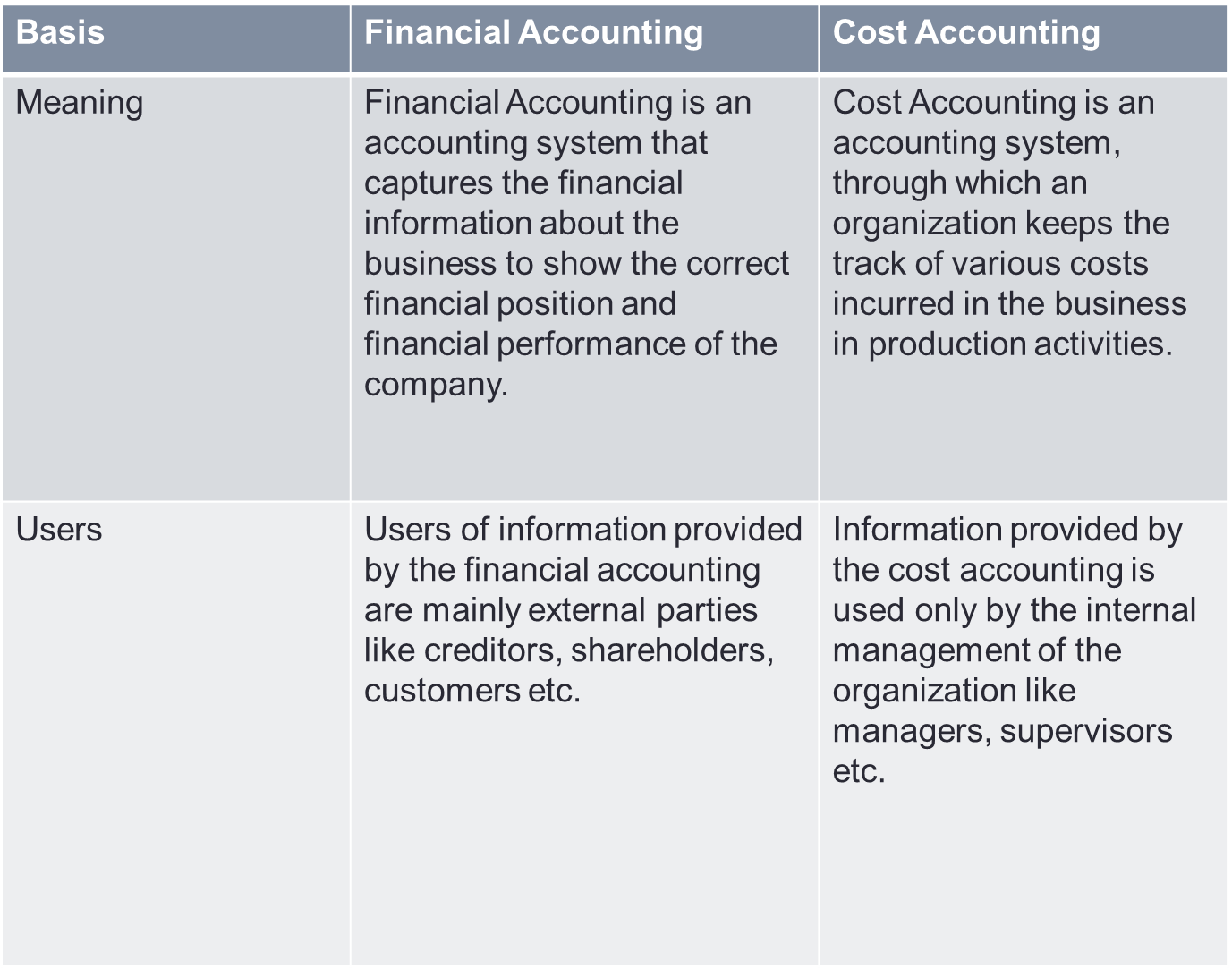

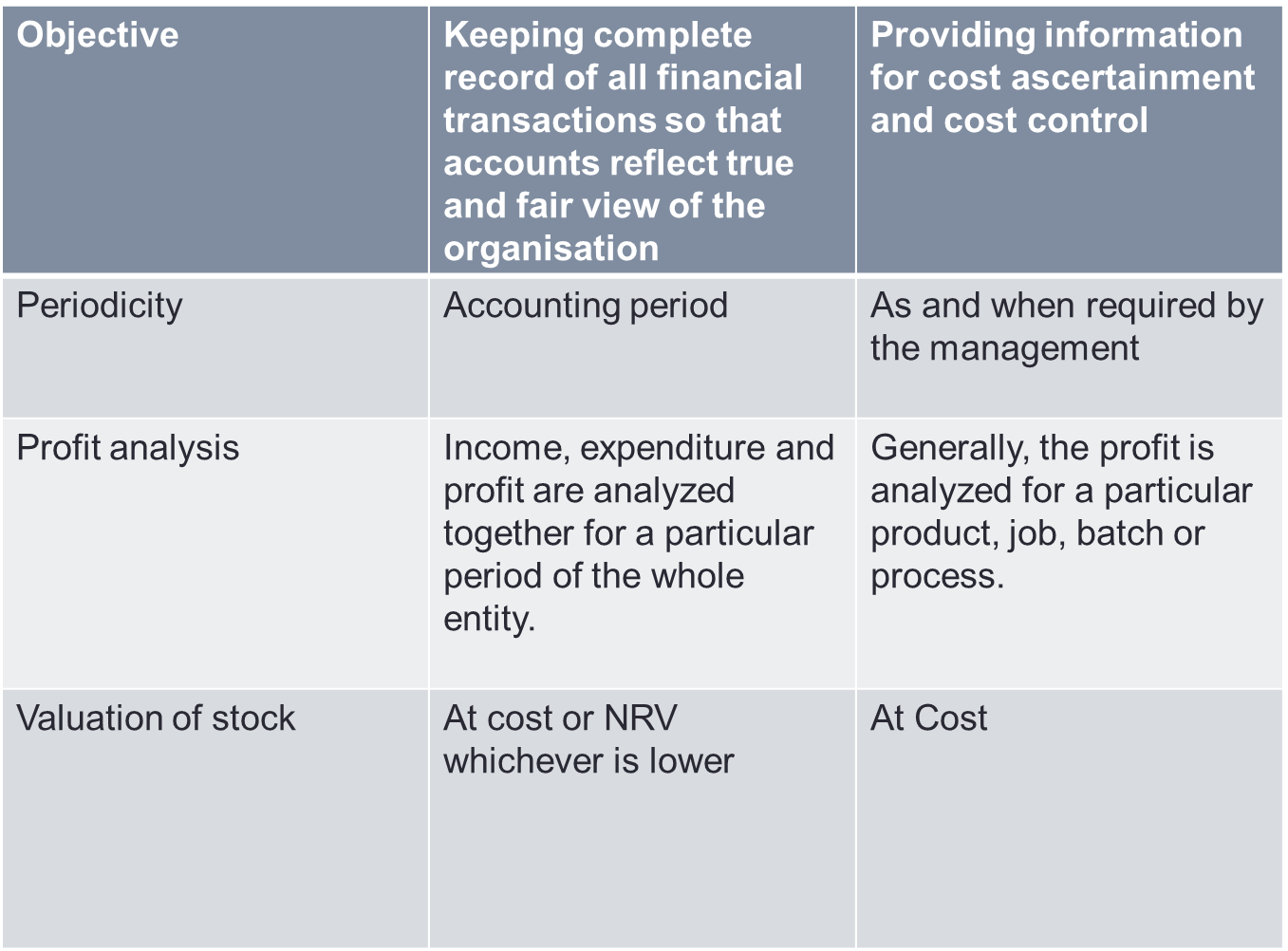

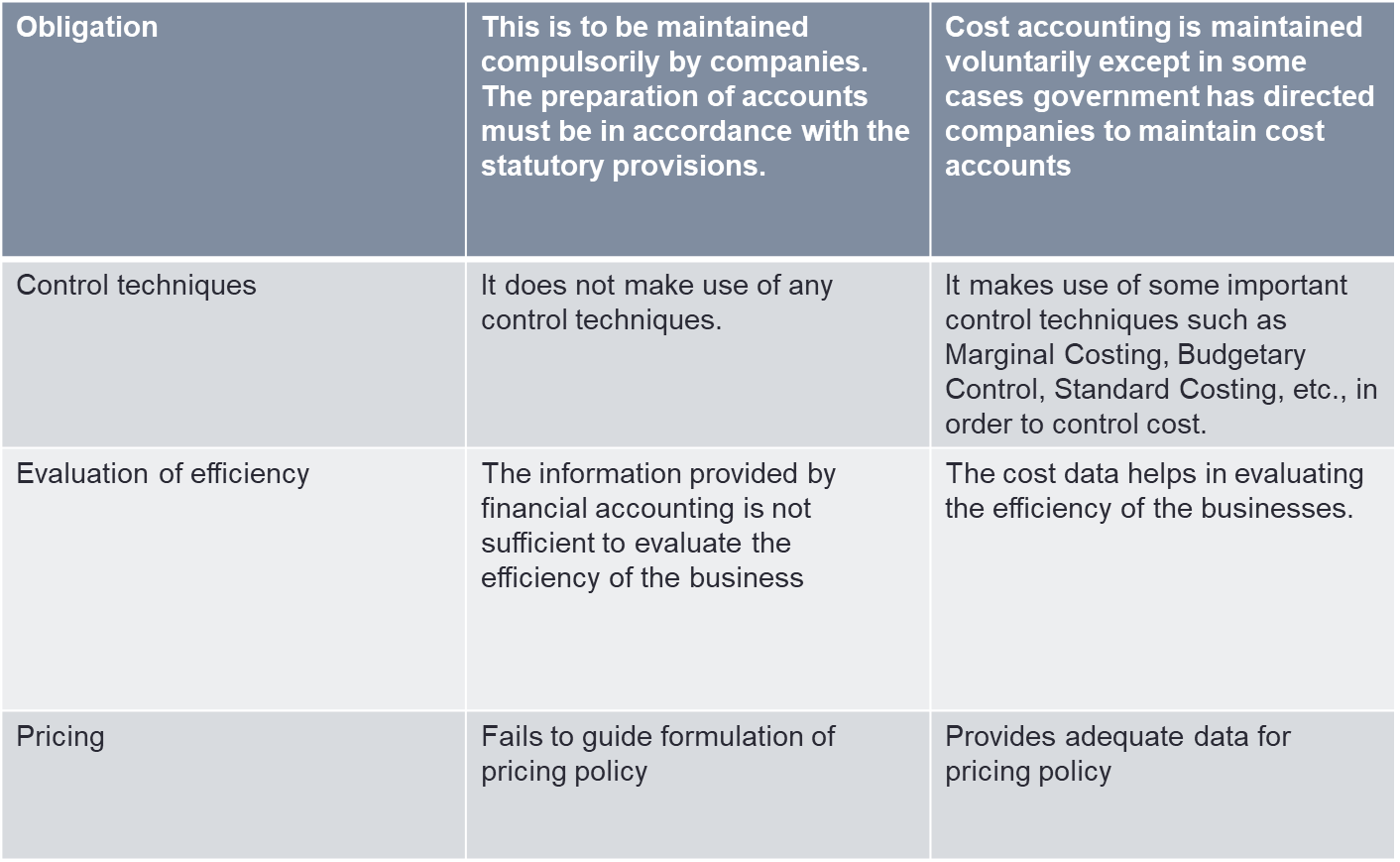

Financial Accounting versus Cost Accounting

No Comments