Credit Ratings

Credit ratings are like grades for borrowers, helping investors assess the risk of lending money. They're crucial in financial markets, guiding investment decisions and impacting borrowing costs.

Introduction to Credit Ratings

- What are they? A credit rating is an evaluation of a borrower's (e.g., a company, government) ability and willingness to repay its debts on time and in full.

- Who uses them? Investors (individuals, institutions), lenders, and issuers (borrowers) all use credit ratings.

- What do they measure? Credit ratings primarily assess creditworthiness or credit risk. Higher ratings indicate lower risk of default (non-payment), while lower ratings suggest higher risk.

- Symbolic Indicator: The document mentions that a credit rating is a symbolic indicator of the rating agency's current opinion.

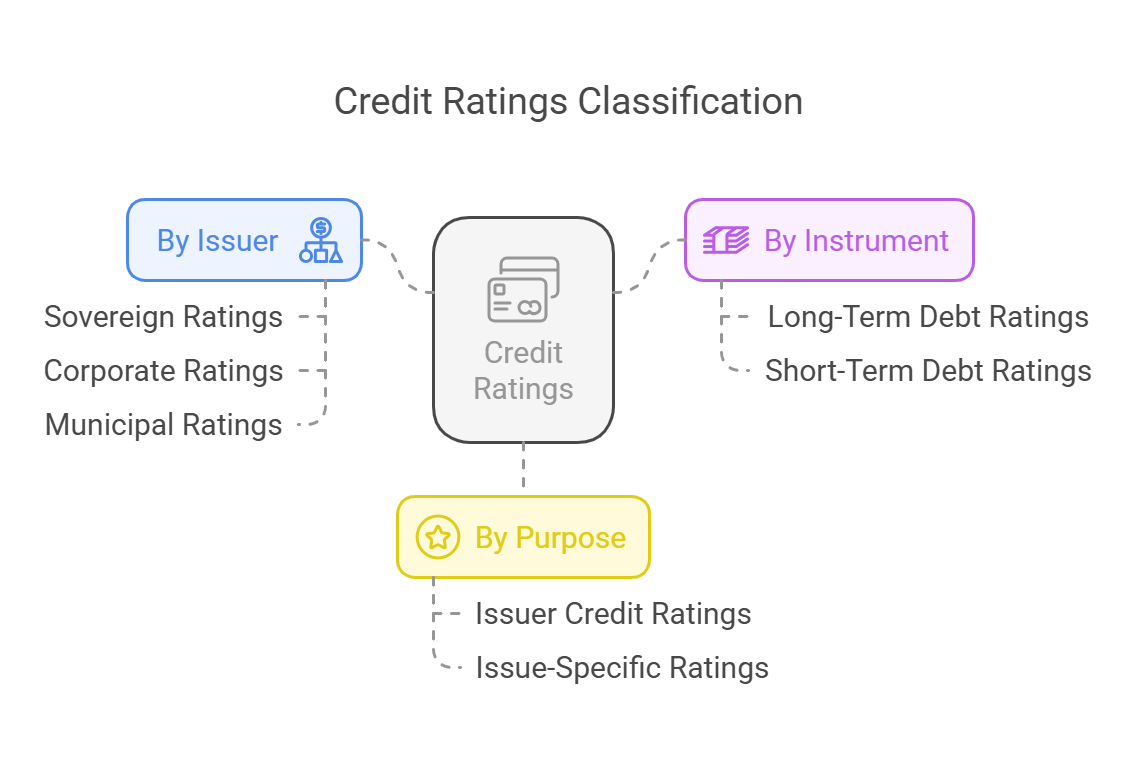

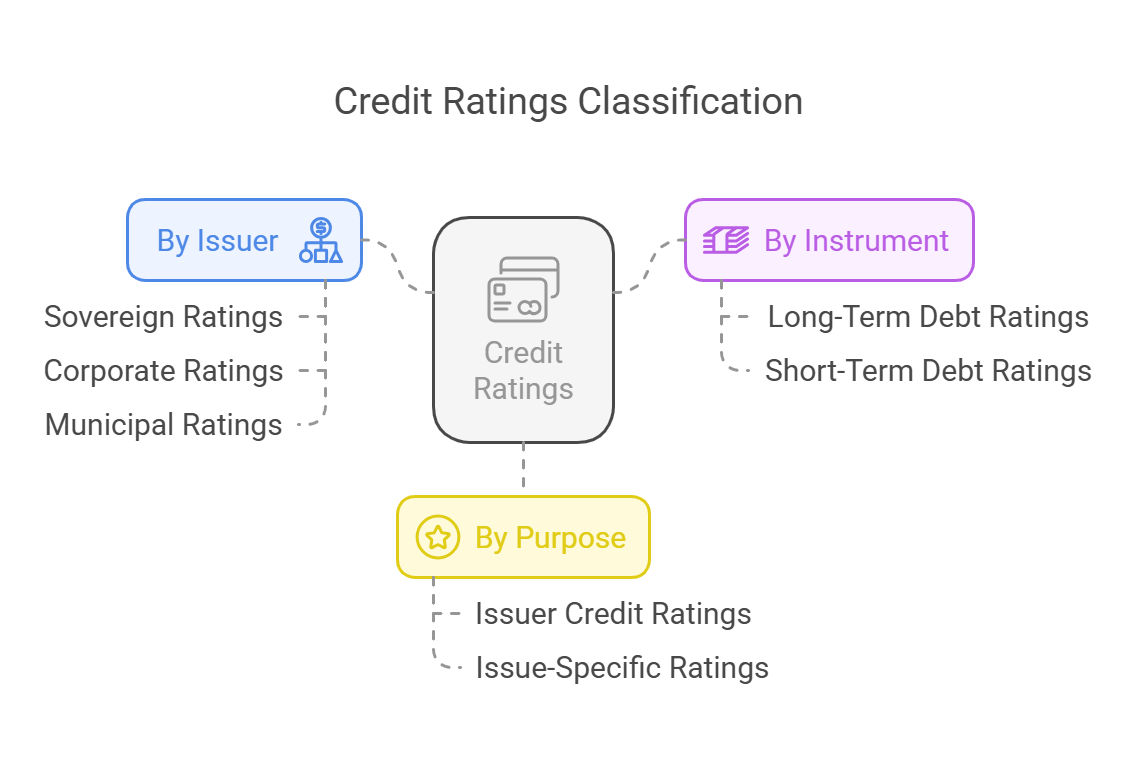

Types of Credit Ratings

Credit ratings are categorized in several ways:

-

By Issuer:

- Sovereign Ratings: Assigned to countries (governments).

- Corporate Ratings: Assigned to companies.

- Municipal Ratings: Assigned to cities, states, or other local government entities.

-

By Instrument:

- Long-Term Debt Ratings: Assess the risk of repayment for bonds, loans, and other long-term obligations.

- Short-Term Debt Ratings: Assess the risk of repayment for commercial paper, short-term notes, and other short-term debt instruments. The document used contained charts from CRISIL for long-term debt like debentures, bonds and preference shares. Short term ratings are listed as commercial papers as shown in page 81.

-

By Purpose:

- Issuer Credit Ratings: Overall creditworthiness of the borrowing entity.

-

Issue-Specific Ratings: Ratings assigned to a particular debt instrument (e.g., a specific bond issue).

Advantages and Disadvantages of Credit Ratings

| Advantage | Disadvantage |

|---|---|

| Informed Investment Decisions | Potential for Conflicts of Interest: Rating agencies are often paid by the entities they rate. |

| Standardized Assessment | Rating Agency Errors: Ratings are opinions, not guarantees, and can be inaccurate. |

| Market Efficiency | Lagging Indicators: Ratings may not reflect the most up-to-date information or market conditions. |

| Lower Borrowing Costs (for good ratings) | Oversimplification: Ratings may reduce complex situations to a single score, losing nuance. |

| Regulatory Compliance | Procyclicality: Ratings agencies may be slow to downgrade issuers during economic booms, then aggressively downgrade during downturns. |

Credit Rating Agencies and Their Methodology

-

Who are they? Independent firms that assess creditworthiness and assign ratings. Examples include:

- Global: Standard & Poor's (S&P), Moody's, Fitch Ratings

- India: CRISIL, ICRA, CARE Ratings

-

Methodology: The document goes over the rating agency methodology. The process generally includes:

- Rating agreement and analytical team assignment

- Meeting with management to review philosophy, plans and future projections.

- Rating committee review

- Communication to the issuer with rations and justifications.

- Dissemination to the public if the issuer accepts rating.

- Review Process: Agencies monitor the rated instruments for any changes that may impact credit quality.

-

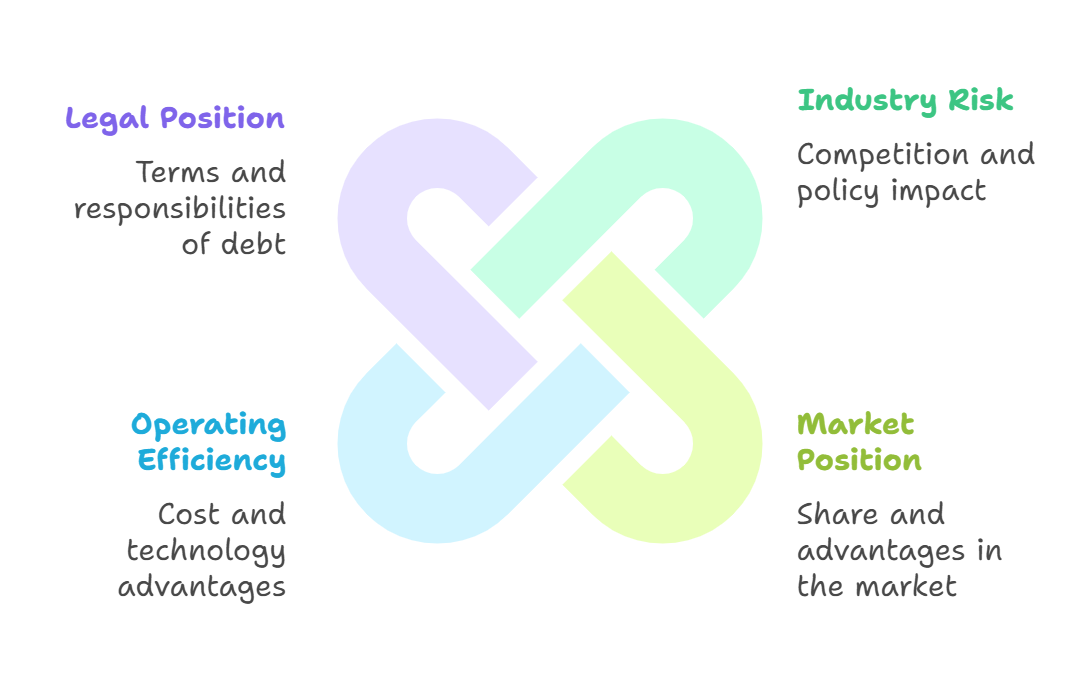

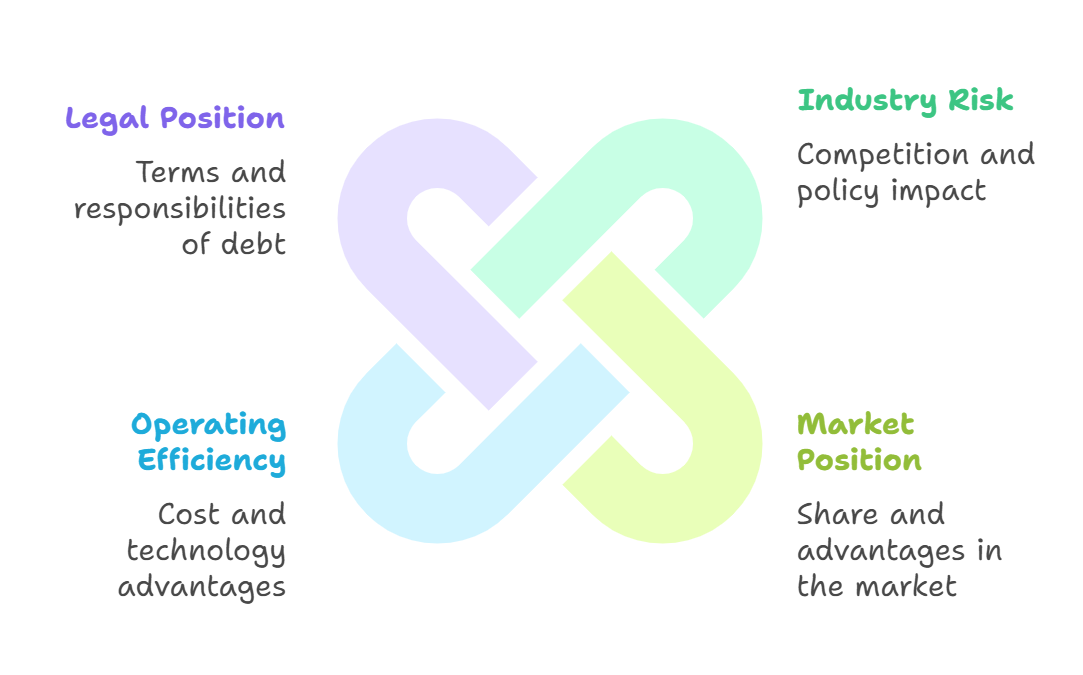

Key Factors Analyzed (Manufacturing Companies):

- Industry Risk: Nature of competition, industry structure, government policies.

- Market Position: Market share, competitive advantages.

- Operating Efficiency: Cost structure, technological advantages.

-

Legal Position: Terms of the debt issue, trustee responsibilities.

-

Key Factors Analyzed (Financial Service Companies):

- Regulatory and competitive environment

- Capital Adequacy

- Asset Quality

- Profitability and financial position

- Interest and Tax Sensitivity

-

International Credit Rating Practices

- Global Standards: International rating agencies (S&P, Moody's, Fitch) use similar methodologies but may have different rating scales.

- Sovereign Ratings: These ratings are crucial for countries because they affect their ability to borrow money internationally and attract foreign investment.

- Country Risk: Agencies consider a country's economic stability, political environment, and regulatory framework.

In summary, credit ratings are essential tools for evaluating credit risk in financial markets. While they offer valuable insights, it's important to understand their limitations and use them in conjunction with other information sources.

No Comments