Housing Finance

A. What is Housing Finance?

Housing finance encompasses a comprehensive range of financial services and products aimed at facilitating the acquisition, construction, improvement, or renovation of residential properties. This can also be refered as Home Loans,

It's more than just a simple loan. It represents a commitment to addressing a fundamental human need. More granularly, it covers:

- Purchase of a Ready Property: Financing the acquisition of an existing house, apartment, or flat.

- Land Acquisition and Construction: Loans to purchase a plot of land and subsequently build a house.

- Construction Alone: Financing the building of a home on land already owned

- Extensions and Improvements: Loans for adding rooms, floors, or improving the condition of an existing property.

- Renovations and Upgrades: Financing for modernizing or enhancing the features of a house or flat.

- Loan Takeover: Refinancing an existing housing loan from another lender, often to secure better terms.

- Special products : Housing finances can be loans only for purchase and for construction of housing.

B. Broader Significance:

- Basic Human Need: Shelter is a fundamental requirement for well-being. Housing provides safety, security, and a sense of belonging.

-

Economic Impact: The housing sector plays a crucial role in the economy through:

- Investment Generation: Housing projects require significant capital investment.

- Employment Creation: Housing construction and related industries provide employment opportunities for a large workforce.

- Multiplier Effect: Stimulates demand in numerous ancillary industries (cement, steel, bricks, timber, electrical, ceramic, sanitary ware, paints, hardware, etc.), boosting economic activity across multiple sectors.

- Backward Linkage: The construction sector ranks among the top sectors in terms of backward linkage, meaning it draws inputs from many other industries.

- Social Welfare: Improved housing quality leads to better living conditions, contributing to the economic well-being and overall quality of life for individuals and communities.

2. The Rise of Housing Finance in India: A Historical Perspective

A. Traditional Approach (Pre-1990s):

- Limited access to institutional finance.

- Individuals relied primarily on personal savings, loans from friends/relatives, or informal sources.

- Housing activity was relatively slow.

B. The Era of Institutionalization (Post-1990s):

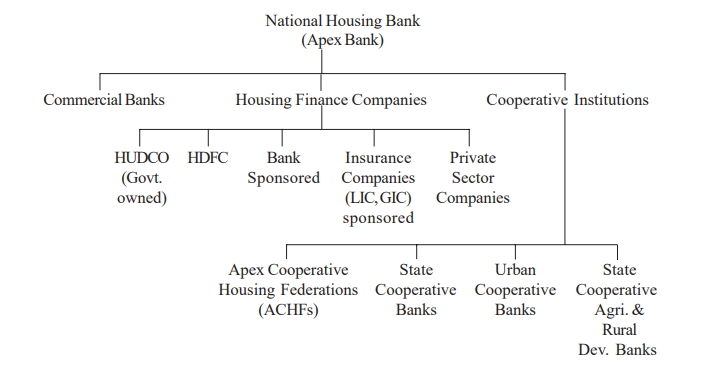

- Key Catalyst: Establishment of the National Housing Bank (NHB) in 1988. NHB served as the apex institution to promote and regulate the housing finance sector.

- Entry of Commercial Banks: Increased participation of commercial banks in housing finance, both directly and through dedicated subsidiaries.

- Emergence of Housing Finance Companies (HFCs): Specialized institutions focused solely on providing housing finance (e.g., HDFC).

-

Impact of Regulatory Changes: The Reserve Bank of India (RBI) played a key role by:

- Including housing finance within the priority sector lending guidelines.

- Directing banks to allocate a certain percentage of their deposits to housing.

- Reducing the risk weighting for housing loans, making them more attractive for banks.

-

Increased Competition & Innovation: The growth in the number of players led to greater competition, resulting in:

- More innovative loan products tailored to diverse customer needs.

- Competitive interest rates.

- Improved service delivery.

C. Continued Evolution:

- Securitization of Housing Loans: NHB introduced securitization as a way for HFCs and banks to mobilize more resources.

- Technological advancements

3. Fixed vs. Floating Interest Rates: Which is Right for You?

A. Fixed Interest Rate:

- How it Works: The interest rate is set at the beginning of the loan and remains unchanged throughout the loan tenure.

-

Pros:

- Predictability: Fixed monthly payments make budgeting easier.

- Protection from Rising Rates: Shields you from potential interest rate increases in the future.

-

Cons:

- Higher Initial Rate: Usually starts at a higher rate compared to floating-rate loans (to compensate the lender for taking on the interest rate risk).

- Missed Opportunity: If interest rates fall, you won't benefit from lower payments.

- Example: A loan with a fixed interest rate of 8% will require you to pay 8% irrespective of interest rate conditions.

B. Floating (Adjustable) Interest Rate:

- How it Works: The interest rate is linked to a benchmark or base rate (e.g., Retail Prime Lending Rate or RPLR) and adjusts periodically (e.g., every 3 months, 6 months, or annually) based on changes in the benchmark.

-

Pros:

- Lower Initial Rate: Typically starts at a lower rate compared to fixed-rate loans.

- Potential Savings: You can benefit if interest rates fall during the loan term.

-

Cons:

- Payment Uncertainty: Monthly payments can fluctuate, making budgeting more challenging.

- Risk of Rising Rates: Payments can increase significantly if interest rates rise.

- Example: If the loan rate was linked to prime lending rate, then any increase or decrease of prime lending rate will affect the housing loan interest rate, however the equated amount will stay the same.

C. Housing Finance Interest Rates: A Comparison

| Feature | Fixed Interest Rate | Floating (Adjustable) Interest Rate |

|---|---|---|

| Interest Rate Stability | Remains constant throughout the loan | Varies based on a benchmark rate |

| Payment Predictability | Fixed monthly payments | Payments fluctuate based on market conditions |

| Initial Rate | Typically higher initial rate | Typically lower initial rate |

| Potential Savings | Limited savings potential | Potential savings if rates fall |

| Risk | Lower risk of rising rates | Higher risk of rising rates |

| Best For | Borrowers seeking budget certainty | Borrowers expecting rates to fall |

| Suitable for those who need | 1. Stability of payments: Some borrowers, especially those with tight budget like stability |

- long term: In long term mortgages like 15 year etc are good to protect from risks. | Suitable for those who | 1. can handle more risk

- short term loans are taken

- may find to increase credit amount in the future. |

Key Points to Remember:

- Fixed Rates provide predictability, which makes budget and savings easy.

- Floating Rates could save you money if rates fall, they introduce uncertainty.

- Long vs Short Term: Long term might find hybrid better and short term with floating, to manage cashflows.

D. Key Factors to Consider When Choosing:

- Interest Rate Expectations: Do you expect interest rates to rise, fall, or remain stable?

- Risk Tolerance: Are you comfortable with fluctuating monthly payments?

- Budgeting Style: Do you prefer predictable payments or are you willing to adjust your budget based on market conditions?

- Loan Term: The longer the loan term, the greater the potential impact of interest rate fluctuations.

- Loan Value: The more value will affect the payments in the future.

- Amount already repaid

- **Hybrid rates: ** Some lenders give an option to the borrowers to avail part of the loan under fixed rate and the balance under variable rate

No Comments