Insurance

Insurance is a financial mechanism where individuals or entities pay regular premiums to an insurance company. This transfers the risk of potentially large, unforeseen financial losses to the insurer, who pools these premiums to create a fund. When a covered loss occurs, the insurer pays out funds to compensate the insured, providing financial security and peace of mind in exchange for a known, smaller cost.

Concept of Insurance

- Risk Transfer: Insurance is fundamentally a mechanism for transferring risk from an individual or entity (the insured) to an insurance company (the insurer).

- Pooling of Risk: Insurers pool premiums from many policyholders to create a fund to pay out claims to those who experience covered losses.

- Financial Protection: It provides financial protection against unforeseen and potentially devastating events, offering peace of mind and stability.

- Consideration The consideration made by the insured to the insurer is called the insurance premium

- Premium: A relatively small payment (the premium) is made to protect against a potentially much larger financial loss.

Classification of Insurance

Insurance can be broadly classified into two major categories:

-

Life Insurance:

- Provides financial protection against loss of life (death benefit) or survival to a certain age (endowment policy).

- Types: Term life, whole life, endowment, unit-linked insurance plans (ULIPs).

-

General Insurance:

- Covers risks to assets, liabilities, and other interests.

- Types: Property insurance (fire, marine), motor insurance, health insurance, liability insurance, etc.

Within these broad categories, there are numerous sub-classifications and specialized insurance policies.

Principles of Insurance

Several fundamental principles underpin the operation of insurance:

| Principle | Explanation |

|---|---|

| Insurable Interest | The insured must have a financial interest in the subject matter of the insurance (e.g., ownership of a property). |

| Utmost Good Faith (Uberrimae Fidei) | Both the insurer and the insured must disclose all material facts truthfully and honestly. |

| Indemnity | The insurer will compensate the insured for the actual loss suffered, up to the policy limits. |

| Contribution | If multiple insurance policies cover the same loss, the insurers share the loss proportionally. |

| Subrogation | After paying a claim, the insurer has the right to pursue any legal remedies the insured had against a third party. |

| Proximate Cause | The loss must be directly caused by a covered peril to be eligible for a claim payment. |

| Mitigation | It requires the insured to take all measures to lower loss from an insured event |

IRDA and Regulatory Norms in India

-

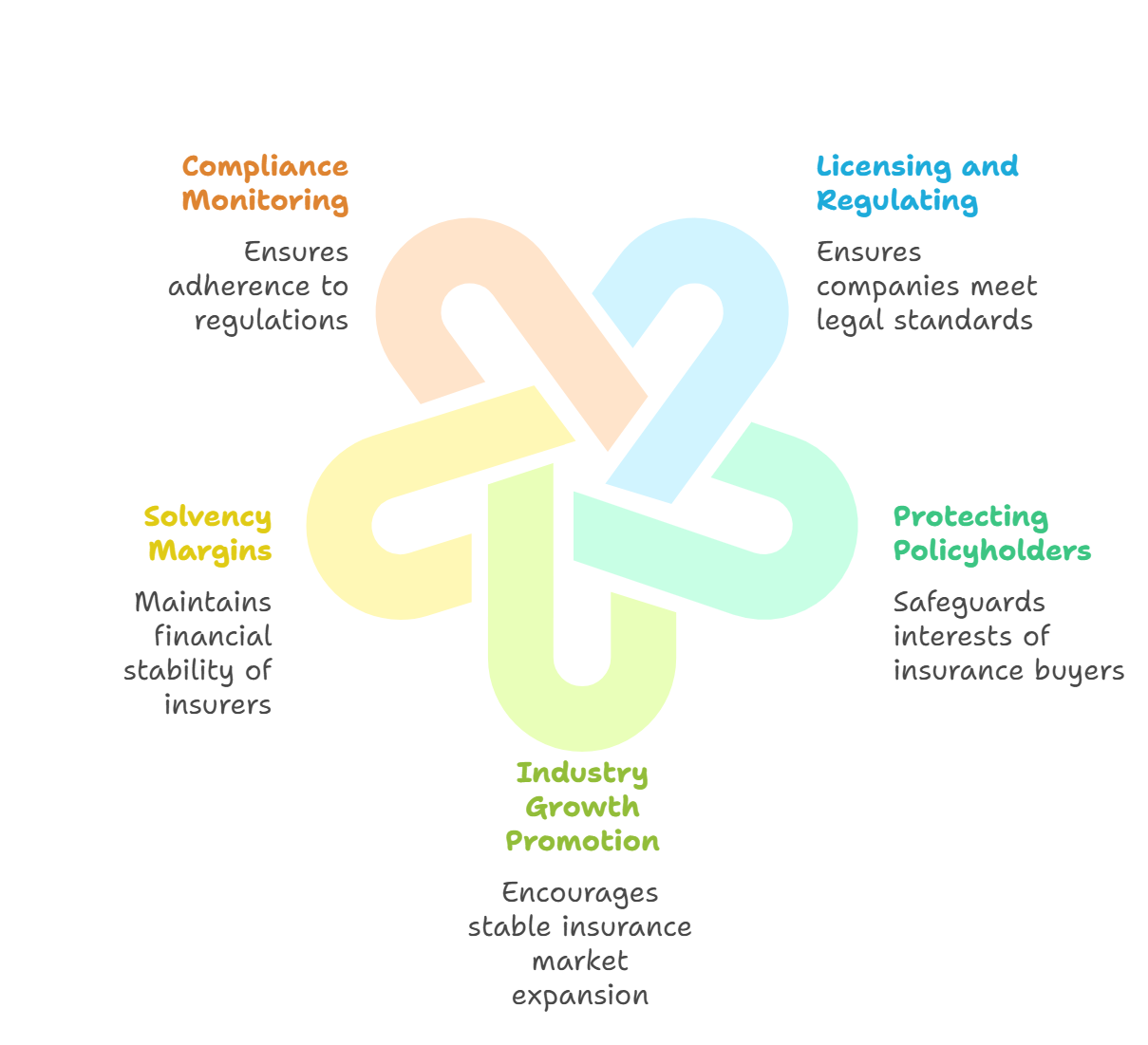

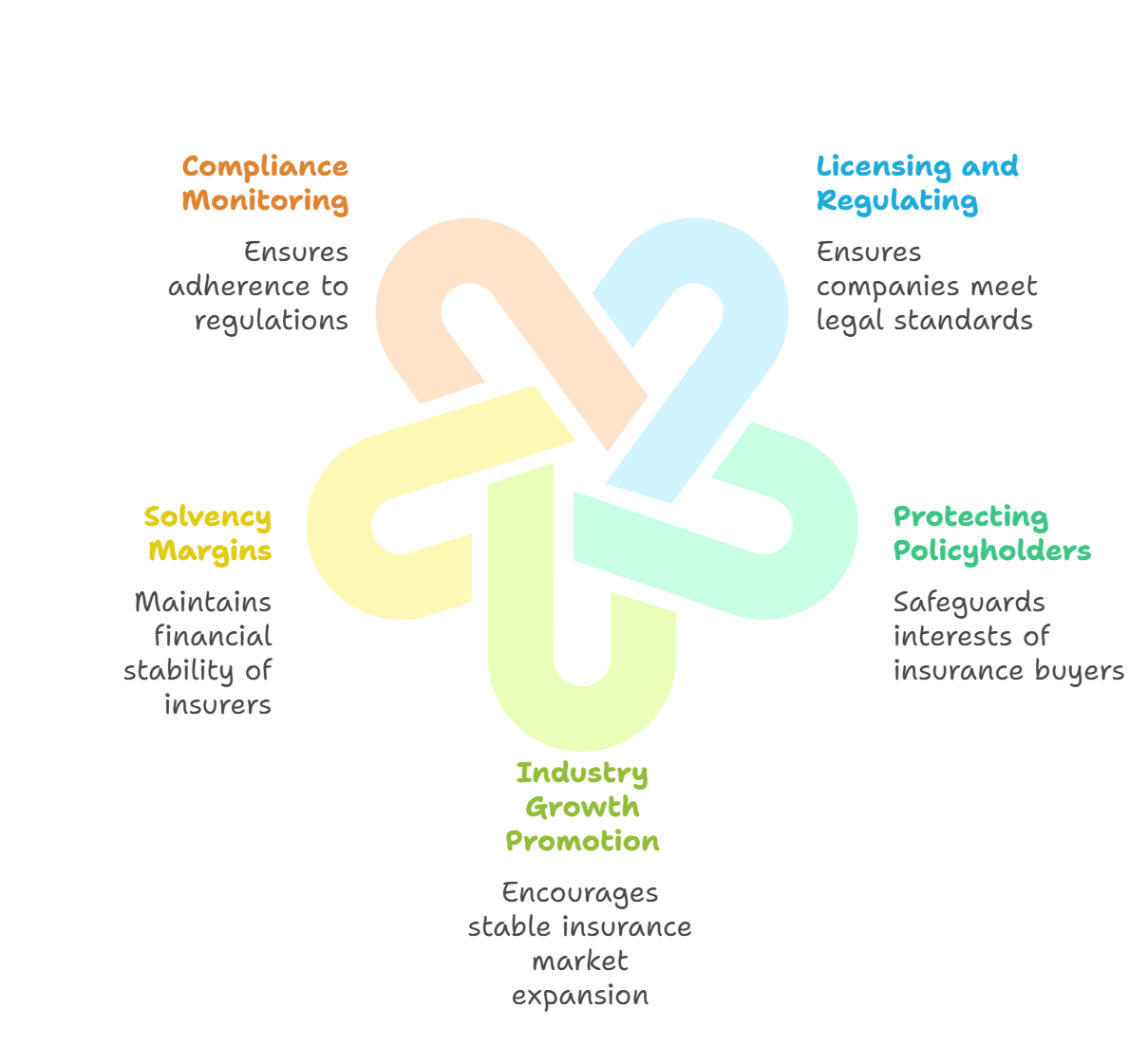

IRDAI: The Insurance Regulatory and Development Authority of India (IRDAI) is the regulatory body for the insurance sector in India.

-

Functions:

- Licensing and regulating insurance companies.

- Protecting the interests of policyholders.

- Promoting the orderly growth of the insurance industry.

- Setting solvency margins and investment regulations for insurers.

- Monitoring and enforcing compliance with regulations.

- Compliance Monitoring

-

Key Regulations:

- Solvency margin requirements (minimum capital required for insurers).

- Investment norms (restricting investments in risky assets).

- Pricing guidelines for insurance products.

- Consumer protection regulations (claims settlement, grievance redressal).

Operation of General Insurance

-

Core Operations:

- Underwriting: Assessing risk and determining premium rates.

- Policy Issuance: Creating and issuing insurance policies.

- Claims Processing: Investigating and settling claims.

- Reinsurance: Transferring risk to other insurers (reinsurers).

- Investment Management: Investing premiums to generate returns.

-

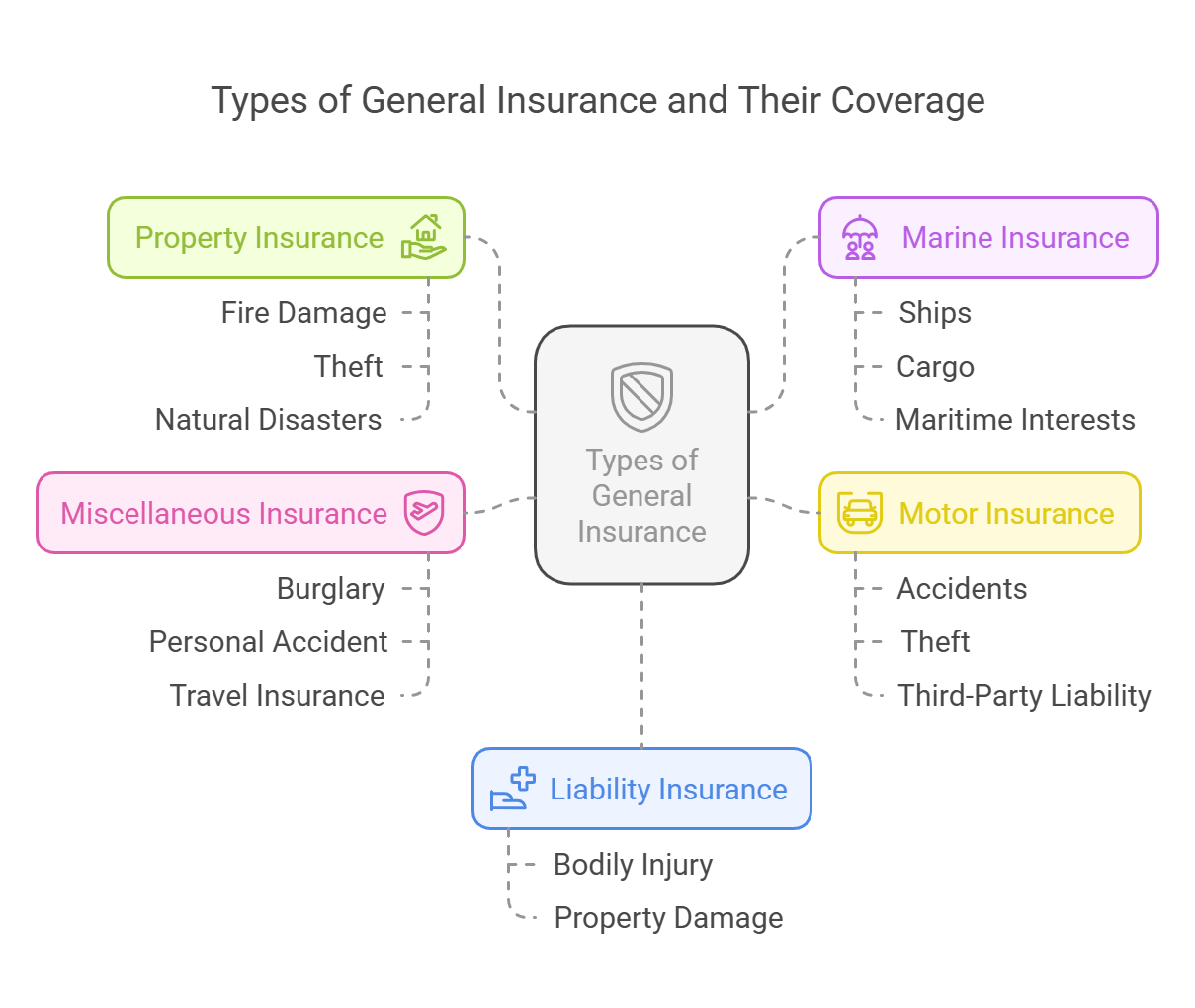

Types of General Insurance:

- Property Insurance: Protects against damage or loss to property due to fire, theft, natural disasters, etc.

- Marine Insurance: Covers loss or damage to ships, cargo, and other maritime interests.

- Motor Insurance: Provides coverage for vehicle accidents, theft, and third-party liability.

- Liability Insurance: Protects against legal claims for bodily injury or property damage caused to others.

- Miscellaneous Insurance: Covers various other risks, such as burglary, personal accident, and travel insurance.

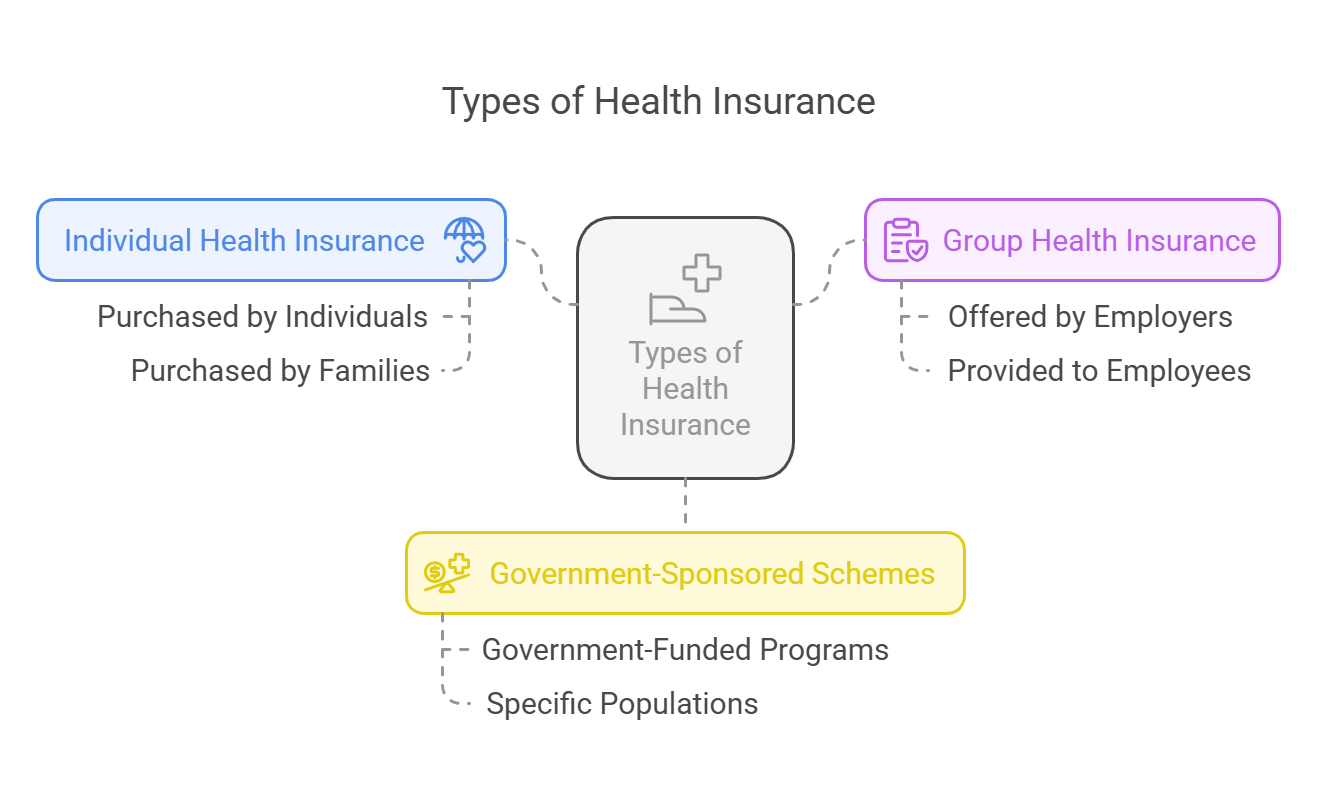

Health Insurance

-

Purpose: Provides coverage for medical expenses arising from illness, injury, or other health conditions.

-

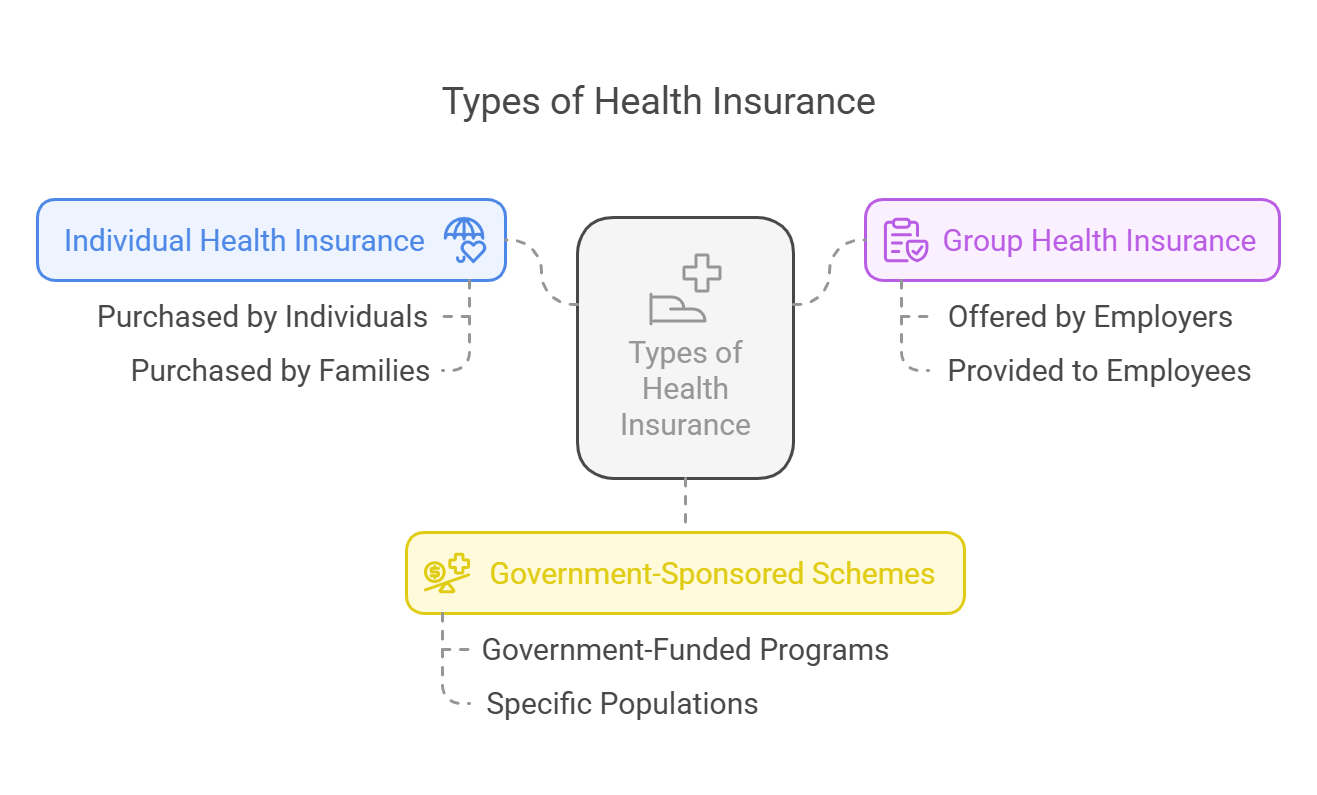

Types:

- Individual Health Insurance: Purchased by individuals and families.

- Group Health Insurance: Offered by employers to their employees.

-

Government-Sponsored Schemes: Government-funded programs providing health insurance to specific populations (e.g., Ayushman Bharat).

-

Key Features:

- Coverage for hospitalization expenses (room rent, doctor's fees, surgery, etc.).

- Coverage for pre- and post-hospitalization expenses.

- Daycare procedures (medical treatments that don't require overnight hospitalization).

- Pre-existing disease coverage (after a waiting period).

- Cashless treatment at network hospitals.

- Reimbursement of expenses at non-network hospitals.

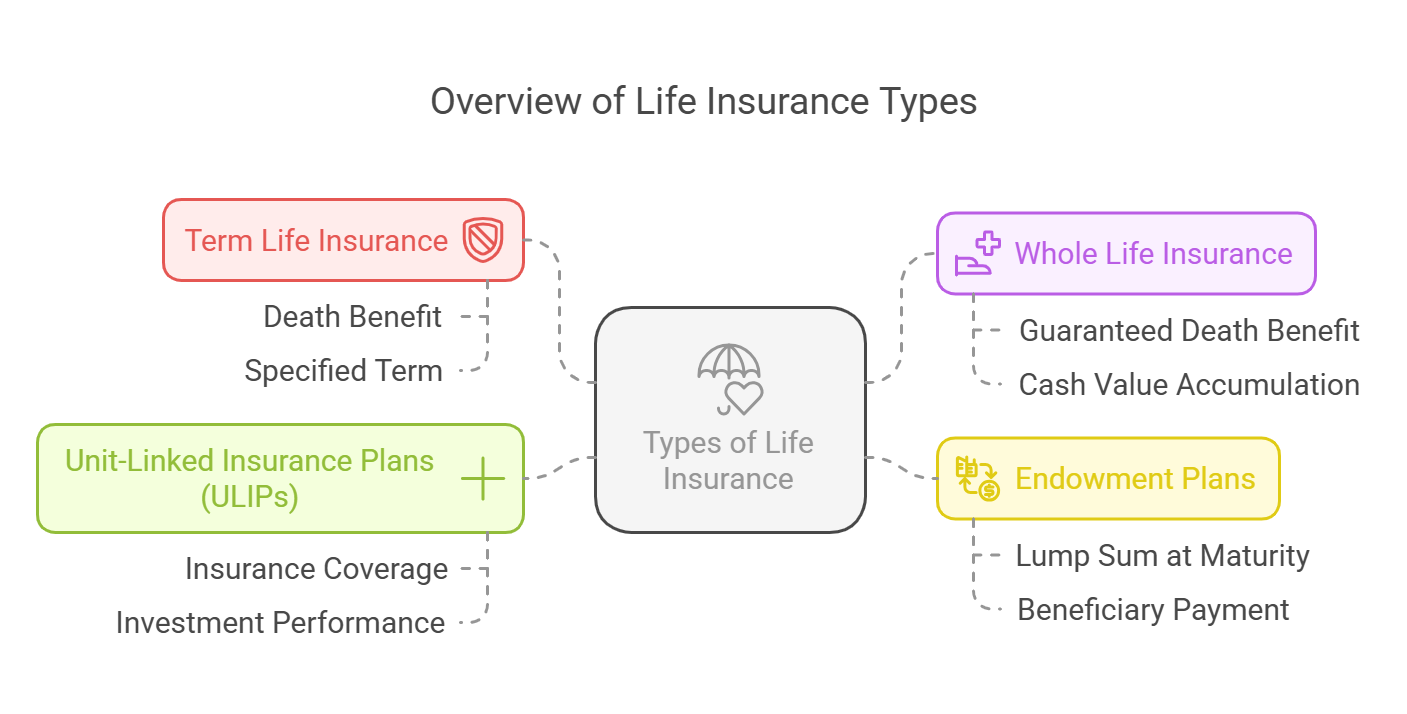

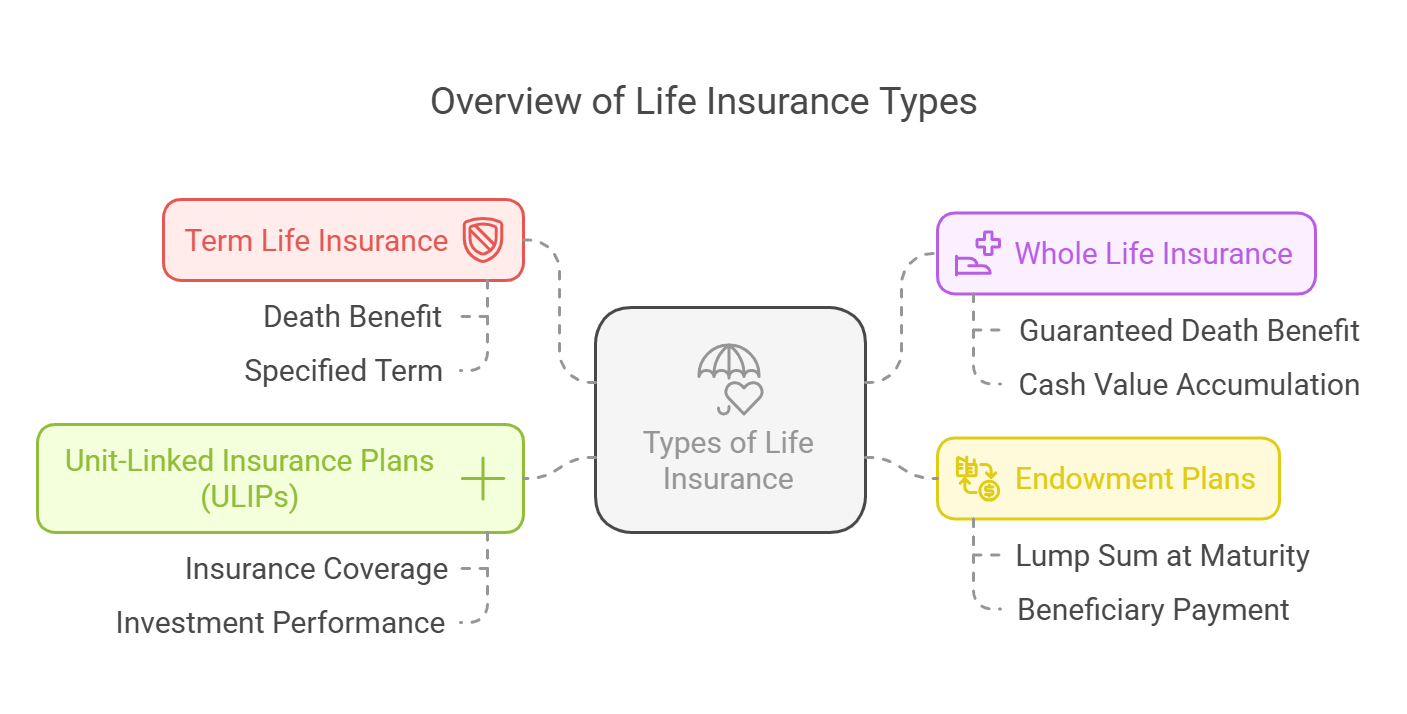

Life Insurance

- Purpose: Provides financial security to the policyholder's family in the event of their death or provides a lump-sum payment upon survival to a certain age.

-

Types:

- Term Life Insurance: Provides coverage for a specified period (the term). Pays a death benefit if the insured dies during the term.

- Whole Life Insurance: Provides lifelong coverage with a guaranteed death benefit and cash value accumulation.

- Endowment Plans: Pays a lump sum to the insured if they survive to a specified maturity date or to their beneficiaries if they die before the maturity date.

-

Unit-Linked Insurance Plans (ULIPs): Combines insurance coverage with investment in market-linked funds. The policy's value depends on the performance of the underlying investments.

-

Key Features:

- Death benefit (sum assured)

- Premium payment options (regular, single)

- Policy term

- Riders (additional benefits like accidental death or critical illness coverage)

- Tax benefits.

No Comments