Hire Purchase, Factoring, and Forfaiting

1. Hire Purchase (HP)

Concept: Buying an asset over time with installments, where ownership transfers after all payments are made. The math involves calculating installments, interest, and rebates. Terms:

- Cash Price: The price if you bought the asset outright with cash.

- Down Payment (DP): The initial payment made at the beginning.

- Installment: The fixed amount paid regularly (monthly, quarterly, etc.).

- Number of Installments (n): How many installments you have to pay.

- Hire Purchase Price (HPP): The total amount you pay under the hire purchase agreement (DP + Total Installments).

- Interest: HPP - Cash Price

Key Calculations:

- Total Installments = Installment Amount * Number of Installments

- Hire Purchase Price (HPP) = Down Payment + Total Installments

- Interest Charged = Hire Purchase Price – Cash Price

Arrangement:

- Buyer (Hirer) selects an asset (e.g., car, appliance).

- Buyer and seller (or finance company) agree on the cash price, down payment, installment amount, and the number of installments.

- Buyer pays the down payment and takes possession of the asset.

- Buyer pays installments according to the agreement.

- Once all installments are paid, ownership transfers to the buyer.

2. Factoring

Concept: Selling your accounts receivable (invoices) to a third party (the factor) to get immediate cash. This helps improve cash flow and reduces the burden of collections.

Terms:

- Receivables (Book Debts): Money owed to your business by customers who bought goods or services on credit.

- Factor: The financial institution or company that buys your receivables.

- Advance Rate: The percentage of the receivables' value that the factor pays upfront (e.g., 70-80%).

- Factor's Fee (Discount/Commission): The charge the factor takes for its services (expressed as a percentage).

- Factor Reserve: The portion of the receivable value that the factor holds back until the customer pays (to cover potential bad debts or adjustments).

Key Calculations:

- Advance Amount = Receivable Value * Advance Rate

- Amount Paid = Invoice Value * advance rates

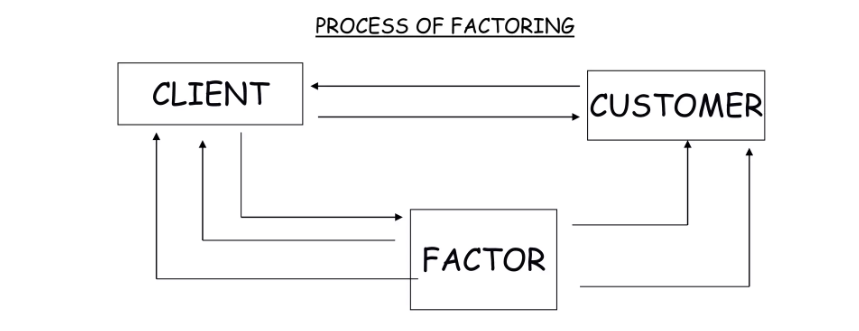

Arrangement:

- A business (Client) makes credit sales to its customers.

- The client enters into a factoring agreement with a Factor.

- The client sells their invoices (receivables) to the Factor.

- The Factor pays the client an advance (a percentage of the invoice value), minus the factor's fee/discount.

- The client's customers pay the Factor directly.

- Once the Factor receives payment from the customers, they pay the remaining balance (if any) to the client (minus the factor reserve, if applicable).

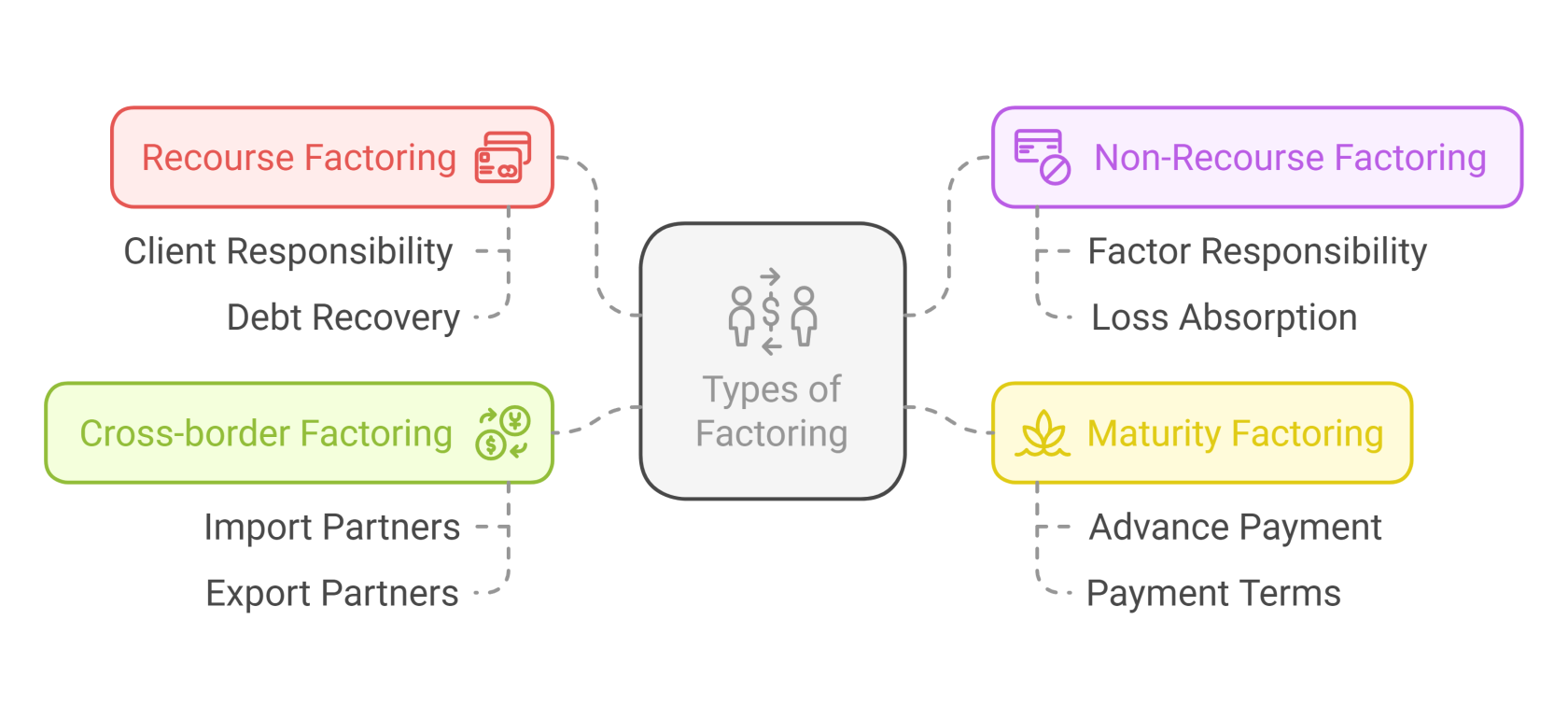

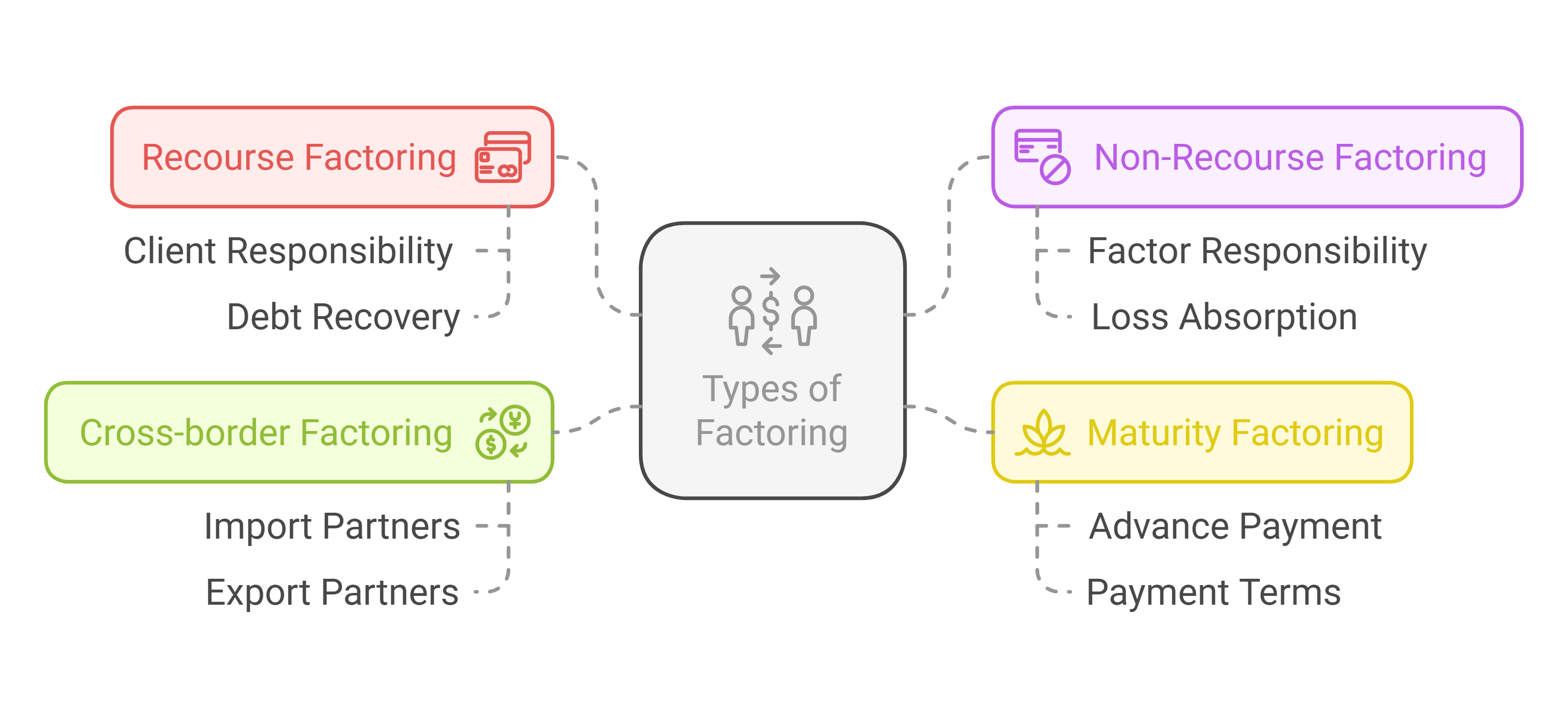

Types of Factoring:

- Recourse Factoring: The client bears the risk of bad debts. If the customer doesn't pay, the factor can "recourse" back to the client to recover the advance.

- Non-Recourse Factoring: The factor assumes the risk of bad debts. If the customer doesn't pay, the factor absorbs the loss.

- Maturity Factoring: Factor does not pay any cash in advance.

-

Cross-border Factoring Involves import and export partners and factoring.

Key Aspects in Factoring

- Scrutiny: Can be individual sale or service oriented.

- Extent of Finance: Usually 75-80% of the total value

- Recourse: Can be with or without

- Sale Administration: Done by factor

- Term: Short Term.

- Charge Creation: Done by assignment of debt.

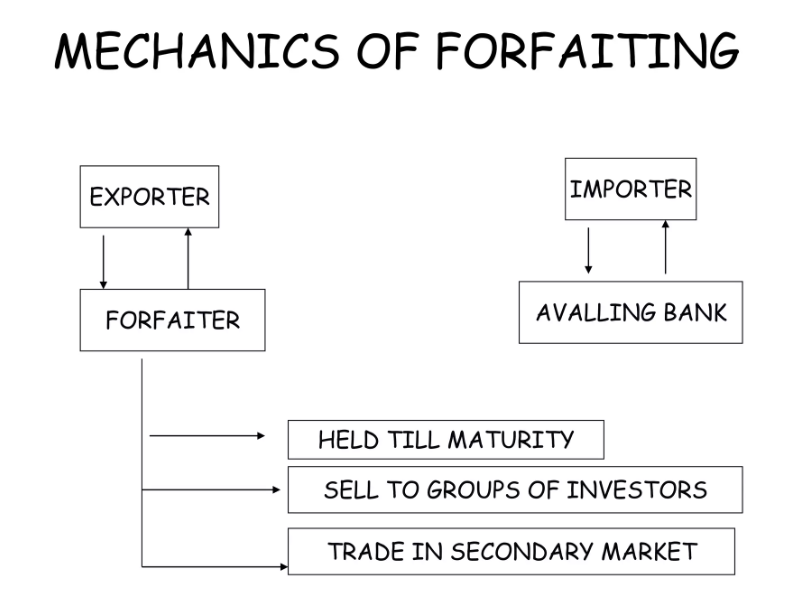

3. Forfaiting

Concept: A specialized type of factoring used in international trade. An exporter sells their medium- to long-term receivables (typically backed by a bank guarantee or letter of credit) to a forfaiter in exchange for immediate cash. This allows the exporter to get paid quickly and eliminates their risk.

Terms:

- Exporter: The seller of goods or services in an international transaction.

- Importer: The buyer of goods or services in an international transaction.

- Forfaiter: The financial institution that buys the exporter's receivables.

- Aval (Bank Guarantee): A guarantee from the importer's bank that payment will be made.

- Discount Rate: The rate used to calculate the discount (the difference between the face value of the receivable and the amount the exporter receives). This includes the forfaiter's profit margin and cost of funds.

Key Calculations:

-

Discount Amount = Receivable Value * Discount Rate * (Term in Years)

-

Amount Paid to Exporter = Receivable Value – Discount Amount

Forfaiting Arrangement:

- An exporter makes a sale to an importer and receives a promissory note or bill of exchange.

- The importer's bank provides an "aval" (guarantee) on the promissory note.

- The exporter sells the note to a forfaiter at a discount.

- The exporter receives immediate cash (Receivable value- Discount fee) from the forfaiter.

- The forfaiter holds the note until maturity or sells it to another investor.

- At maturity, the forfaiter (or subsequent investor) presents the note to the importeror their bank for payment.

Essential Aspects

- Scrutiny: Individual sale transaction focused.

- Extent of Finance: Upto 100%

- Recourse: Without

- Sale Administration: Not Involved.

- Term: Medium Term from 6 months to 5 years.

- Charge Creation: Done by assignment of debt.

Key Differences: Factoring vs. Forfaiting

| Feature | Factoring | Forfaiting |

|---|---|---|

| Term | Short-term | Medium- to Long-Term |

| Geographic Scope | Primarily domestic | Primarily international |

| Risk | Can be with or without recourse | Always without recourse |

| Security | Typically unsecured | Typically secured (bank guarantee/LC) |

| Extent of Finance | Usually 75-80% | Up to 100% |

Comparative Analysis: Bills Discounted, Factoring, and Forfaiting

| Feature | Bills Discounted | Factoring | Forfaiting |

|---|---|---|---|

| 1. Scrutiny | Individual Sale Transaction | Service of Sale Transaction | Individual Sale Transaction |

| 2. Extent of Finance | Upto 75 - 80% | Upto 80% | Upto 100% |

| 3. Recourse | With Recourse | With or Without Recourse | Without Recourse |

| 4. Sales Administration | Not Done | Done | Not Done |

| 5. Term | Short Term | Short Term | Medium Term |

| 6. Charge Creation | Hypothecation | Assignment | Assignment |

Explanation of Features:

-

Scrutiny: This refers to the level of individual assessment done before providing the financial service.

-

Extent of Finance: The percentage of the receivable's value that the financial institution is willing to advance.

-

Recourse: This indicates who bears the risk if the customer doesn't pay.

-

Sales Administration: This refers to whether the financial institution handles the collections and management of the receivables

-

Term: The typical duration of the financing.

-

Charge Creation: This refers to the legal mechanism used to secure the financial institution's interest in the receivable.

In Essence:

-

HP is for buying assets over time, focusing on eventual ownership.

-

Factoring is for improving cash flow by selling short-term invoices.

-

Forfaiting is for getting immediate payment on medium- to long-term export receivables while eliminating risk.

No Comments