Securitization

Securitization is a complex financial process that transforms illiquid assets into marketable securities. It's a key tool for financial institutions to manage risk, improve liquidity, and raise capital.

Concept and Process of Securitization

What is it? Securitization is the process of pooling together similar types of assets (e.g., mortgages, auto loans, credit card receivables) and converting them into securities that can be sold to investors. Essentially, it transforms illiquid assets into liquid investments.

Why is it done?

- Improved Liquidity: Allows originators to free up capital tied up in illiquid assets.

- Risk Management: Transfers credit risk from originators to investors.

- Lower Funding Costs: May enable originators to access cheaper funding sources.

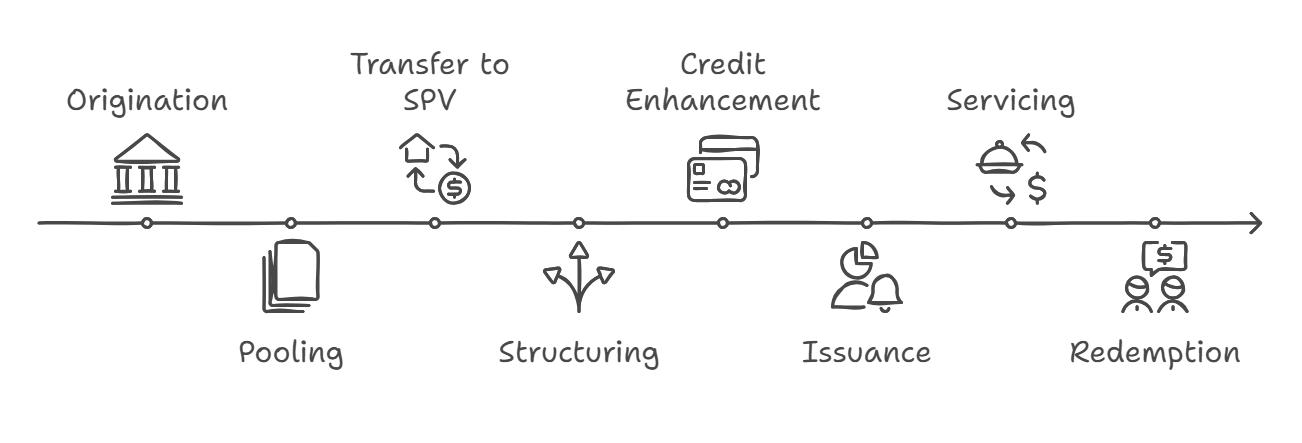

Key Steps in the Securitization Process:

- Origination: A lender (originator) makes loans or generates receivables.

- Pooling: The originator pools together similar assets.

- Transfer to SPV: The assets are transferred to a Special Purpose Vehicle (SPV), a legally separate entity created solely for this transaction.

- Structuring: The SPV structures the assets into different tranches (segments) with varying levels of risk and return.

- Credit Enhancement: Techniques are used to improve the creditworthiness of the securities (see section 2 below).

- Issuance: The SPV issues securities (e.g., asset-backed securities or ABS) to investors.

- Servicing: The originator or a third party (servicer) collects payments from the underlying assets and distributes them to investors.

- Redemption: The securities are gradually paid off as the underlying assets mature.

Credit Enhancement in Securitization

Credit enhancement techniques are used to make securitized assets more attractive to investors by reducing the risk of loss. Some common methods include:

- Senior/Subordinate Structure (Tranching): Creating different classes (tranches) of securities with varying levels of priority in receiving payments. Senior tranches have the highest priority and are the least risky, while subordinate tranches absorb losses first and are riskier.

- Overcollateralization: Including more assets in the pool than the total value of the securities issued. This provides a cushion to absorb potential losses.

- Cash Reserve Funds: Setting aside a cash reserve to cover potential shortfalls in payments.

- Guarantees/Insurance: Obtaining guarantees from third parties or purchasing insurance policies to protect against losses.

Parties to a Securitization Transaction

| Party | Role |

|---|---|

| Originator | Creates the assets (loans, receivables) and initiates the securitization process. |

| SPV | Special Purpose Vehicle - A legally separate entity that holds the assets and issues securities. |

| Investors | Purchase the securities issued by the SPV. |

| Servicer | Collects payments from the underlying assets and distributes them to investors. |

| Credit Enhancer | Provides guarantees or other forms of credit support to improve the creditworthiness of the securities. |

Instruments of Securitization

- Pass-Through Certificates (PTCs): Securities that represent a direct claim on the cash flows generated by the underlying assets. Investors receive a proportional share of the payments. These transfer most of the risks to the investor.

- Pay-Through Certificates: Repackages cashflows and reinvests to configure it in an organized way for a fixed date, even if its not matched to original maturities.

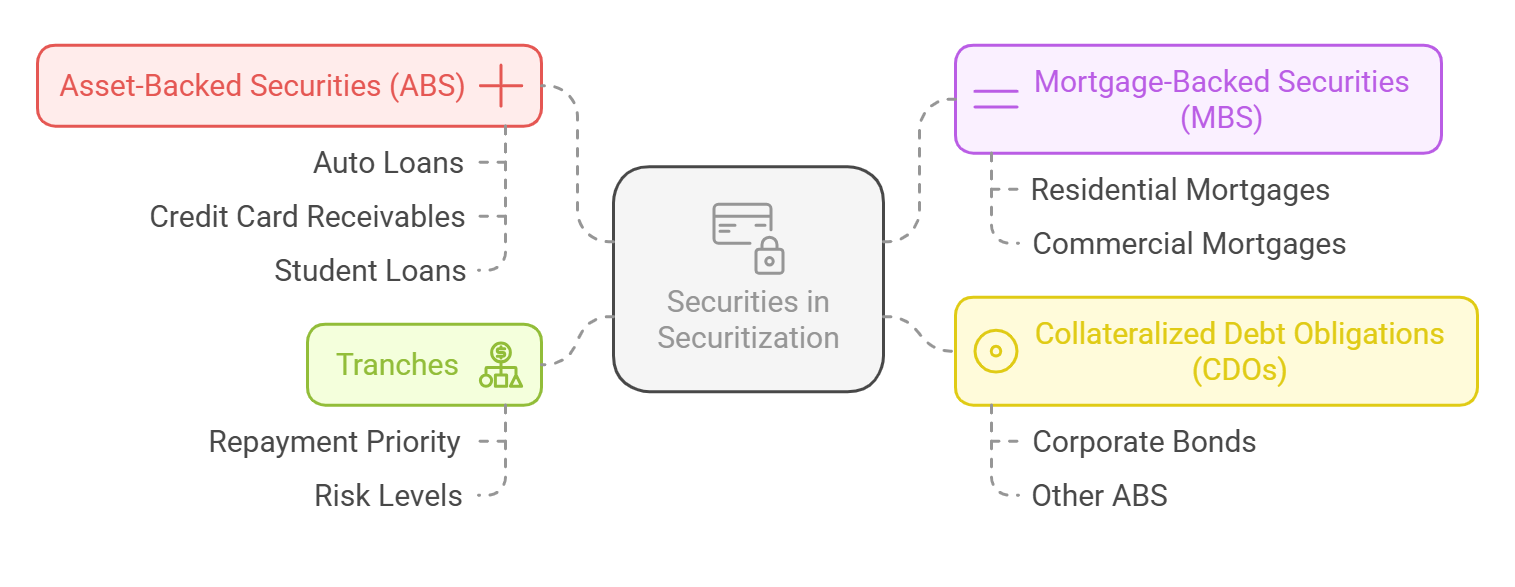

Types of Securities Issued in Securitization

- Asset-Backed Securities (ABS): Securities backed by a pool of assets, such as auto loans, credit card receivables, or student loans.

- Mortgage-Backed Securities (MBS): Securities backed by a pool of mortgages.

- Collateralized Debt Obligations (CDOs): More complex securities backed by a pool of debt instruments, such as corporate bonds or other ABS.

- Tranches: the different classes issued from securities, with different levels of repayment priority and risk.

Securitization in India

- Evolution: Securitization has grown in India in recent years.

- Underlying Assets: Common assets include auto loans, mortgages, and microfinance loans.

- Benefits to originator a) Balance sheet financing, b) credit enhancemtn

-

Key Issues:

- Transfer of assets

- True sale of question

- Constitution of Special Purpose Vehicle

- Equitable Transfers

In conclusion, securitization is a complex but valuable financial tool. It is used by financial institutions around the world to manage risk, improve liquidity, and generate capital.

No Comments