Capital Budgeting Process

The capital budgeting process is a systematic method used by businesses to evaluate and decide on long-term investment projects. It involves assessing potential capital expenditures, forecasting future cash flows, analyzing risks, and selecting the most profitable projects.

Steps in the Capital Budgeting Process

1. Identifying Investment Opportunities

- Businesses must identify potential capital investment projects based on strategic goals.

-

Types of capital investments include:

- Expansion projects (e.g., setting up a new factory).

- Replacement projects (e.g., upgrading old machinery).

- Research & Development (R&D) initiatives.

- Cost-saving projects (e.g., process automation).

🔹 Key Considerations: Market trends, technology advancements, competitive landscape.

2. Screening and Preliminary Analysis

- The identified projects undergo an initial evaluation to determine feasibility.

-

Factors considered:

- Alignment with company objectives.

- Expected profitability.

- Risk assessment (economic, technological, operational risks).

- Example: A retail company analyzing whether opening new stores will increase market share.

3. Estimating Cash Flows

- Businesses must estimate:

- Initial Investment Cost: The upfront capital needed.

- Operating Costs: Maintenance, labor, and other recurring expenses.

- Revenue Generation: Expected cash inflows over the project's life.

- Importance: Inaccurate cash flow projections can lead to incorrect investment decisions.

4. Investment Evaluation Using Capital Budgeting Techniques

Various quantitative techniques are used to analyze investment feasibility:

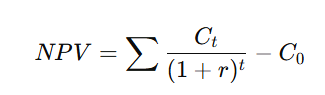

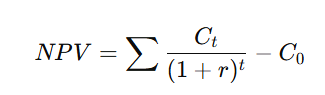

a) Net Present Value (NPV)

- Measures the difference between present cash inflows and outflows, adjusted for the time value of money.

-

Formula:

- If NPV > 0, the project is accepted.

- If NPV < 0, the project is rejected.

b) Internal Rate of Return (IRR)

- The discount rate at which NPV = 0.

- If IRR is higher than the required rate of return, the project is considered viable.

c) Payback Period

- Measures how long it takes for an investment to recover its initial cost.

-

Formula:

- Limitation: It does not account for the time value of money.

d) Profitability Index (PI)

- Measures the ratio of the present value of future cash flows to the initial investment.

-

Formula:

- Decision Rule: If PI > 1, the project is accepted.

5. Risk Analysis and Sensitivity Testing

- Before finalizing a project, companies perform risk analysis by using:

- Sensitivity Analysis – Examining how changes in key variables (e.g., inflation, interest rates) affect profitability.

- Scenario Analysis – Testing different economic conditions.

- Monte Carlo Simulation – A statistical approach for uncertainty modeling.

Example: A company considering international expansion assesses risks related to currency exchange fluctuations and geopolitical instability.

6. Selection and Approval of the Project

- The finance department and top management review investment feasibility reports before making a final decision.

- Approved projects are included in the company's capital expenditure budget.

7. Implementation and Execution

- Once an investment project is approved, companies:

- Allocate funds and resources.

- Acquire assets or equipment.

- Hire employees and train personnel.

- Set up production and distribution.

8. Post-Investment Review and Performance Monitoring

- Businesses conduct regular performance reviews to measure actual outcomes against projected results.

-

Key Performance Indicators (KPIs):

- Return on Investment (ROI).

- Cost savings achieved.

- Impact on revenue growth.

- If a project fails to meet expectations, corrective measures are taken.

Importance of the Capital Budgeting Process

- Ensures Optimal Resource Allocation – Helps businesses allocate capital efficiently.

- Minimizes Investment Risks – Identifies high-risk projects before execution.

- Enhances Business Growth – Supports expansion and market penetration.

- Improves Financial Planning – Helps in managing cash flow and debt.

- Supports Strategic Decision-Making – Aligns investments with long-term business goals.

Conclusion

- The capital budgeting process is an essential tool for making data-driven investment decisions. By following a structured approach—including investment identification, cash flow estimation, risk analysis, and financial modeling—businesses can maximize profitability and ensure long-term success.

- Effective monitoring and post-investment analysis further enhance decision-making and risk management.

No Comments