Capital Structure

Capital structure refers to the mix of debt, equity, and other financial instruments a company uses to finance its operations and growth. The decision regarding capital structure is crucial as it impacts the firm's risk, cost of capital, and overall financial stability.

Concept of Capital Structure

Definition

Capital structure is the proportion of different sources of capital (debt, preference shares, and equity) used by a company to finance its assets.

Components of Capital Structure

- Debt Capital – Borrowed funds such as loans, bonds, and debentures.

- Equity Capital – Ownership funds raised through common and preference shares.

- Hybrid Instruments – A combination of debt and equity, such as convertible debentures.

Importance of Capital Structure

- Affects Cost of Capital – A well-balanced structure minimizes the Weighted Average Cost of Capital (WACC).

- Influences Risk and Return – Higher debt increases financial risk, while equity financing may dilute ownership.

- Impacts Firm Value – A strategically planned capital structure can maximize shareholder wealth.

Factors Affecting Capital Structure

Several internal and external factors influence a company's capital structure decisions.

1. Business Risk

- Companies in volatile industries (e.g., technology) prefer lower debt to avoid financial distress.

- Stable industries (e.g., utilities) can afford higher debt due to predictable earnings.

2. Cost of Debt and Equity

- Debt is cheaper than equity due to tax benefits, but excessive debt increases financial risk.

- Equity financing avoids fixed interest payments but may dilute control.

3. Market Conditions

- During economic booms, firms prefer equity financing due to high stock prices.

- In recessions, companies rely more on debt financing as interest rates may be lower.

4. Taxation Policies

- Interest on debt is tax-deductible, reducing the effective cost of debt.

- Firms in high-tax regimes may prefer debt over equity.

5. Flexibility and Control

- High debt obligations restrict operational flexibility.

- Issuing more equity can lead to dilution of ownership and reduced decision-making power.

6. Industry Norms

- Capital structure choices are often influenced by industry benchmarks and competitors' financial policies.

Capital Structure Theories

Several theories explain how capital structure impacts a firm’s value and cost of capital.

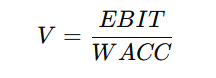

1. Net Income Approach (NI Approach)

Proposed by: David Durand

Key Assumption: Capital structure affects the value of the firm and cost of capital is not constant.

Concept:

- An increase in debt (cheaper than equity) reduces the overall cost of capital (WACC), increasing firm value.

- Firms should maximize leverage (use more debt) to increase value.

Formula:

Criticism:

- Assumes debt has no impact on financial risk, which is unrealistic.

- Ignores the potential for bankruptcy costs.

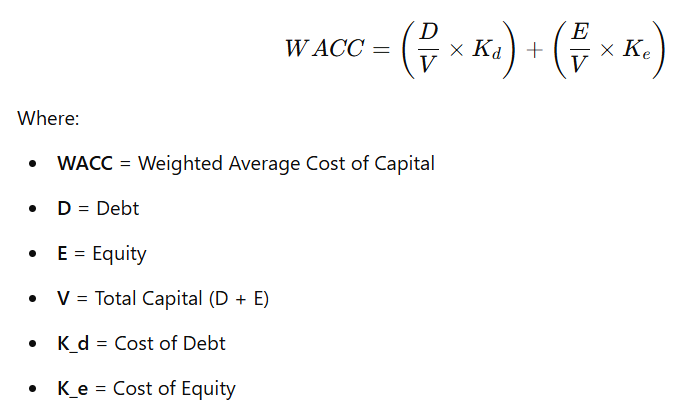

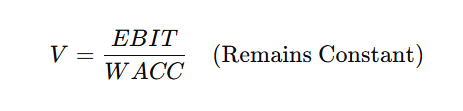

2. Net Operating Income Approach (NOI Approach)

Proposed by: David Durand

Key Assumption: Capital structure is irrelevant and does not affect firm value.

Concept:

- The firm's total value depends on its operating income (EBIT) and business risk, not on debt-equity mix.

- As debt increases, cost of equity increases, offsetting any benefits from lower-cost debt.

- Thus, WACC remains constant, and capital structure decisions do not impact firm value.

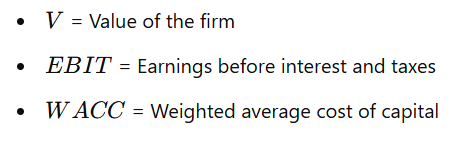

Formula:

Criticism:

- Ignores the tax benefits of debt financing.

- Assumes investors do not perceive financial risk due to high debt levels.

3. Traditional Approach (Intermediate Approach)

Proposed by: Ezra Solomon

Key Assumption: Capital structure influences firm value, but only up to a certain level.

Concept:

- Optimal capital structure exists, balancing the benefits of debt (lower WACC) with the risk of excessive debt (financial distress).

- At moderate levels of debt, the cost of capital decreases and firm value increases.

- Beyond a certain debt threshold, cost of capital increases due to high financial risk.

Graphical Explanation:

-

Stage 1:

- Debt is introduced, reducing WACC.

- Firm value increases as debt is cheaper than equity.

-

Stage 2:

- Excessive debt increases financial risk.

- WACC starts increasing.

-

Stage 3:

- Too much debt causes bankruptcy risk.

- Firm value declines as WACC rises.

Criticism:

- Difficult to determine the exact point where debt becomes excessive.

- Market conditions and investor perception affect capital structure choices.

Conclusion

- Capital structure decisions play a vital role in determining a company's financial performance, risk exposure, and cost of capital

- Theories such as Net Income Approach, Net Operating Income Approach, and the Traditional Approach provide different perspectives on how capital structure impacts firm value.

- While high debt can reduce financing costs, excessive borrowing increases financial distress and bankruptcy risk.

- Therefore, companies must strike a balance between debt and equity to achieve an optimal capital structure that maximizes firm value while minimizing risk.

No Comments