Dividend Decisions

Dividend decisions refer to the policies that companies adopt to distribute profits to shareholders or retain them for reinvestment. These decisions significantly impact a company's stock price, investor satisfaction, and long-term growth.

Concept of Dividend Decisions

A dividend is the portion of a company's earnings that is distributed to shareholders. The decision on how much profit to retain and how much to distribute is influenced by financial stability, future investment needs, and shareholder preferences.

Key Aspects of Dividend Decisions

- Retention vs. Distribution – Companies must decide whether to retain earnings for growth and expansion or distribute them as dividends.

- Effect on Share Price – Dividend payments can signal financial strength, influencing stock prices.

- Tax Considerations – Dividends are taxable income for shareholders, whereas retained earnings contribute to capital gains.

- Market Expectations – Investors expect consistent or growing dividends, impacting stock valuation.

Relevance of Dividend Decisions

The relevance of dividend decisions depends on whether they affect the company’s value and shareholder wealth. Some theories suggest that dividends do impact stock prices, while others argue that dividends are irrelevant if reinvested efficiently.

1. Walter’s Model

Walter’s Model, developed by James E. Walter, suggests that dividend policy influences a firm’s value. The model assumes that:

- All earnings are either reinvested or distributed as dividends.

- The firm’s return on investment (r) and cost of capital (Ke) determine dividend relevance.

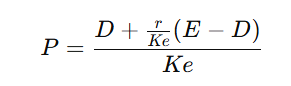

Formula

Where:

- P = Market price per share

- D = Dividend per share

- E = Earnings per share

- r = Return on investment

- Ke = Cost of equity

Decision Rule

- If r > Ke, the firm should retain earnings for reinvestment.

- If r < Ke, the firm should distribute profits as dividends.

- If r = Ke, dividend policy does not affect firm value.

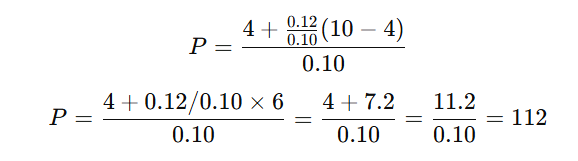

Example

A company has:

Using Walter’s formula:

Since r > Ke, the firm should retain earnings for reinvestment.

Limitations of Walter’s Model

- Assumes constant cost of capital.

- Assumes all profits are either distributed or reinvested.

- Ignores external financing options.

2. Gordon’s Model

Gordon’s Model, developed by Myron Gordon, argues that dividend policy affects stock price because investors prefer stable dividends over uncertain capital gains.

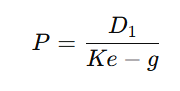

Formula

Where:

Where:

- P = Market price per share

- D1 = Expected dividend per share (D0 × (1+g))

- Ke = Cost of equity

- g = Growth rate of earnings

Decision Rule

- If dividends increase, stock price increases.

- If growth rate (g) is higher, investors may prefer retention over dividends.

- Investors with risk aversion prefer higher dividends.

Example

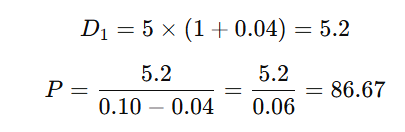

A company has:

- Current dividend (D0) = $5

- Growth rate (g) = 4%

- Cost of equity (Ke) = 10%

Using Gordon’s formula:

Since dividends contribute to stock valuation, dividend policy is relevant.

Limitations of Gordon’s Model

- Assumes constant growth rate (not realistic).

- Ignores market fluctuations.

- Investors may prefer capital gains over dividends for tax reasons.

Comparison of Walter’s and Gordon’s Models

| Aspect | Walter’s Model | Gordon’s Model |

|---|---|---|

| Key Assumption | Firm’s return on investment (r) vs. cost of capital (Ke) | Investors prefer stable dividends |

| Decision Rule | If r > Ke, retain earnings; If r < Ke, pay dividends | If dividends increase, stock price rises |

| Stock Valuation | Based on profit retention and reinvestment | Based on expected dividends and growth |

| Limitations | Assumes no external financing | Assumes constant dividend growth |

Conclusion

Dividend decisions are crucial for balancing shareholder satisfaction and business expansion.

- Walter’s Model supports reinvestment if returns exceed cost of capital.

- Gordon’s Model emphasizes stable dividends for stock value appreciation.

Companies must adopt flexible dividend policies based on profitability, market conditions, and investor expectations.

No Comments