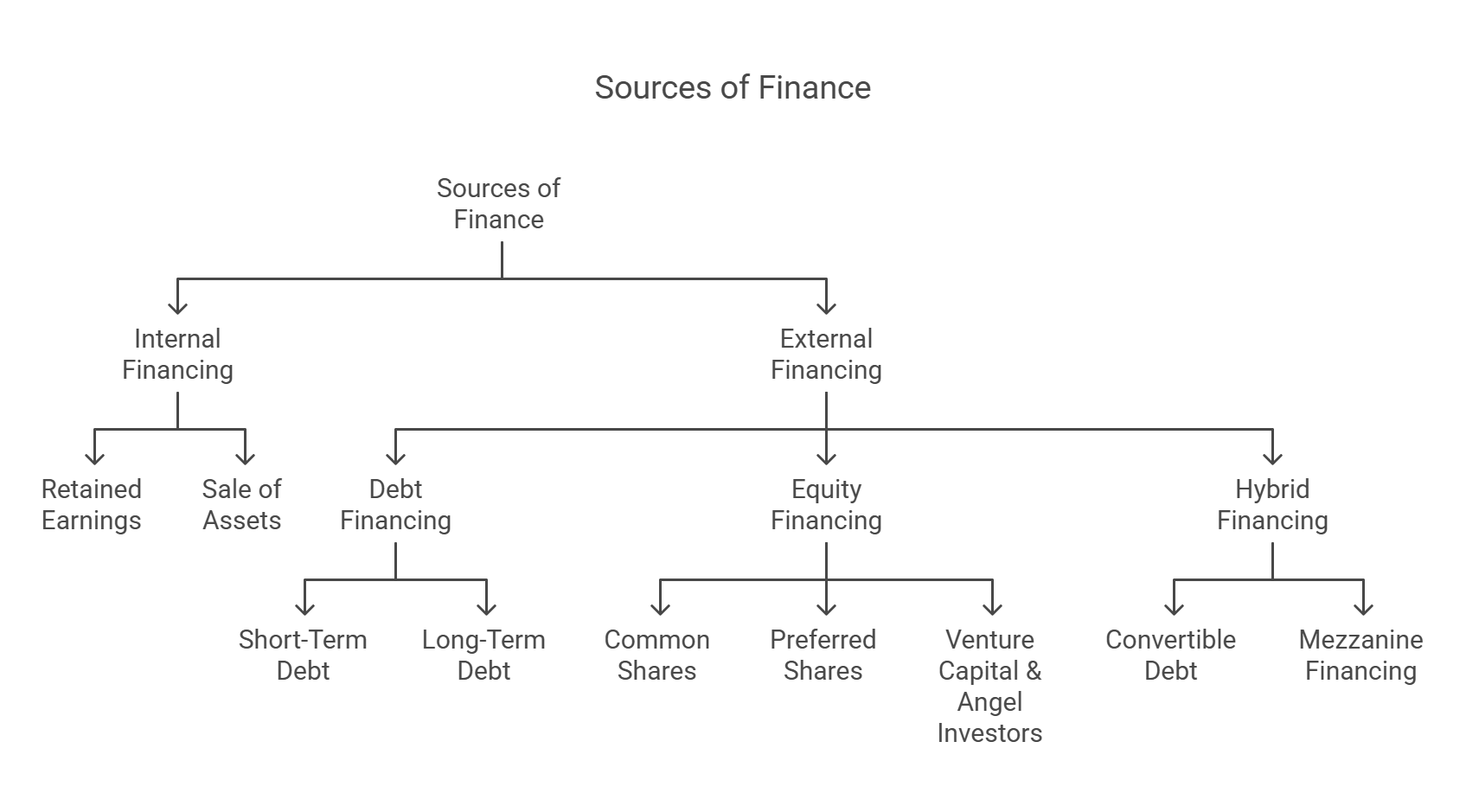

Sources of Finance

Businesses need finance for various purposes, such as starting operations, expansion, acquiring assets, and managing daily operations. The sources of finance are broadly classified into internal sources (funds generated within the company) and external sources (funds obtained from outside the company). Each source has distinct characteristics, advantages, and risks.

1. Internal Sources of Finance

Internal financing refers to funds generated from within the business, helping companies maintain financial independence without incurring debt or diluting ownership.

a) Retained Earnings

- Definition: Profits that are reinvested in the business rather than distributed as dividends.

- Purpose: Used for expansion, purchasing assets, research & development, or acquiring other companies.

- Advantages: No debt incurred, no interest payments, and no dilution of ownership.

- Limitations: Availability depends on profitability; some companies may have negative retained earnings (deficit) if they have sustained losses.

b) Sale of Assets

- Definition: Selling company-owned assets, such as machinery, buildings, or land, to generate cash.

- Purpose: Helps raise funds without borrowing; commonly used in restructuring situations.

- Advantages: No repayment obligation; avoids interest costs.

- Limitations: Selling key assets may impact future operations; the value of assets may depreciate over time.

2. External Sources of Finance

External financing is obtained from outside the company, including debt, equity, and hybrid financing.

A. Debt Financing

Debt financing involves borrowing money that must be repaid over time, usually with interest. It includes short-term and long-term financing options.

i) Short-Term Debt

Used to cover temporary financial needs or working capital shortages.

-

Bank Overdraft: A facility that allows businesses to withdraw more than the available balance in their bank account.

- Pros: Flexible, helps manage cash flow gaps.

- Cons: High-interest rates, repayable on demand.

-

Trade Credit: Suppliers allow businesses to purchase goods/services on credit, with payment due later.

- Pros: No immediate cash outflow, enhances cash management.

- Cons: Late payments may attract penalties or loss of supplier trust.

-

Short-Term Bank Loans: Loans with a maturity period of less than a year.

- Pros: Quick access to funds.

- Cons: Higher interest rates compared to long-term loans.

ii) Long-Term Debt

Used for capital-intensive investments such as asset acquisition, business expansion, or mergers.

-

Term Loans: Loans obtained from banks or financial institutions with fixed repayment schedules.

- Pros: Predictable payments, suitable for asset financing.

- Cons: Requires collateral; failure to repay may result in asset seizure.

-

Debentures/Bonds: Debt instruments issued by companies to raise funds from investors.

- Pros: Fixed interest payments; longer repayment periods.

- Cons: Increases debt burden; investors must be repaid regardless of company performance.

-

Lease Financing: Instead of buying an asset, a company leases it and makes periodic payments.

- Pros: No large upfront investment; tax benefits.

- Cons: Ownership remains with the lessor; long-term costs may be higher than purchasing.

B. Equity Financing

Equity financing involves raising capital by selling shares in the company. Unlike debt financing, there is no obligation to repay investors, but it dilutes ownership control.

i) Common Shares (Ordinary Shares)

ii) Preferred Shares

iii) Venture Capital & Angel Investors

- Definition: Investors who provide funds to startups and high-growth companies in exchange for equity.

- Advantages: Access to large capital, strategic guidance from investors.

- Disadvantages: High expectations for growth; loss of business control.

C. Hybrid Financing

Hybrid financing combines elements of debt and equity, providing flexibility to businesses.

i) Convertible Debt

- Definition: A loan that can be converted into equity at a later stage.

- Advantages: Lower interest rates compared to regular debt; can attract investors.

- Disadvantages: Can dilute ownership when converted.

ii) Mezzanine Financing

- Definition: A mix of debt and equity financing where lenders receive equity in case of loan default.

- Advantages: Flexible repayment terms.

- Disadvantages: Higher interest rates; risk of ownership loss if not repaid.

Conclusion

Businesses utilize a mix of internal and external financing based on their needs, risk appetite, and growth plans. Debt financing offers quick access to capital but increases liabilities, whereas equity financing avoids repayment obligations but dilutes ownership. Understanding various financing options helps businesses optimize capital structure and financial sustainability.

No Comments