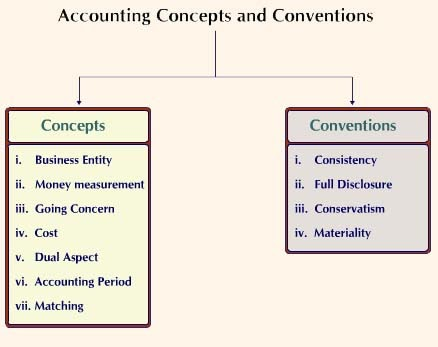

Basic Concepts and Conventions

Accounting principles are like the rules of the road for financial reporting. They ensure everyone understands the financial story being told. They're broadly categorized into Concepts and Conventions.

What are Concepts?

Concepts are fundamental ideas or assumptions that guide accounting practices. They are the why behind the how of accounting. Think of them as the basic building blocks.

What are Conventions?

Conventions are generally accepted practices or customs that have evolved over time. They are the how of applying the why (concepts). They provide guidance on how to deal with specific situations where concepts might be open to interpretation.

Why are they needed?

- Comparability: Concepts and conventions create a standardized framework, allowing users to compare financial information across different companies and time periods.

- Reliability: They enhance the credibility and trustworthiness of financial information.

- Understandability: They make financial statements easier to understand for users.

- Decision-Making: They provide a solid foundation for informed business decisions.

In essence, concepts provide the theoretical foundation, while conventions provide the practical guidelines for applying those concepts. Together, they create a robust system for financial reporting.

So lets start with the concepts -

1. The Business Entity Concept

Imagine your business as a separate person, even if you're the only owner. That's the core idea behind the Business Entity Concept. It means your business is a distinct entity, completely separate from you, the owner. Think of it like this:

- You: You have your own money, your own expenses, and your own taxes.

- Your Business: Your business has its own money, its own expenses, and its own taxes.

These two "people" are distinct. The business's finances shouldn't be mixed with your personal finances.

Why is this important?

This separation is crucial for several reasons:

- Accurate Financial Reporting: It gives a clear picture of how your business is actually performing. Mixing personal and business finances makes it impossible to tell if the business is profitable.

- Tax Purposes: Separate records make filing taxes much easier and more accurate. You can clearly distinguish between business income and personal income.

- Legal Reasons: In some business structures (like corporations), the business is legally separate from the owner. The Business Entity Concept reinforces this legal separation.

- Easy Evaluation: If you ever want to sell your business or get a loan, separate financial records make it much easier for others to assess the business's value.

Examples to Make it Clear -

-

Owner Takes Money Out: Let's say you own a bakery. If you take $1,000 from the bakery's cash register to pay for your personal groceries, that's not a business expense. It's considered a "draw" or "owner's withdrawal" and reduces your ownership stake in the business. It's also taxable income for you personally.

-

Owner Loans Money to the Business: If you lend your business $10,000, the business records this as a liability (a debt it owes you). You, personally, record it as an asset (a loan receivable). Again, the transaction is recorded separately for both entities.

2. The Dual Aspect Concept

Imagine every financial transaction as a coin. The Dual Aspect Concept, also known as the duality principle, says that every coin has two sides. In accounting, these sides are called debit and credit. Every transaction affects at least two accounts, one with a debit and the other with a credit.

What does this mean?

This concept is the foundation of double-entry bookkeeping, a system that ensures balance in your financial records. Think of it like a seesaw. For the seesaw to stay balanced, any change on one side must be matched by an equal change on the other.

- Debit: Often associated with increases in assets (what your business owns, like cash, equipment) and expenses (what your business spends, like rent, salaries). It can also represent decreases in liabilities (what your business owes, like loans) income/revenue and equity.

- Credit: Often associated with increases in liabilities, income/revenue and equity (the owner's stake in the business). It can also represent decreases in assets and expenses.

How it Works: The Double-Entry System

The double-entry system records every transaction twice: once as a debit and once as a credit. This ensures that the accounting equation (Assets = Liabilities + Equity) always stays balanced.

Let's look at a simple example:

Scenario: You buy a new computer for your business for $1,000 in cash.

- Debit: You increase your asset "Equipment" by $1,000.

- Credit: You decrease your asset "Cash" by $1,000.

Notice how both sides of the transaction are equal ($1,000) and how one is a debit and the other is a credit. This keeps your accounting equation balanced.

from incidental transactions (e.g., selling an asset for less than its value).

Why is this important?

The Dual Aspect Concept and double-entry bookkeeping are crucial for:

- Accuracy: It helps catch errors because every transaction is recorded twice.

- Reliability: It provides a more complete and reliable picture of your business's finances.

- Better Decision-Making: Accurate financial information leads to better business decisions.

3.The Going Concern Concept

The Going Concern Concept is a fundamental assumption in accounting. It basically means that when preparing financial statements, accountants assume your business will continue operating in the foreseeable future and won't be forced to close down or sell off all its assets anytime soon.

What does this mean in practice?

Imagine you're looking at a company's financial report. The Going Concern Concept implies that the numbers you see are based on the idea that the business will continue to operate and generate revenue. It's not a snapshot of a business about to close its doors.

- Foreseeable Future: While not strictly defined, "foreseeable future" is generally considered to be at least the next 12 months from the end of the reporting period.

Why is this important?

The Going Concern Concept is crucial because it:

- Impacts how assets are valued: If a business is expected to continue operating, its assets can be valued based on their future use. If it's about to close, assets might need to be valued at their fire-sale price (what they'd fetch quickly in a liquidation).

- Affects expense recognition: Some expenses can be spread out over time (depreciation, for example) because the business is expected to use the related asset for a while. This wouldn't make sense if the business was about to shut down.

- Provides context for financial statements: Investors and other stakeholders rely on the Going Concern Concept to make informed decisions. They assume the business will continue, and therefore, the financial information is relevant to their future interactions with the company.

Example :

A company, "ABC Ltd.," makes a specialized chemical. Suddenly, the government bans the manufacture and sale of this chemical. If this is ABC Ltd.'s only product, the Going Concern assumption is questionable. They might not be able to continue operating in the same way.

4.The Accounting Period Concept

The Accounting Period Concept is all about dividing a business's life into specific time periods for reporting and analysis. Think of it like slicing a cake into pieces. Each slice represents a specific period (a week, a month, a quarter, or a year) for which the business prepares financial reports.

What does this mean?

Businesses don't exist indefinitely. While the Going Concern Concept assumes they'll continue for the foreseeable future, it's still useful to look at their performance over shorter, defined periods. This is where the Accounting Period Concept comes in. It allows businesses to:

- Track Performance Regularly: By dividing time into periods, businesses can see how they're doing over specific intervals. Are sales up this quarter compared to last quarter? Are expenses under control this month?

- Make Comparisons: Financial reports prepared for different periods can be compared to identify trends and patterns. Is the business more profitable now than it was a year ago? This helps in understanding progress and identifying potential problems.

- Plan for the Future: Past performance is a key indicator for future success. By analyzing financial data from previous periods, businesses can make forecasts and develop budgets for upcoming periods.

- Provide Information to Stakeholders: Investors, lenders, and other stakeholders need regular updates on a business's financial health. The Accounting Period Concept makes it possible to provide these updates in a timely and organized manner.

How it Works

A business chooses its accounting period. Common periods include:

- Monthly: Provides very detailed and frequent updates.

- Quarterly: A good balance between detail and frequency.

- Annually (Fiscal Year): Required for tax purposes and provides a comprehensive overview of the year's performance.

Regardless of the period chosen, the business records all its financial transactions within that specific timeframe. At the end of the period, financial statements (like income statements and balance sheets) are prepared to summarize the business's performance and financial position for that period.

Example

Imagine a clothing store. They might choose a monthly accounting period. At the end of each month, they'll prepare financial statements that show:

- How much revenue they earned from selling clothes during that month.

- How much they spent on expenses (rent, salaries, inventory) during that month.

- Their profit or loss for that month.

They can then compare these monthly reports to see if their sales are increasing, if their expenses are under control, and how their overall profitability is trending.

5.The Money Measurement Concept

The Money Measurement Concept in accounting states that only transactions that can be expressed in monetary terms (i.e., money) should be recorded in the accounting books. Essentially, if you can't put a price tag on it, it doesn't get formally recorded in the financial statements.

What does this mean?

This concept focuses on quantifiable, objective data. It deals with things you can count and measure in currency. Think of it this way: if a transaction doesn't involve an exchange of money or have a clear monetary value, it's generally not recorded in the traditional accounting system.

- Quantitative Transactions: These are recorded. Examples include sales, purchases, salaries paid, loans, and cash received. These have a direct financial impact and can be easily measured in monetary units.

- Qualitative Transactions: These are not recorded. Examples include employee morale, the quality of customer service, the reputation of the company, or the skill level of the workforce. While these factors are important for a business's success, they are difficult to quantify in monetary terms.

Why is this important?

The Money Measurement Concept provides a consistent and objective way to track and report a business's financial activities. It allows for:

- Standardized Reporting: By focusing on monetary transactions, financial statements can be easily compared across different companies and time periods. Everyone understands the value of a dollar.

- Objective Analysis: Financial data becomes more objective and less subjective, allowing for more meaningful analysis and decision-making.

- Clear Financial Picture: The financial statements provide a focused view of the business's financial performance and position, even if they don't capture every aspect of the business.

Example

Let's say a company hires a highly skilled and experienced manager. This is a very positive event for the business! However, the hiring itself is not a monetary transaction (until the first salary payment). Therefore, the hiring of the manager, no matter how skilled they are, is not immediately recorded in the accounting books. Only when the business pays the manager's salary will a monetary transaction occur and be recorded.

6.Accrual Accounting

Accrual accounting is a method of accounting that records revenues when they are earned and expenses when they are incurred, regardless of when cash changes hands. It's about matching the timing of revenues and expenses to the actual economic activity, not just the cash flow.

What does this mean?

Think of it this way:

- Revenue: In accrual accounting, you record revenue when you've earned it, not necessarily when you get paid. This usually means when you've provided the goods or services to the customer.

- Expenses: You record expenses when you've incurred them, not necessarily when you pay for them. This usually means when you've used the goods or services in your business operations.

How it works

Accrual accounting uses the matching principle. This principle states that revenues and the expenses related to generating those revenues should be recognized in the same accounting period. This gives a more accurate picture of profitability.

Example

Let's say you own a consulting business.

-

Scenario 1: You provide consulting services to a client in December, but you don't get paid until January.

- Accrual Accounting: You would record the revenue in December (when you earned it), even though you didn't receive the cash until January. You would also record any related expenses (like consultant salaries) incurred in December.

- Cash Accounting: You would record the revenue in January (when you received the cash).

-

Scenario 2: You receive a utility bill in December for services used in November, but you don't pay it until January.

- Accrual Accounting: You would record the expense in November (when you incurred it), even though you didn't pay the bill until January.

- Cash Accounting: You would record the expense in January (when you paid the bill).

Accrual vs. Cash Accounting

The main difference between accrual and cash accounting is the timing of when revenues and expenses are recognized.

- Accrual Accounting: Focuses on when revenues are earned and expenses are incurred.

- Cash Accounting: Focuses on when cash is received or paid.

Why use accrual accounting?

Accrual accounting provides a more accurate picture of a business's financial performance over a period of time. It's generally considered the more sophisticated and reliable method, and it's often required for larger businesses.

7.The Full Disclosure Principle

The Full Disclosure Principle in accounting requires companies to include all relevant information in their financial statements so that anyone reading those statements can make informed decisions about the company. It's about transparency and providing a complete picture of the business's financial health.

What does this mean?

Imagine you're considering investing in a company. You wouldn't want to make that decision based on incomplete or misleading information, right? The Full Disclosure Principle ensures that companies provide all the necessary details, both positive and negative, so you can understand the true financial state of the business.

What kind of information needs to be disclosed?

Pretty much anything that could impact a user's understanding of the financial statements. This includes:

- Financial Performance: Revenue, expenses, profits, losses – the core financial data.

- Financial Position: Assets, liabilities, equity – what the company owns and owes.

- Significant Events: Lawsuits, mergers, acquisitions, major changes in operations – anything that could significantly affect the company's future.

- Accounting Policies: The specific methods the company uses to account for certain transactions – this helps users compare financial statements across different companies.

- Contingencies: Potential future events that could impact the company's finances (e.g., pending lawsuits).

Why is this important?

The Full Disclosure Principle is essential for:

- Informed Decision-Making: Investors, lenders, and other stakeholders rely on financial statements to make decisions about whether to invest in, lend to, or do business with a company. Full disclosure ensures they have the information they need to make sound judgments.

- Transparency and Trust: By being transparent about their finances, companies build trust with their stakeholders.

- Accountability: Full disclosure holds companies accountable for their financial performance.

Example

Let's say a company is facing a major lawsuit that, if lost, could significantly impact its financial stability. The Full Disclosure Principle requires the company to disclose this lawsuit in the notes to its financial statements, even if the outcome is uncertain. This allows investors to assess the potential risk associated with the lawsuit.

8.The Materiality Concept

The Materiality Concept in accounting is all about focusing on what's important. It states that only information that is significant enough to influence the decisions of users of financial statements needs to be included in those statements. In other words, don't get bogged down in the small stuff; focus on the things that actually matter.

What does this mean?

Imagine a large company like Amazon. A few dollars' worth of office supplies probably won't make a big difference to their overall financial picture. However, a multi-million dollar contract or a significant lawsuit would be material. The Materiality Concept guides accountants to focus on disclosing the latter and not necessarily the former.

How do you determine what's material?

There's no hard and fast rule. It depends on the size and nature of the business, as well as the specific situation. Accountants use their professional judgment to assess whether an item is material. Factors they consider include:

- The size of the transaction: A $10 error might be immaterial for a large corporation but very material for a small business.

- The nature of the item: Some items might be qualitatively material, even if they are small in amount. For example, a small illegal payment is likely to be considered material because of its nature.

- The impact on decision-making: If the information would change a user's decision about the company (e.g., whether to invest), it's likely to be material.

Example

Let's say a small bakery buys a new $50 spatula. This is probably an immaterial expense. They might simply include it in a general category of "kitchen supplies" rather than listing it separately. However, if they buy a new $5,000 oven, that would be a material purchase and would likely be listed separately in the financial statements.

Why is this important?

The Materiality Concept helps to:

- Keep financial statements clear and concise: By focusing on material information, the statements are easier to understand and use.

- Reduce clutter: Including every tiny detail would make financial statements overwhelming and difficult to navigate.

9.The Consistency Concept

The Consistency Concept in accounting emphasizes the importance of using the same accounting methods and policies over time. It's like having a set of rules for how you keep score in a game. If you change the rules every time you play, it becomes difficult to track progress and compare scores.

What does this mean?

This concept means that once a company chooses a particular accounting method (for example, how to depreciate assets or how to recognize revenue), they should stick with it from one accounting period to the next. This allows for meaningful comparisons of financial performance over time.

Why is this important?

Consistency is crucial for:

- Comparability: If a company changes its accounting methods frequently, it becomes difficult to compare its financial performance from one year to the next. Consistency allows stakeholders to see trends and assess how the business is doing over time.

- Reliability: Consistent application of accounting methods enhances the reliability and credibility of financial statements. Users can trust that the numbers are calculated using the same "rules" each time.

- Reduced Bias: Changing accounting methods can sometimes be used to manipulate financial results. Consistency helps to prevent this by requiring companies to stick to their chosen methods.

When can accounting methods be changed?

While consistency is important, there are situations where a change in accounting methods might be necessary. This could be due to:

- Changes in accounting standards: New accounting rules might require companies to adopt a different method.

- Changes in the business: A significant change in the nature of the business might necessitate a change in accounting methods.

However, even when a change is made, it should be clearly disclosed in the financial statements, along with an explanation of the reason for the change and its impact on the financial results. This maintains transparency.

Example

Let's say a company decides to use the straight-line method of depreciation for its equipment. The Consistency Concept suggests they should continue using the straight-line method for similar equipment in future periods. If they suddenly switched to a different depreciation method, it would make it difficult to compare their profits from one year to the next.

10.The Conservatism Concept

The Conservatism Concept in accounting is all about being cautious and erring on the side of understatement. It's like saying, "Hope for the best, but prepare for the worst." When faced with uncertainty, accountants should choose the option that is less likely to overstate assets or income, and more likely to overstate liabilities or expenses.

What does this mean?

Conservatism encourages accountants to:

- Recognize losses sooner: If there's a chance of a loss, it's better to recognize it now rather than later.

- Delay recognizing gains: If there's a chance of a gain, it's better to wait until it's certain before recognizing it.

- Value assets conservatively: When in doubt, it's better to value assets at a lower, more conservative estimate.

- Estimate liabilities cautiously: When estimating liabilities, it's better to err on the side of a higher estimate.

Why is this important?

Conservatism helps to:

- Provide a more realistic picture: By being cautious, financial statements are less likely to paint an overly optimistic picture of a company's financial health.

- Protect stakeholders: Conservatism helps to protect investors and creditors by ensuring that financial statements are not misleadingly optimistic.

- Promote prudent decision-making: By recognizing potential problems early, conservatism encourages businesses to take steps to mitigate those risks.

Example

Let's say a company is involved in a lawsuit. Even if the company believes they will win the lawsuit, the Conservatism Concept suggests they should still estimate and record a potential liability in case they lose. This is because it's better to be prepared for a potential loss than to be caught off guard.

2 Comments

add page introduction. concepts are good but you need to add intro like what are an concept and an convention and why its import and and then proceed with expalinaiton of these concepts. please make the revisions. concepts are beautifully explained good job

use infographics from napkin.ai