Salient features of Ind-AS

Indian Accounting Standards (Ind AS) - Key Features

The Institute of Chartered Accountants of India (ICAI) introduced Indian Accounting Standards (Ind AS) to bring Indian accounting practices closer to international standards. Ind AS is based on the International Financial Reporting Standards (IFRS) and is mandatory for certain companies in India. Let's break down the key features:

Applicability

-

Who uses Ind AS? Ind AS applies to specific types of companies, including:

- Listed companies (those whose shares are traded on the stock market)

- Unlisted companies with a net worth of INR 250 crore or more

- Holding companies, subsidiaries, and associate companies of listed companies.

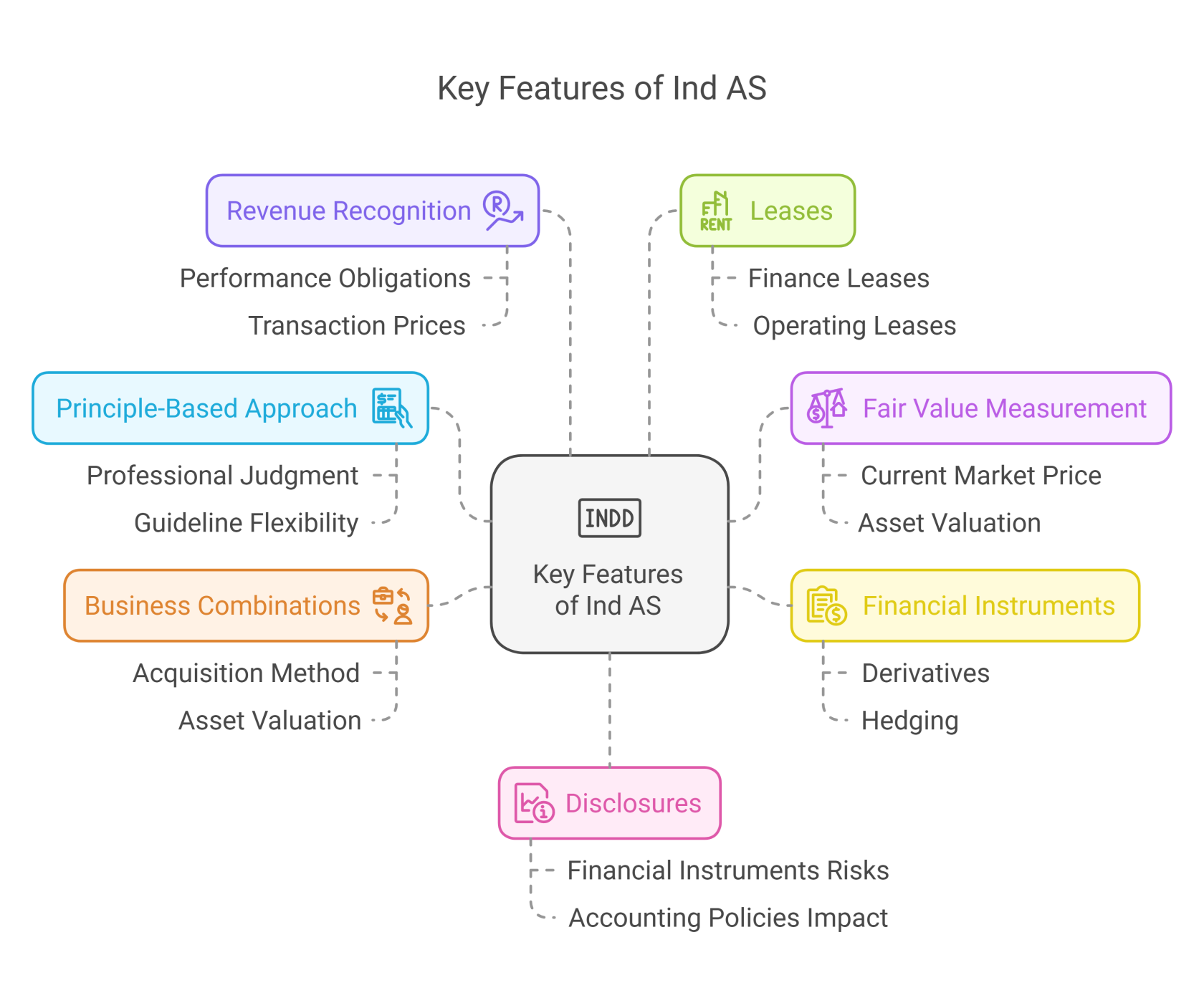

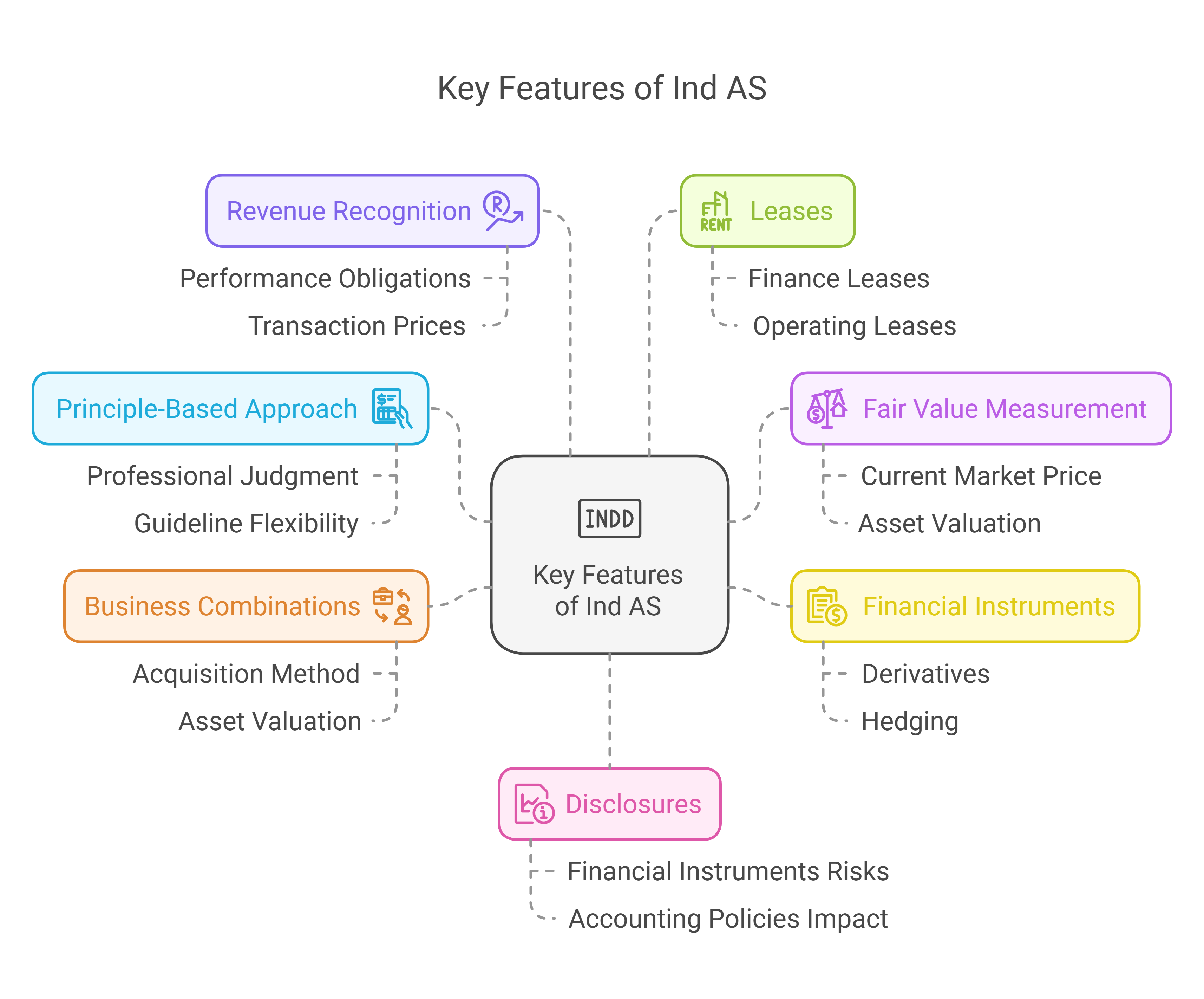

Key Features of Ind AS

-

Principle-Based Approach:

- What it is: Instead of strict rules, Ind AS focuses on general principles.

- How it works: Companies use their professional judgment to decide the best way to account for a transaction, based on these principles.

- Analogy: Think of it like having guidelines instead of step-by-step instructions, allowing for flexibility in complex situations.

-

Fair Value Measurement:

- What it is: Some assets and liabilities are measured at their "fair value" - what they're worth in the market right now.

- How it works: This is like valuing your house based on the current market price instead of what you originally paid for it.

-

Financial Instruments:

- What it is: Ind AS has detailed rules for accounting for financial instruments, including complex items like derivatives and hedging.

- How it works: It provides a framework for recognizing, measuring, and disclosing these instruments, making it clearer how these complex financial elements affect companies' financials.

-

Business Combinations:

- What it is: Ind AS provides guidance on accounting when one company buys another (mergers and acquisitions).

- How it works: It uses the "acquisition method," where the buying company records the purchased company's assets and liabilities at their fair value.

-

Revenue Recognition:

- What it is: Ind AS has detailed rules on when and how to recognize revenue.

- How it works: It focuses on performance obligations, allocating transaction prices, and handling situations where the amount to be received varies.

-

Leases:

- What it is: Ind AS has rules for how to account for leases, which are agreements to rent something for a certain period.

- How it works: It distinguishes between finance leases and operating leases, requiring the recognition of lease liabilities and right-of-use assets, providing a more realistic reflection of the lease contracts.

-

Disclosures:

- What it is: Companies must provide detailed disclosures in their financial reports.

-

How it works: These disclosures include information on risks related to financial instruments, how accounting policies affect the reports, and key assumptions made in measuring fair value. These help users understand the underlying story behind the financials.

Conclusion:

In short, Ind AS aims to improve the quality and reliability of financial reporting in India. It provides detailed guidance on accounting for various transactions using a principle-based approach and fair value measurement. It also includes guidance on financial instruments, business combinations, revenue recognition, leases, and detailed disclosures. By following these standards, companies in India are bringing their accounting practices in line with international standards, improving transparency and making their financial reports more comparable globally.

No Comments