Preparation of Trial Balance

Trial Balance: Checking Your Accounting Accuracy

The Trial Balance is a crucial step in the accounting process. It's like a checkpoint that helps ensure your financial records are accurate and balanced. It lists all the account balances from your ledger and checks to make sure the total debits equal the total credits.

What is the Trial Balance?

Think of the Trial Balance as a summary of all your ledger accounts. It's a statement with two columns: debit and credit. All the accounts with debit balances are listed in the debit column, and all the accounts with credit balances are listed in the credit column.

Why is it important?

The main purpose of the Trial Balance is to:

- Verify accuracy: It checks if the total debits equal the total credits. If they do, it suggests that your journal entries and ledger postings have been done correctly. If they don't, it means there's an error somewhere that needs to be found and corrected.

- Identify errors: If the Trial Balance doesn't balance, it helps you pinpoint where the error might be. It could be a simple transposition error (e.g., writing $540 instead of $450), an incorrect posting, or a more complex issue.

- Prepare financial statements: The Trial Balance is the foundation for preparing the financial statements (balance sheet, income statement, etc.).

When is it prepared?

The Trial Balance can be prepared at any time, but it's most commonly prepared at the end of the accounting period (month, quarter, or year).

Methods for Preparing a Trial Balance

There are three main methods for preparing a Trial Balance:

-

Balance Method:

- This is the most common method.

- Only the balances of the ledger accounts are transferred to the Trial Balance.

- Debit balances go in the debit column, and credit balances go in the credit column.

-

Total Amount Method:

- This method uses the total debits and credits from each ledger account, not just the balances.

- It can be prepared immediately after posting to the ledger, even before any adjustments are made.

-

Total-cum-Balances Method:

- This method combines the Balance Method and the Total Amount Method.

- It has four columns: debit balances, credit balances, total debits, and total credits.

- This method is rarely used in practice.

FORMAT :

Name of Business Trial Balance as on date _______

| Particulars | L.F. | Dr. Balance(₹) | Cr. Balance (₹) |

|---|---|---|---|

| Cash A/c | XXXX | ||

| Capital A/c | XXXX | ||

| Drawings A/c | XXXX | ||

| Purchases A/c | XXXX | ||

| Sales A/c | XXXX | ||

| Machinery A/c | XXXX | ||

| Rent A/c | XXXX | ||

| Salaries A/c | XXXX | ||

| Purchase Return and so on | XXXX | ||

| Total | XXXX | XXXX |

Example

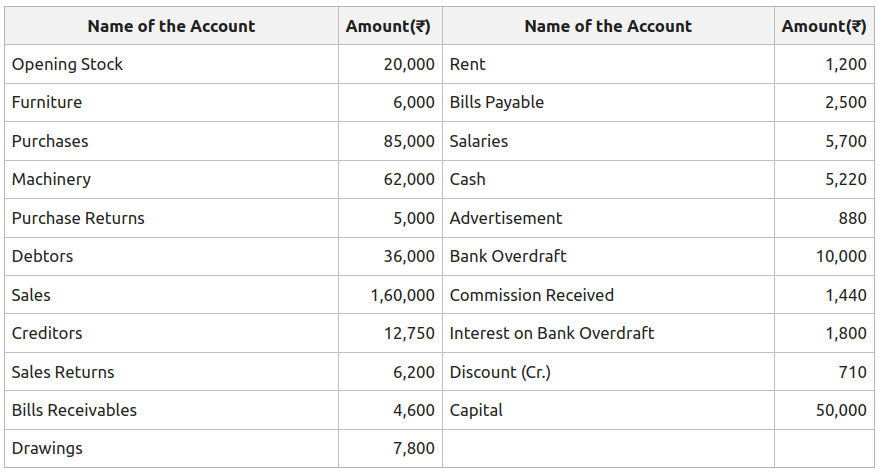

Following are the ledger balances of Ram Das Pvt. Ltd. as on the date 31 March, 2022. Prepare the Trial Balance using the following balances.

SOLUTION :

Ram Das Pvt. Ltd. Trial Balance as on 31st March 2022

| Particulars | L.F. | Dr. Balance(₹) | Cr. Balance (₹) |

|---|---|---|---|

| Opening Stock | 20,000 | ||

| Furniture | 6,000 | ||

| Purchases | 85,000 | ||

| Machinery | 62,000 | ||

| Purchase Returns | 5,000 | ||

| Debtors | 36,000 | ||

| Sales | 1,60,000 | ||

| Creditors | 12,750 | ||

| Sales returns | 6,200 | ||

| Bills Receivables | 4,600 | ||

| Drawings | 7,800 | ||

| Rent | 1,200 | ||

| Bills Payable | 2,500 | ||

| Salaries | 5,700 | ||

| Cash | 5,220 | ||

| Advertisement | 880 | ||

| Bank Overdraft | 10,000 | ||

| Commission Received | 1,440 | ||

| Interest on Overdraft | 1,800 | ||

| Discount (Cr.) | 710 | ||

| Capital | 50,000 | ||

| Total | 2,42,400 | 2,42,400 |

No Comments