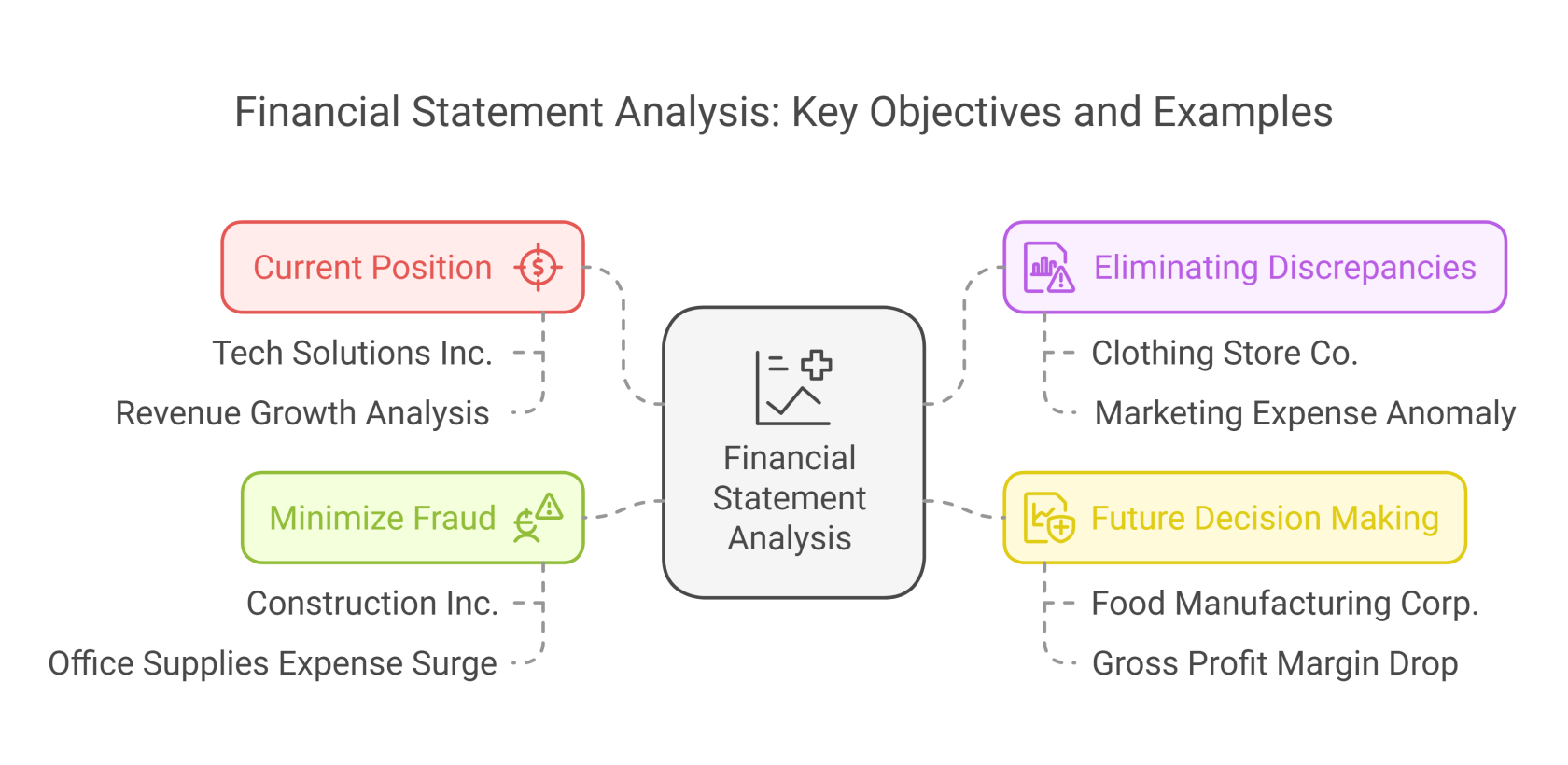

Objectives of Financial Statement Analysis And Its source of Information

Financial statement analysis is like a company's health check-up. It uses financial data to see how well a business is doing. Let's look at the key reasons and see them with clear examples.

1. Knowing Where the Company Stands (Current Position)

- The Goal: To assess if the company is meeting its financial targets and if it's heading in the right direction.

- Simple Explanation: Like checking a GPS to see if you're on the right route.

-

Example:

- Scenario: "Tech Solutions Inc." aimed to increase revenue by 15% this year.

- Analysis: By comparing this year's revenue to last year's, analysts can see if they're on track.

- Outcome: If revenue only increased by 5%, Tech Solutions knows it's falling short and needs to figure out why and adjust its strategy. If it increased by 20% they can pat themselves on the back and plan for further growth.

2. Spotting and Fixing Problems (Eliminating Discrepancies)

- The Goal: To identify any unusual or problematic trends in a company's finances to quickly fix them.

- Simple Explanation: Like checking a car for unusual noises – something might need fixing.

-

Example:

- Scenario: "Clothing Store Co." typically spends about 8% of revenue on marketing.

- Analysis: This quarter, the marketing expenses are suddenly 15% of revenue.

- Outcome: The company investigates, finding a one-off advertising campaign, and is able to budget for it accordingly in future. They can also see that this will impact profits and can adjust accordingly. If it isn't one-off and the reason is unknown, it can be addressed quickly so it doesn't become a long-term issue.

3. Making Smart Decisions for the Future (Future Decision Making)

- The Goal: To make informed plans and adjustments based on the company's financial health.

- Simple Explanation: Like looking at the weather forecast to decide what activities to plan.

-

Example:

- Scenario: "Food Manufacturing Corp." has a historical gross profit margin of 30%.

- Analysis: In the last quarter, the gross profit margin dropped to 25%.

- Outcome: They investigate, find that raw material prices have increased, and decide to either raise prices, find new suppliers, or cut costs in another area to keep profits up.

4. Reducing Fraud and Theft (Minimize Chances of Fraud)

- The Goal: To ensure financial accuracy and deter employees from fraudulent activities.

- Simple Explanation: Like security cameras in a store that deters theft.

-

Example:

- Scenario: "Construction Inc." has a typical expense of $5000 per month for office supplies.

- Analysis: This month, the office supplies expense jumped to $20,000.

- Outcome: The company audits the purchases and finds that a manager was using the company to purchase personal goods. The firm can now address this fraudulent activity.

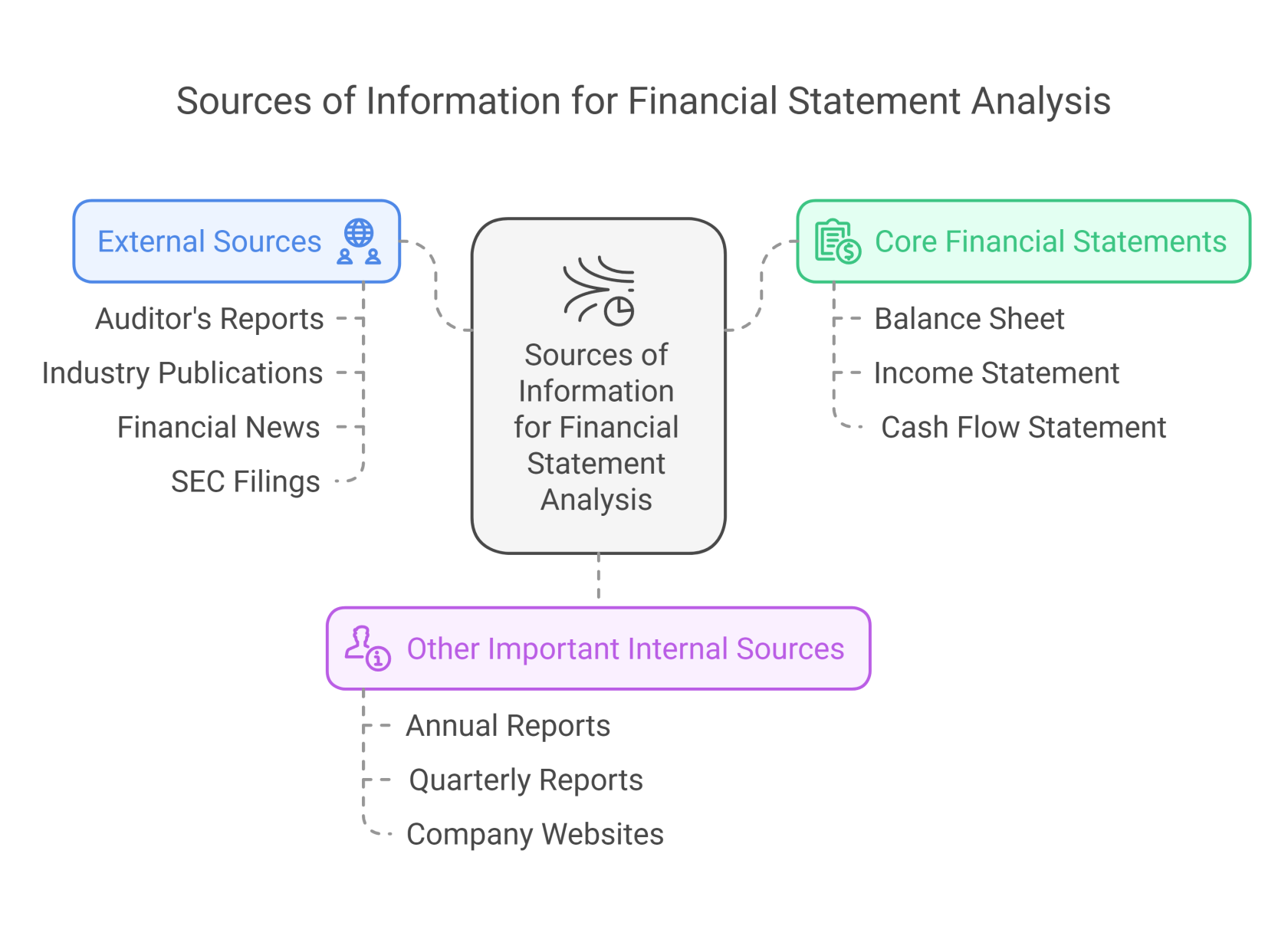

Sources of Information for Financial Statement Analysis

As we've established, financial statement analysis relies on a variety of data sources. These sources can be categorized, and each plays a unique role in providing a holistic view of a company's financial health. Let's explore these in more detail:

1. The Core Financial Statements

These are the primary documents that form the basis of any financial analysis.

Balance Sheet:

- What it is: A snapshot of a company's assets (what it owns), liabilities (what it owes), and equity (the owner's stake) at a specific point in time. It's like a company's financial "selfie" on a given date.

-

Information Provided:

-

Assets:

- Current Assets: Cash, accounts receivable (money owed by customers), inventory, and other assets that can be converted to cash within a year.

- Non-Current Assets: Property, plant, and equipment (PP&E), intangible assets (like patents), and long-term investments.

-

Liabilities:

- Current Liabilities: Accounts payable (money owed to suppliers), short-term debt, and other obligations due within a year.

- Non-Current Liabilities: Long-term debt, mortgages, and other obligations due beyond a year.

-

Equity:

- Share Capital: Funds invested by shareholders.

- Retained Earnings: Accumulated profits that have not been distributed to shareholders.

-

Assets:

- Importance: The balance sheet helps assess a company's financial stability, solvency (ability to meet long-term obligations), and capital structure. It reveals how a company funds its operations and what resources it has at its disposal.

Income Statement (or Profit & Loss Statement):

- What it is: A report that summarizes a company's financial performance over a period of time (usually a quarter or a year). It shows revenues, expenses, and ultimately, profit.

-

Information Provided:

- Revenues (or Sales): The money earned from the company's core business activities.

- Cost of Goods Sold (COGS): The direct costs associated with producing goods sold (for manufacturing or retail companies).

- Gross Profit: Revenue minus COGS, showing the profitability of a company's core business.

- Operating Expenses: Costs related to running the business (e.g., salaries, rent, utilities, marketing).

- Operating Income (or Profit): Gross profit minus operating expenses, showing profit from day-to-day operations.

- Interest Expense: The cost of borrowing money.

- Taxes: Amount paid to the government.

- Net Income (or Profit): The final profit after all expenses (including taxes).

- Importance: The income statement is used to assess a company's profitability, efficiency, and ability to generate revenue. It shows how well a company manages its operations to achieve profit.

Cash Flow Statement:

- What it is: A report that tracks the movement of cash in and out of a company over a period of time.

-

Information Provided:

- Cash Flow from Operating Activities: Cash generated or used by the company's core business operations (e.g., selling goods, providing services).

- Cash Flow from Investing Activities: Cash flows related to purchasing or selling long-term assets (e.g., property, equipment, investments).

- Cash Flow from Financing Activities: Cash flows related to borrowing or repaying debt, issuing or repurchasing stock, and paying dividends.

- Net Increase (or Decrease) in Cash: The overall change in cash over the period.

- Importance: The cash flow statement helps assess a company's liquidity (ability to meet short-term obligations), its sources of cash, and its uses of cash. It provides insights into how a company funds its operations and growth.

2. Other Important Internal Sources

Beyond the core financial statements, these internal documents offer more detailed information.

Annual Reports:

- What it is: A comprehensive report published by companies at the end of each fiscal year.

-

Information Provided: Besides the three financial statements, annual reports often include:

- Management's Discussion and Analysis (MD&A): Commentary from management on the company's performance, risks, and future outlook.

- Detailed notes to the Financial Statements: Provides additional context for items in the financial statements.

- Auditor's Report: An opinion from an independent auditor on the fairness of the financial statements.

- Corporate Governance information: Details about the company's structure and board of directors.

- Importance: The annual report provides a wealth of contextual information and management's perspective.

Quarterly Reports:

- What it is: Similar to annual reports but issued every three months.

- Information Provided: Condensed versions of the three financial statements, along with brief management commentary.

- Importance: Quarterly reports offer more frequent updates on a company's performance, enabling investors and other stakeholders to keep up with the latest trends.

Company Websites (Investor Relations Sections):

- What it is: The dedicated section of the company's website that provides financial information for investors.

- Information Provided: Access to financial statements, investor presentations, press releases, and SEC filings.

- Importance: Company websites often provide easy access to financial data and investor-related information.

3. External Sources

These resources offer independent perspectives and comparative data.

Auditor's Reports:

- What it is: An independent opinion from a certified public accountant on the fairness of a company's financial statements.

- Information Provided: Assurance (or otherwise) that the financial statements are presented fairly and are in accordance with Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS).

- Importance: Provides credibility and assurance to users of the financial statements.

Industry Publications and Databases:

- What it is: Reports, articles, and data from reputable sources that analyze industries and their performance.

- Information Provided: Industry trends, benchmarks, competitor data, market analysis, and forecasts.

- Importance: Enables comparative analysis of a company's performance against its peers and overall industry trends.

Financial News and Analysis:

- What it is: Reports, articles, and analyses from reputable financial news outlets (e.g., Wall Street Journal, Bloomberg, Financial Times).

- Information Provided: Market insights, economic data, company-specific news, and expert opinions on company performance.

- Importance: Provides context for a company's financial performance in light of broader economic and market trends.

SEC (Securities and Exchange Commission) Filings

- What it is: Public companies are required to submit periodic reports (10-K annual, 10-Q quarterly) with the SEC. These contain detailed financial information and disclosures.

- Information Provided: Detailed financial statements, management discussions, risk factors and much more.

- Importance: These filings are official sources of information and are subject to scrutiny.

No Comments