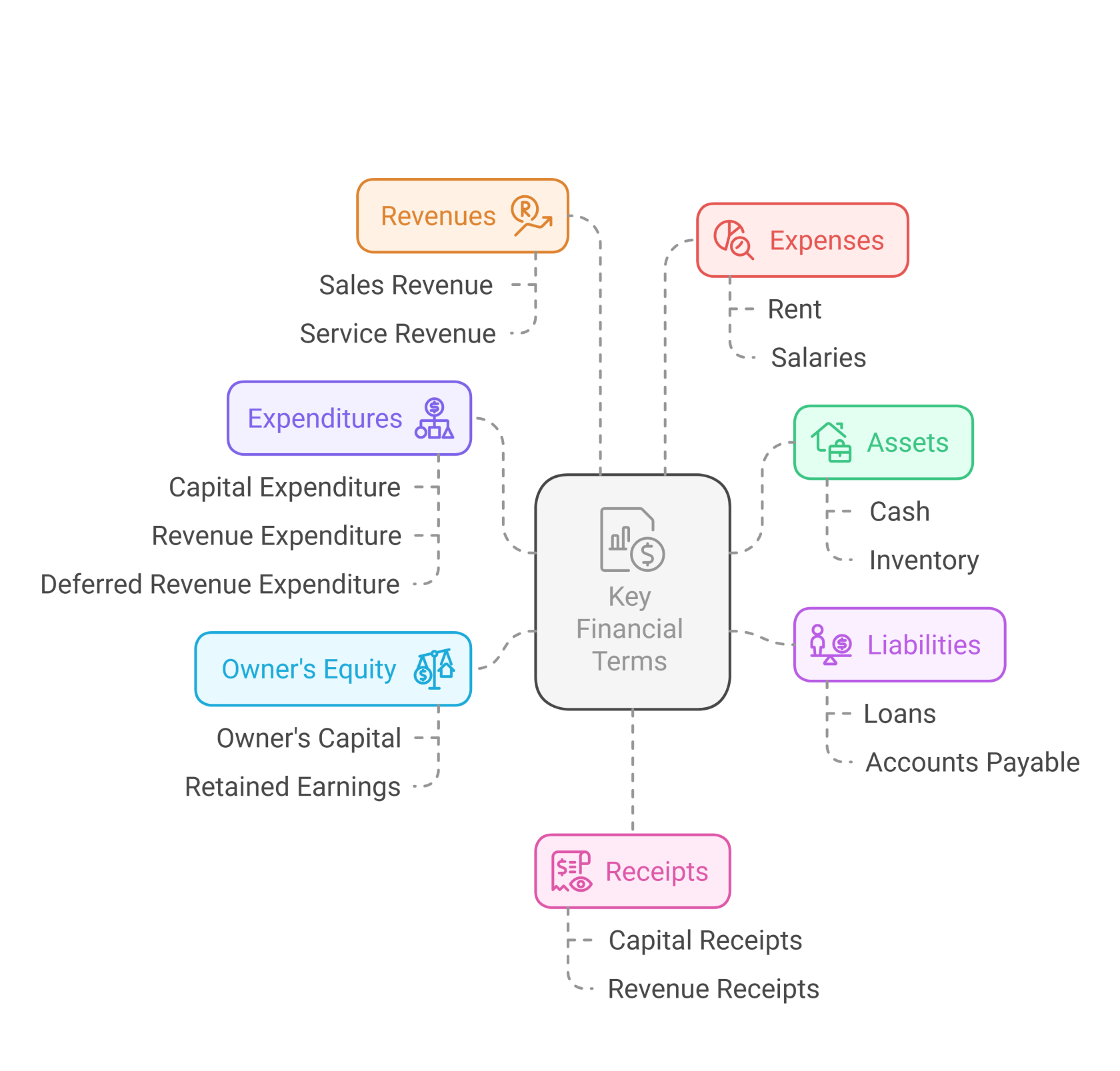

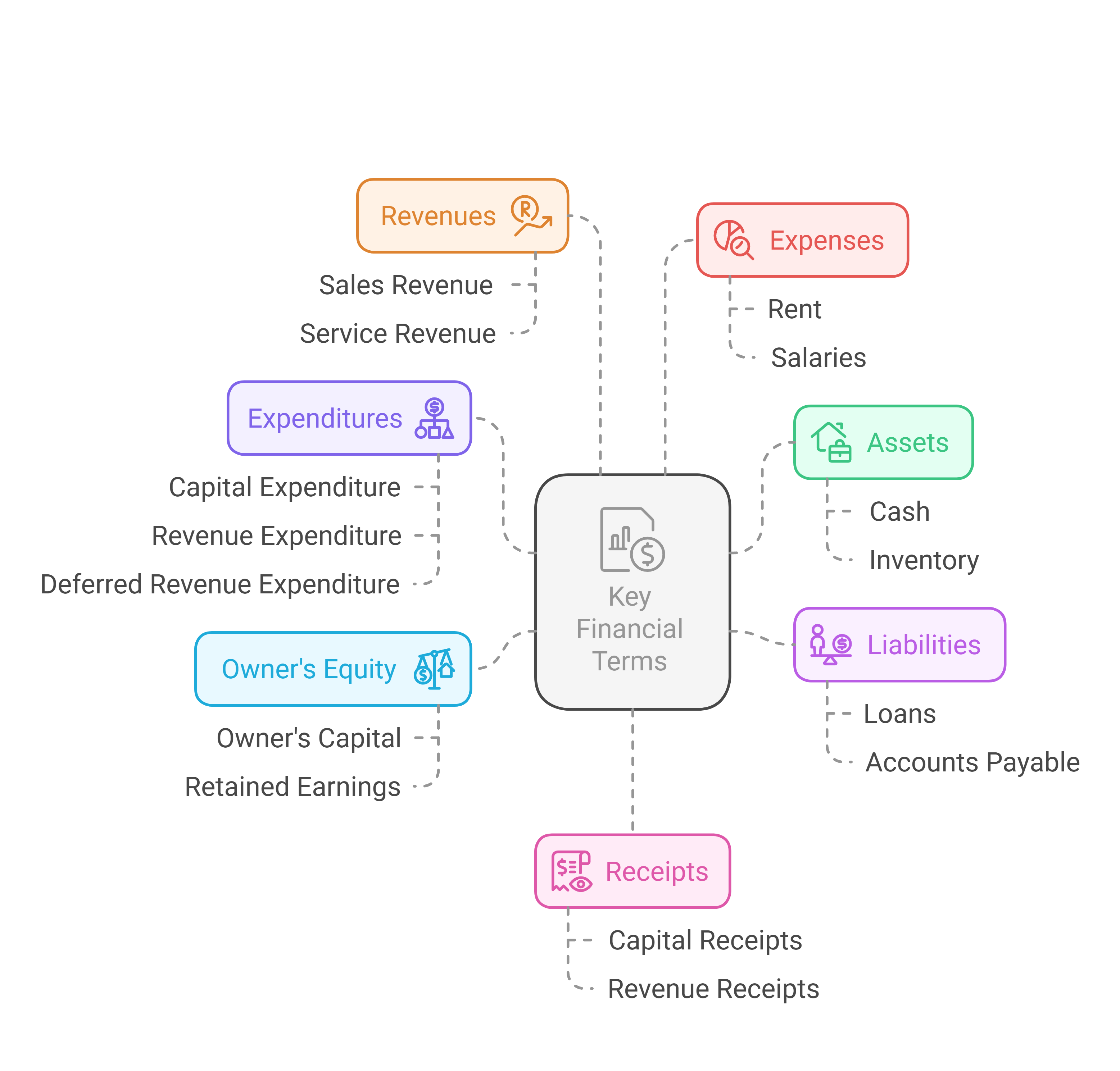

Key Financial Terms

Understanding Key Financial Terms

Let's break down some essential financial terms that are crucial for understanding how businesses operate.

The Building Blocks: Assets, Liabilities, and Owner's Equity

Imagine a business as a building. These three elements are the foundation:

-

Assets: These are what the business owns. Think of them as the building itself, the land it sits on, the equipment inside, and any money it has. Assets are expected to provide future economic benefit. Examples include:

- Cash: Money in hand or in the bank.

- Accounts Receivable: Money owed to the business by customers.

- Inventory: Goods held for sale.

- Equipment: Machinery, computers, vehicles.

- Buildings: Offices, factories, stores.

- Land: Property owned by the business.

-

Liabilities: These are what the business owes to others. Think of them as loans, debts, or obligations. Examples include:

- Accounts Payable: Money owed to suppliers.

- Loans: Money borrowed from banks or other lenders.

- Salaries Payable: Money owed to employees.

-

Owner's Equity (or just Equity): This is the owner's stake in the business. It's what's left over after liabilities are subtracted from assets. Think of it as the owner's investment plus any accumulated profits.

- Owner's Capital: The original investment by the owner(s).

- Retained Earnings: Profits accumulated over time.

- Drawings: Money taken out of the business by the owner(s).

The relationship between these three is expressed in the accounting equation:

Assets = Liabilities + Owner's Equity

The Flow of Money: Revenues and Expenses

Now, let's look at how money flows in and out of the business:

-

Revenues: These are the money the business earns from its operations. Think of it as the money coming in from sales or services. Examples include:

- Sales Revenue: Money from selling goods.

- Service Revenue: Money from providing services.

- Interest Revenue: Money earned from interest on investments.

-

Expenses: These are the costs the business incurs to generate revenue. Think of them as the money going out to pay for things needed to run the business. Examples include:

- Rent: Cost of office or store space.

- Salaries: Payments to employees.

- Utilities: Costs of electricity, water, etc.

- Advertising: Costs of marketing and promotion.

Classifying Spending: Capital vs. Revenue Expenditure

Businesses spend money on various things. It's important to distinguish between:

-

Capital Expenditure: Spending on assets that will benefit the business for more than one year. These are long-term investments. Think of it as buying a new building or a major piece of equipment. These increase the value of assets.

-

Revenue Expenditure: Spending on day-to-day expenses that keep the business running. These are short-term costs. Think of it as paying rent, salaries, or utilities. These are expensed immediately.

-

Deferred Revenue Expenditure: This is a type of expenditure that, while initially treated as a revenue expenditure, provides benefits over several accounting periods. The cost is spread out over the periods it benefits. A common example is heavy advertising or promotional campaigns.

Classifying Income: Capital vs. Revenue Receipts

Similarly, businesses receive money from different sources:

-

Capital Receipts: Money received from the sale of long-term assets or from new equity contributions. These are not part of the regular operating revenue. Think of it as selling a building or receiving an investment from a new partner.

-

Revenue Receipts: Money received from the normal day-to-day operations of the business (sales, services). This is the regular income.

No Comments