Commercial Banking

Commercial banks are the linchpin of the modern financial system, acting as vital intermediaries between savers and borrowers and facilitating the smooth flow of funds throughout the economy. This document explores the multifaceted role of commercial banks, the challenges they face, particularly with Non-Performing Assets (NPAs), and the critical importance of effective risk management.

1. Role of Commercial Banks: Fueling Economic Growth

Commercial banks play a pivotal role in the economy by performing a variety of essential functions:

- Deposit Taking: Commercial banks accept deposits from individuals, businesses, and institutions, providing a safe and convenient place to store savings. These deposits form the foundation of the bank's lending activities. In return, banks offer interest to depositors, incentivizing them to save.

- Credit Creation: Banks are not simply custodians of money; they also create credit by lending a portion of their deposits to borrowers. This lending process multiplies the money supply in the economy and stimulates economic activity. The amount of credit a bank can create is limited by regulations and its own risk management policies.

-

Loan Provisioning: Commercial banks provide a diverse range of loans to meet the varied needs of individuals, businesses, and governments. These loans can be short-term or long-term and are used for various purposes, such as:

- Business Loans: Used for expansion, working capital, equipment purchases, and other business needs.

- Home Loans (Mortgages): Used by individuals to purchase residential properties.

- Car Loans: Used by individuals to finance the purchase of vehicles.

- Personal Loans: Used by individuals for a variety of purposes, such as education, medical expenses, and debt consolidation.

-

Facilitating Payments: Commercial banks are essential to the payment system, enabling transactions through various channels, including:

- Cheques: Traditional paper-based payment instruments.

- Wire Transfers: Electronic transfers of funds between bank accounts.

- Credit Cards and Debit Cards: Widely used for retail transactions.

- Digital Wallets: Mobile-based payment systems that allow users to make purchases using their smartphones.

-

Wealth Management: Many commercial banks offer wealth management services to assist individuals and businesses in managing their funds, providing investment advice, and planning for the future. These services may include:

- Investment Advisory: Providing guidance on investment strategies and asset allocation.

- Portfolio Management: Managing investment portfolios on behalf of clients.

- Financial Planning: Helping clients plan for retirement, education, and other financial goals.

-

Foreign Exchange Services: Commercial banks facilitate international trade and investment by providing foreign exchange services, including:

- Currency Conversion: Converting one currency into another.

- Trade Finance: Providing financing for international trade transactions.

- Hedging Services: Helping businesses manage currency risk.

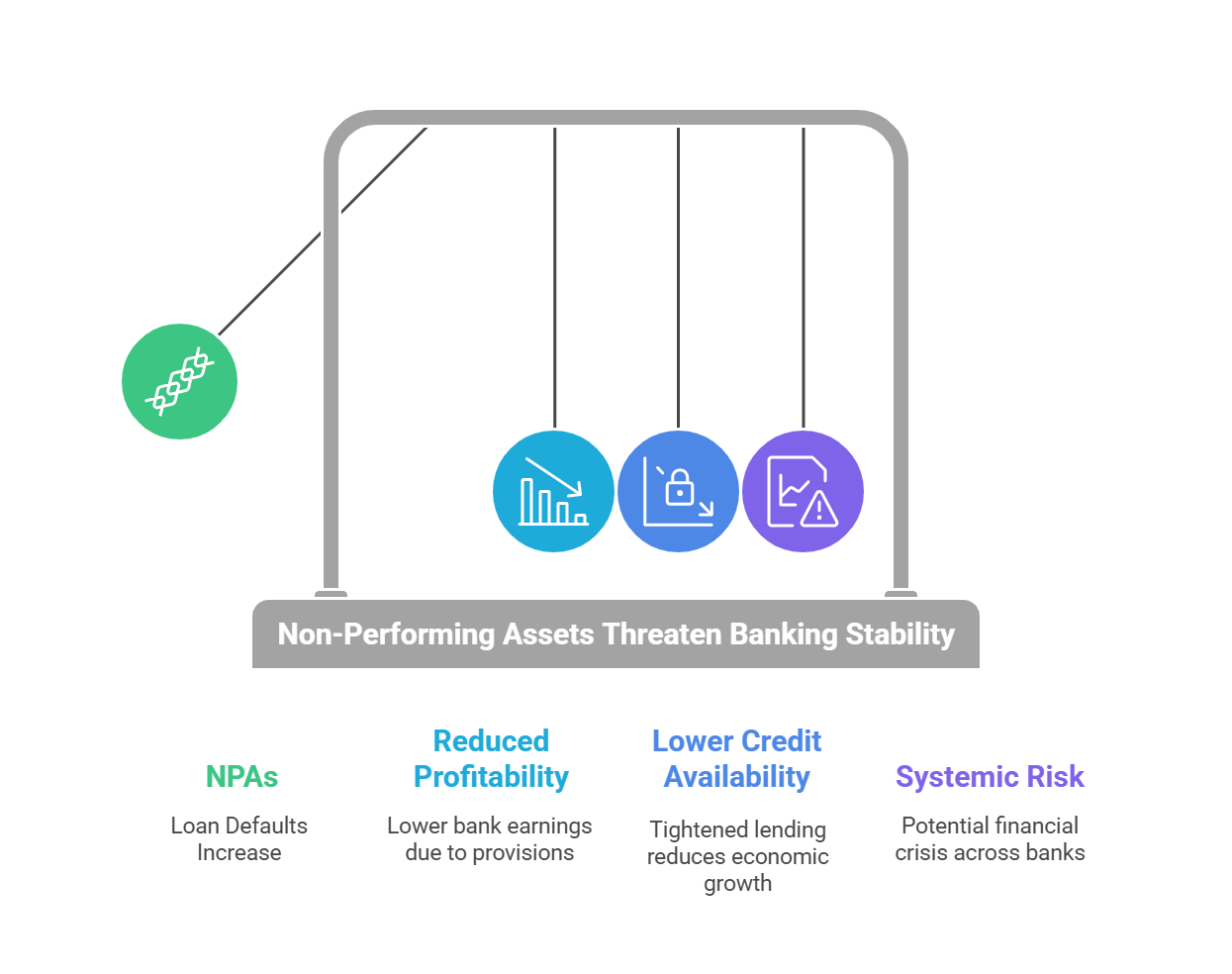

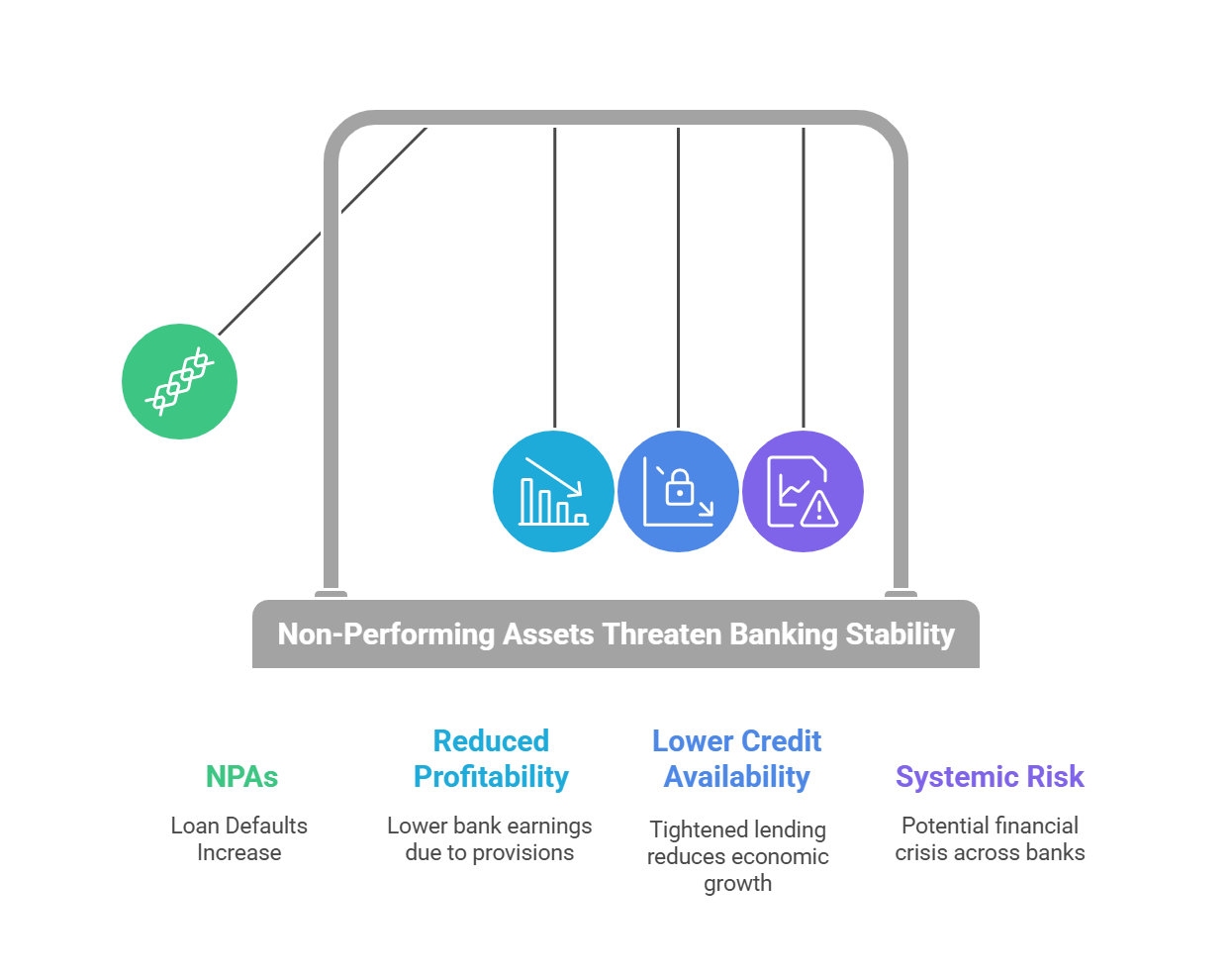

2. Non-Performing Assets (NPAs): A Threat to Bank Stability

Non-Performing Assets (NPAs) are loans or advances where the borrower has defaulted on their repayment obligations. Specifically, an asset becomes an NPA when the borrower has failed to make interest or principal payments for a specified period, typically 90 days. NPAs pose a significant threat to the financial health of commercial banks and the overall economy.

-

Classification of NPAs:

- Substandard Assets: Loans that have been non-performing for less than 12 months. These assets are considered to have a higher risk of default than standard assets.

- Doubtful Assets: Loans that have remained non-performing for more than 12 months. The recoverability of these assets is considered doubtful.

- Loss Assets: Loans that are considered uncollectible or partially collectable and have been written off by the bank. These assets represent a significant loss to the bank.

-

Causes of NPAs: Several factors can contribute to the formation of NPAs:

- Economic Downturns: A slowdown in economic growth can lead to defaults as businesses and individuals struggle to repay their loans.

- Poor Credit Appraisal: Inadequate assessment of the borrower's ability to repay can lead to a high incidence of defaults. This can result from insufficient due diligence or a lack of expertise in assessing credit risk.

- Fraud and Mismanagement: Some NPAs arise due to fraudulent activities or mismanagement by borrowers or financial institutions. This can involve diversion of funds, falsification of documents, or insider lending.

- Overexposure to High-Risk Sectors: Lending heavily to sectors that are prone to high risk, such as infrastructure and real estate, can result in NPAs if those sectors face a downturn.

- Regulatory Failures: Lack of strong regulatory oversight and enforcement can allow weak lending practices to persist, leading to increased NPA levels.

-

Impact of NPAs: High levels of NPAs can have a detrimental impact on commercial banks and the economy:

- Reduced Profitability: Banks are required to make provisions for NPAs, which reduces their profitability. The more NPAs a bank has, the less profitable it becomes.

- Lower Credit Availability: High NPA levels can make banks more cautious about lending, leading to a tightening of credit and hindering economic growth.

- Capital Adequacy: NPAs can erode a bank's capital base, making it more difficult to meet regulatory capital adequacy requirements. This can limit the bank's ability to expand its lending activities.

- Systemic Risk: High NPA levels across the banking sector can create systemic risk, potentially leading to a financial crisis.

-

Measures to Address NPAs: The Indian government and the RBI have implemented several measures to address the problem of NPAs:

- Insolvency and Bankruptcy Code (IBC): The IBC provides a legal framework for resolving insolvency cases and recovering dues from defaulting borrowers in a time-bound manner. This has significantly improved the recovery rates for banks.

- Debt Recovery Tribunals (DRTs): DRTs are specialized tribunals that expedite the recovery of debts owed to banks and financial institutions.

- SARFAESI Act: The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act allows banks to take possession of assets pledged as collateral and sell them to recover their dues without court intervention.

- Prudential Norms: The RBI has issued guidelines on the recognition, classification, and provisioning of NPAs to ensure timely action by banks.

- Asset Reconstruction Companies (ARCs): ARCs purchase NPAs from banks at a discount and attempt to recover the dues.

3. Risk Management in Banks: Navigating Uncertainties

Banks operate in a complex and ever-changing environment, facing a variety of risks that can impact their financial stability and profitability. Effective risk management is therefore crucial for the long-term success of commercial banks.

-

Types of Risks Faced by Banks:

-

Credit Risk: The risk that a borrower will default on a loan or fail to meet their repayment obligations. This is one of the most significant risks faced by banks.

-

Management Strategies:

- Credit Appraisal: Thoroughly assessing the creditworthiness of borrowers before granting loans.

- Diversification of Loan Portfolios: Spreading lending across different sectors and industries to reduce concentration risk.

- Risk-Based Pricing: Charging higher interest rates to borrowers with higher credit risk.

- Monitoring of Borrower Repayment Behavior: Regularly monitoring borrowers' repayment performance and taking prompt action when problems arise.

-

Management Strategies:

-

Market Risk: The risk of losses due to changes in market conditions, such as interest rates, currency exchange rates, and stock prices.

-

Management Strategies:

- Hedging: Using financial instruments, such as derivatives, to mitigate market risks.

- Value-at-Risk (VaR) Models: Using statistical models to measure potential losses under different market conditions.

- Stress Testing: Evaluating the bank's resilience to extreme market events.

-

Management Strategies:

-

Liquidity Risk: The risk that a bank may not be able to meet its short-term obligations due to insufficient cash or liquid assets.

-

Management Strategies:

- Maintaining Adequate Cash Reserves: Holding sufficient cash and liquid assets to meet unexpected withdrawals and payment obligations.

- Monitoring the Liquidity Coverage Ratio (LCR): Maintaining a minimum LCR, which is the ratio of liquid assets to short-term liabilities.

- Accessing Short-Term Borrowing Facilities: Having access to borrowing facilities, such as the interbank market and the repo market, to meet short-term funding needs.

-

Management Strategies:

-

Operational Risk: The risk of loss due to failures in internal processes, systems, or human error.

-

Management Strategies:

- Establishing Strong Internal Controls: Implementing robust internal controls to prevent fraud, errors, and other operational failures.

- Conducting Regular Audits: Conducting regular internal and external audits to identify and address weaknesses in internal controls.

- Implementing Robust Risk Mitigation Strategies: Developing disaster recovery plans, cybersecurity measures, and other strategies to mitigate operational risks.

-

Management Strategies:

-

Interest Rate Risk: The risk of loss due to changes in interest rates affecting a bank's profitability and the value of its assets and liabilities.

-

Management Strategies:

- Asset-Liability Management (ALM): Matching the maturities and interest rate sensitivities of assets and liabilities.

- Hedging through Interest Rate Derivatives: Using interest rate swaps and other derivatives to hedge against interest rate risk.

-

Management Strategies:

-

Reputational Risk: The risk of damage to a bank's reputation due to adverse events, such as fraud, regulatory violations, or negative publicity.

-

Management Strategies:

- Strong Corporate Governance: Establishing a strong ethical culture and ensuring accountability at all levels of the organization.

- Transparent Operations: Operating in a transparent and ethical manner.

- Effective Communication: Communicating openly and honestly with stakeholders.

- Customer Satisfaction Initiatives: Providing excellent customer service and addressing customer complaints promptly.

-

Management Strategies:

-

Credit Risk: The risk that a borrower will default on a loan or fail to meet their repayment obligations. This is one of the most significant risks faced by banks.

-

Risk Management Framework: A comprehensive risk management framework is essential for effective risk management. Such a framework typically includes the following elements:

- Risk Identification: Identifying all potential risks associated with the bank's operations, assets, and liabilities.

- Risk Assessment and Measurement: Quantifying the likelihood and impact of each identified risk.

- Risk Mitigation: Developing and implementing strategies to reduce or control risk exposure.

- Monitoring and Reporting: Continuously tracking risk levels and reporting to senior management and regulators.

-

Review and Improvement: Regularly reviewing the risk management framework and making improvements as needed.

Summary:

- Role of Commercial Banks: Commercial banks are vital intermediaries that mobilize savings, provide credit, facilitate payments, and contribute to economic growth.

- Non-Performing Assets (NPAs): NPAs pose a significant threat to bank stability and profitability. Effective recovery and resolution mechanisms, such as the IBC, are essential for managing NPAs.

- Risk Management in Banks: Banks must manage various risks, including credit, market, liquidity, operational, and reputational risks. A comprehensive risk management framework is essential for effective risk management.

By fulfilling their role effectively, managing risks prudently, and maintaining financial stability, commercial banks play a crucial role in supporting economic growth and prosperity.

No Comments