Regulatory Institutions in India

India's robust financial system is overseen by a network of regulatory institutions, each playing a crucial role in maintaining stability, ensuring transparency, and fostering the smooth functioning of various sectors. These institutions are tasked with safeguarding the interests of consumers, investors, and the overall economy. This document provides a comprehensive overview of the key regulatory institutions in India.

1. Reserve Bank of India (RBI): The Central Bank and Apex Regulator

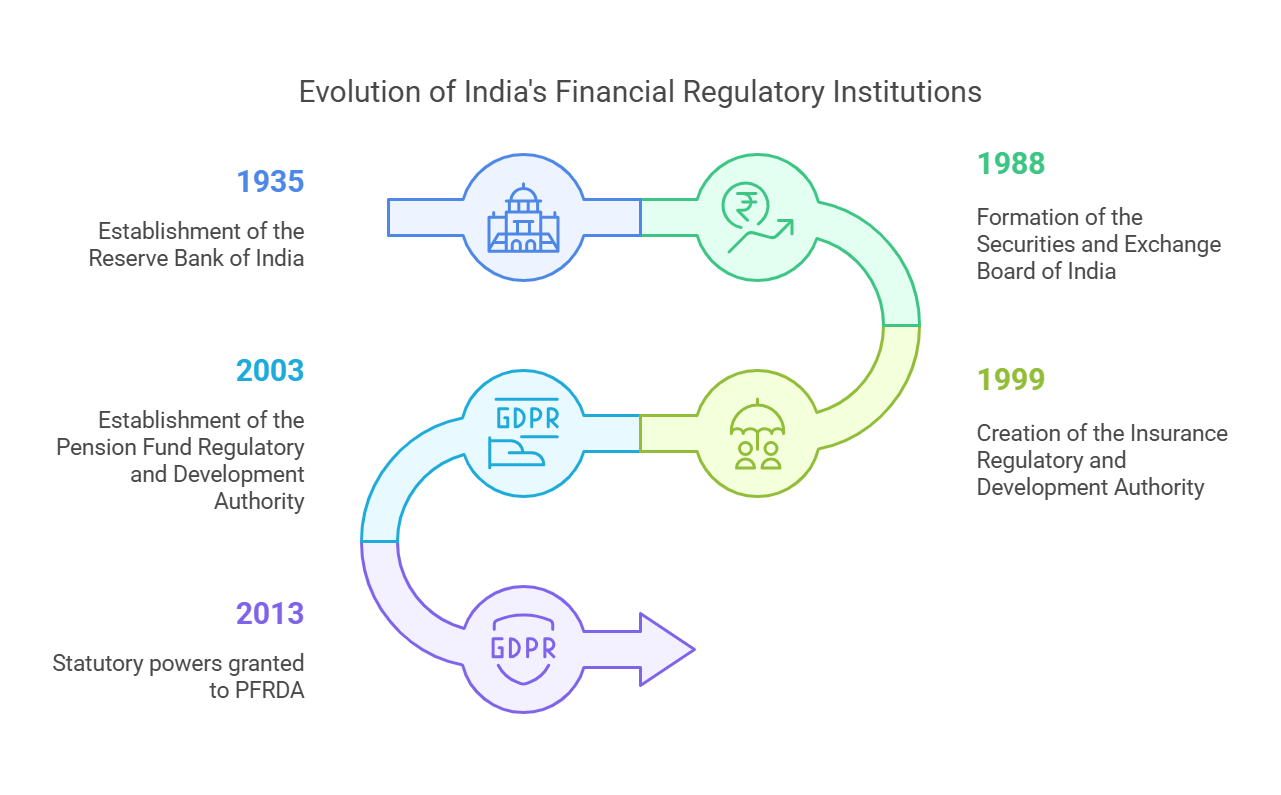

- Overview: The Reserve Bank of India (RBI) is the central bank of India and the primary regulatory authority for the Indian financial system. Established in 1935 under the Reserve Bank of India Act, 1934, it is the cornerstone of India's financial architecture.

-

Functions:

- Monetary Policy: The RBI formulates and implements monetary policy to regulate inflation, manage interest rates, control the money supply, and ensure price stability in the economy. This involves setting key interest rates like the repo rate, reverse repo rate, and cash reserve ratio (CRR).

- Currency Issuance: The RBI has the exclusive right to issue and manage currency in India. It is responsible for printing, distributing, and managing the supply of banknotes in circulation.

- Regulation of Banks and Financial Institutions: The RBI regulates and supervises all scheduled commercial banks (both public and private sector), cooperative banks, and other non-banking financial companies (NBFCs) in India. This includes setting capital adequacy requirements, conducting inspections, and issuing guidelines on lending practices.

- Foreign Exchange Management: The RBI manages the foreign exchange reserves of India and is responsible for regulating the foreign exchange market. It intervenes in the market to stabilize the exchange rate of the Indian rupee and manage capital flows.

- Payment and Settlement Systems: The RBI oversees the payment and settlement systems to ensure smooth and secure financial transactions. This includes regulating payment gateways, electronic fund transfers, and other payment technologies. It also promotes the development of efficient and innovative payment systems.

- Banker to the Government: The RBI acts as the banker to the central and state governments, managing their accounts, providing loans, and advising them on financial matters.

- Lender of Last Resort: The RBI serves as the lender of last resort, providing emergency funds to banks and financial institutions facing liquidity crises, thereby preventing systemic failures.

- Key Role: The RBI acts as the guardian of the Indian financial system, maintaining financial stability, promoting economic growth, and safeguarding the interests of depositors and the public. It plays a critical role in managing macroeconomic stability and ensuring the overall health of the Indian economy.

2. Securities and Exchange Board of India (SEBI): Protecting Investors and Ensuring Market Integrity

- Overview: The Securities and Exchange Board of India (SEBI) was established in 1988 and later became a statutory body in 1992 under the SEBI Act, 1992. It is the primary regulator for the securities and capital markets in India.

-

Functions:

- Regulation of Capital Markets: SEBI formulates regulations for the securities market, including stock exchanges, brokers, mutual funds, investment advisors, and other market participants. This involves setting rules for listing, trading, and disclosure requirements.

- Investor Protection: SEBI works to protect the interests of investors by ensuring transparency, fair practices, and efficient functioning of the securities markets. It investigates complaints from investors and takes action against fraudulent and manipulative activities.

- Market Surveillance: SEBI monitors the trading activities on stock exchanges to detect and prevent market manipulation, insider trading, and other fraudulent practices. It uses sophisticated surveillance systems to identify suspicious transactions and patterns.

- Regulation of Mutual Funds and Derivatives Markets: SEBI oversees mutual funds, portfolio managers, and derivatives markets to ensure their compliance with regulations and investor protection. It sets rules for the operation, management, and disclosure practices of these entities.

- Promoting Market Development: SEBI promotes the development of the securities market by introducing new products, technologies, and trading practices.

- Enforcement: SEBI has the power to investigate and take enforcement actions against individuals and entities violating securities laws, including issuing penalties, barring individuals from the market, and prosecuting offenders.

- Key Role: SEBI promotes transparency, integrity, and confidence in the securities market, ensuring that investors have access to accurate information and that markets operate in a fair and efficient manner. It plays a vital role in fostering the growth and development of the Indian capital market.

3. Insurance Regulatory and Development Authority of India (IRDAI): Fostering a Stable and Growing Insurance Sector

- Overview: The Insurance Regulatory and Development Authority of India (IRDAI) was established in 1999 under the IRDA Act, 1999. It is the regulatory body responsible for overseeing and promoting the insurance industry in India.

-

Functions:

- Regulation of Insurance Companies: IRDAI grants licenses to insurance companies to operate in India and sets the rules and regulations for their operations. It ensures that insurers meet solvency requirements and maintain sound financial practices.

- Product Approvals: IRDAI approves the terms and conditions of insurance products offered by insurers and ensures that policies are transparent, fair, and consumer-friendly. It reviews policy documents to ensure they are clear and easy to understand.

- Solvency and Financial Health: IRDAI ensures that insurance companies maintain adequate solvency margins and have the financial capacity to meet their liabilities and pay claims to policyholders. It monitors the financial performance of insurers and takes corrective action when necessary.

- Consumer Protection: IRDAI safeguards the interests of policyholders by ensuring that companies follow ethical business practices, handle claims fairly, and address consumer grievances promptly. It establishes guidelines for grievance redressal mechanisms and ensures that insurers comply with these guidelines.

- Promotion of Insurance Penetration: IRDAI works to increase insurance penetration in India by encouraging innovation, promoting awareness, and developing new distribution channels.

- Setting Standards: IRDAI sets standards for insurance agents and brokers and conducts training and certification programs.

- Key Role: IRDAI fosters the growth of the insurance industry in India by encouraging innovation, ensuring financial stability, protecting policyholders, and promoting wider insurance coverage.

4. Pension Fund Regulatory and Development Authority (PFRDA): Securing Retirement Futures

- Overview: The Pension Fund Regulatory and Development Authority (PFRDA) was established in 2003 and given statutory powers in 2013 under the PFRDA Act, 2013. It regulates and develops the pension sector in India, with a particular focus on the National Pension System (NPS).

-

Functions:

- Regulation of Pension Schemes: PFRDA regulates and oversees pension funds and the NPS, which provides retirement savings options for employees in the organized sector, as well as for self-employed individuals. It sets rules for the management, investment, and distribution of pension funds.

- Development of Pension Markets: PFRDA encourages the development of the pension sector by promoting private participation, improving pension coverage in India, and introducing innovative pension products.

- Investor Protection: The PFRDA ensures that pension funds are managed transparently, and the interests of pensioners are safeguarded. It sets rules for disclosure, reporting, and grievance redressal.

- Operational Supervision: PFRDA monitors the functioning of pension funds and ensures that they comply with regulations and follow best practices. It conducts inspections and audits to ensure compliance.

- Promoting Awareness: PFRDA promotes awareness about the importance of retirement planning and encourages individuals to participate in pension schemes.

- Key Role: PFRDA plays a crucial role in securing the financial future of citizens by regulating pension funds, promoting retirement savings schemes, and ensuring that pensioners have access to a reliable and sustainable income stream after retirement.

Summary of Regulatory Institutions and Their Roles

| Regulatory Institution | Key Functions | Key Role |

|---|---|---|

| Reserve Bank of India (RBI) | Monetary policy, currency issuance, regulation of banks and financial institutions, foreign exchange management, payment and settlement systems. | Maintaining financial stability, controlling inflation, promoting economic growth, regulating the banking sector. |

| Securities and Exchange Board of India (SEBI) | Regulation of capital markets, investor protection, market surveillance, regulation of mutual funds and derivatives markets. | Ensuring transparency, fairness, and integrity in the securities market, protecting investors' interests. |

| Insurance Regulatory and Development Authority of India (IRDAI) | Regulation of insurance companies, product approvals, solvency and financial health, consumer protection. | Promoting the growth of the insurance industry, ensuring financial stability, protecting policyholders. |

| Pension Fund Regulatory and Development Authority (PFRDA) | Regulation of pension schemes, development of pension markets, investor protection, operational supervision. | Securing the financial future of citizens by regulating pension funds and promoting retirement savings schemes. |

Each of these regulatory bodies plays a vital role in maintaining the stability, integrity, and efficiency of India's financial system. They work to ensure that markets operate in a fair, transparent, and efficient manner, protecting the interests of consumers, investors, and the overall economy. The effectiveness of these institutions is critical to India's continued economic growth and development.

No Comments