Types of Financial Markets: The Money Market

The money market is a crucial component of the financial system, facilitating short-term borrowing and lending. This document provides a comprehensive overview of the money market, its objectives, key instruments, participants, and its importance in India.

The Money Market: Where Short-Term Funds Meet

The money market is a segment of the financial market that deals with short-term borrowing and lending, typically with maturities of one year or less. It focuses on highly liquid and low-risk instruments, making it a safe haven for short-term investments. The money market is essential for managing liquidity in the financial system and meeting the short-term financing needs of governments, financial institutions, and corporations.

Objectives of the Money Market:

- Liquidity Management: Provides a platform for institutions and governments to manage their short-term cash flow needs.

- Facilitating Short-Term Borrowing and Lending: Enables financial institutions and corporations to raise short-term funds quickly and efficiently.

- Interest Rate Control: Helps regulate short-term interest rates, influenced by the monetary policy of the central bank (RBI in India).

- Monetary Policy Implementation: The RBI utilizes tools like repo and reverse repo operations in the money market to control the money supply and influence interest rates.

- Balancing Mechanism: Provides a balancing mechanism to even out the demand for and supply of short-term funds.

- Focal Point for Intervention: Provides a focal point for central bank intervention for influencing liquidity and general level of interest rates in the economy.

-

Reasonable Access: Provides reasonable access to suppliers and users of short-term funds to fulfill their borrowings and investment requirements at an efficient market clearing price.

Key Instruments Traded in the Money Market:

The money market utilizes a variety of financial instruments for short-term borrowing and lending:

-

Treasury Bills (T-Bills):

- Definition: Short-term debt instruments issued by the Government of India with maturities of 91 days, 182 days, or 364 days.

- Purpose: Used to meet the government's short-term funding requirements.

- Features: Highly liquid, low-risk instruments issued at a discount to their face value. They do not pay interest but are redeemed at par value at maturity.

- Market: Issued through regular auctions by the RBI.

-

Certificates of Deposit (CDs):

- Definition: Time deposits issued by banks and financial institutions for a fixed term, generally ranging from 7 days to one year.

- Purpose: Used by banks to raise short-term funds from the market.

- Features: Carry a fixed interest rate and are issued at a discount to their face value. They can be bought and sold in the secondary market.

- Market: Available in the interbank market and traded among banks, financial institutions, and other qualified investors.

-

Commercial Papers (CPs):

- Definition: Unsecured, short-term debt instruments issued by corporations, typically with maturities ranging from 7 days to one year.

- Purpose: Used by companies to meet short-term funding needs like working capital requirements.

- Features: Issued at a discount to face value and bear an interest rate that is typically higher than that of T-bills and CDs, reflecting the higher credit risk.

- Market: Issued in the primary market and can be traded in the secondary market.

-

Repurchase Agreements (Repos) and Reverse Repos:

- Definition: A repurchase agreement is a short-term borrowing mechanism where one party sells securities (usually government securities) to another party with an agreement to repurchase them at a later date at a higher price. The reverse repo is the counterpart transaction where the buyer agrees to sell back the securities at a later date.

- Purpose: Used by financial institutions and the RBI for liquidity management.

- Features: The repo rate is the rate at which the RBI lends to commercial banks, while the reverse repo rate is the rate at which the RBI borrows from commercial banks.

- Market: Typically conducted in the interbank market.

-

Call Money Market:

- Definition: Deals with very short-term borrowings (typically overnight) between financial institutions, such as commercial banks.

- Purpose: Used to meet the liquidity requirements of banks. A bank with surplus funds can lend them to another bank facing a liquidity shortfall.

- Features: Borrowing and lending are typically done for a single day (24 hours), and the interest rate is called the call money rate.

- Market: The rate fluctuates based on the supply and demand for funds in the banking system.

-

Cash Management Bills (CMBs):

- Definition: Short-term debt instruments issued by the Government of India to manage temporary liquidity mismatches.

- Purpose: Issued by the RBI on behalf of the government for short-term government financing.

- Features: Issued for a period less than 91 days and are a tool to manage the government’s cash requirements.

- Market: Primarily purchased by institutional investors, such as banks and financial institutions.

-

Banker's Acceptance (BA):

- Definition: A short-term debt instrument issued by a borrower and guaranteed by a bank.

- Purpose: Used for financing international trade transactions, facilitating payment between buyers and sellers.

- Features: The BA is sold at a discount and redeemed at face value at maturity.

- Market: Typically traded in the secondary market.

-

Short-Term Borrowings by Banks:

- Banks also engage in short-term borrowing from other financial institutions or through instruments like interbank deposits and term deposits.

- Banks also engage in short-term borrowing from other financial institutions or through instruments like interbank deposits and term deposits.

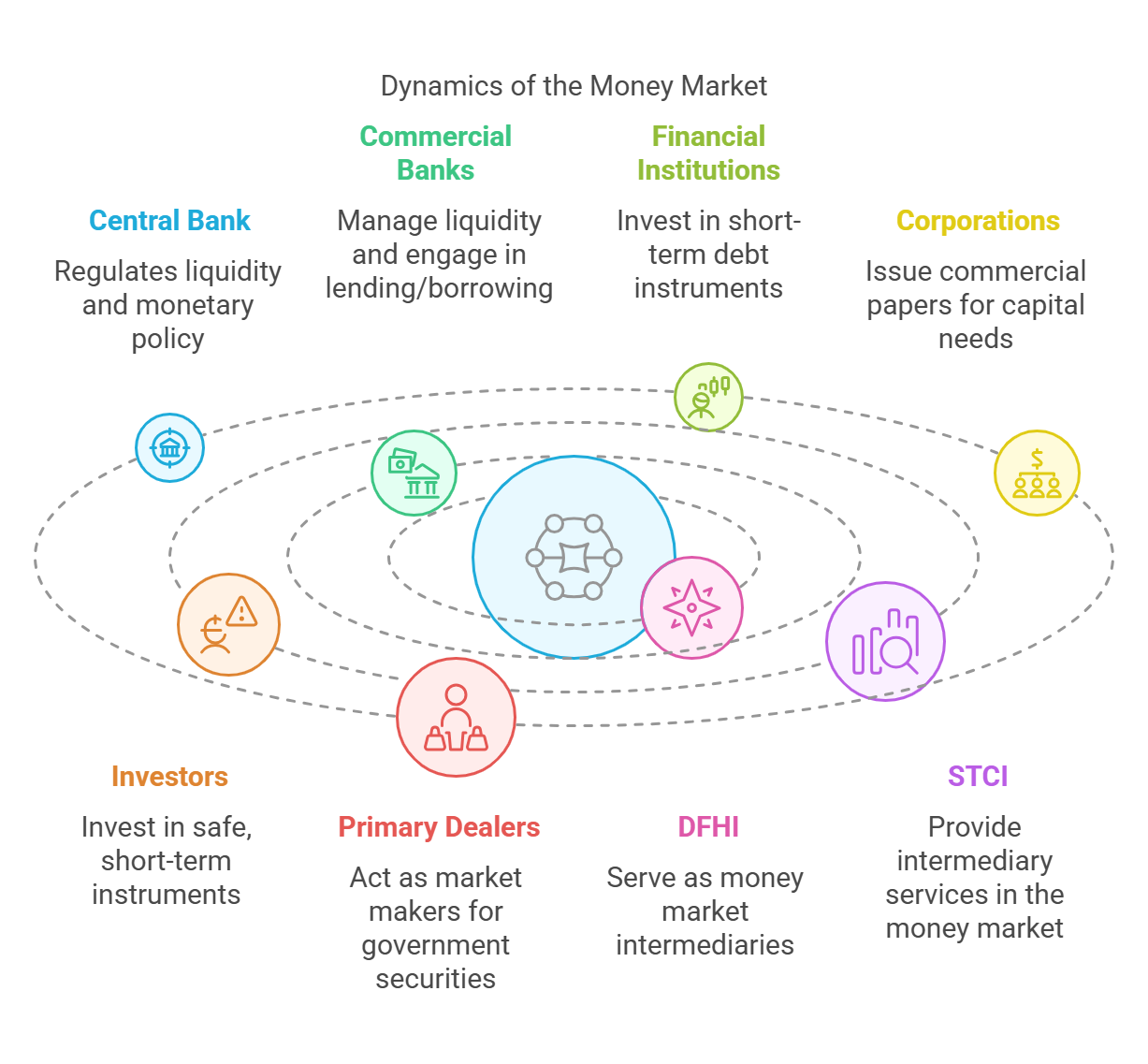

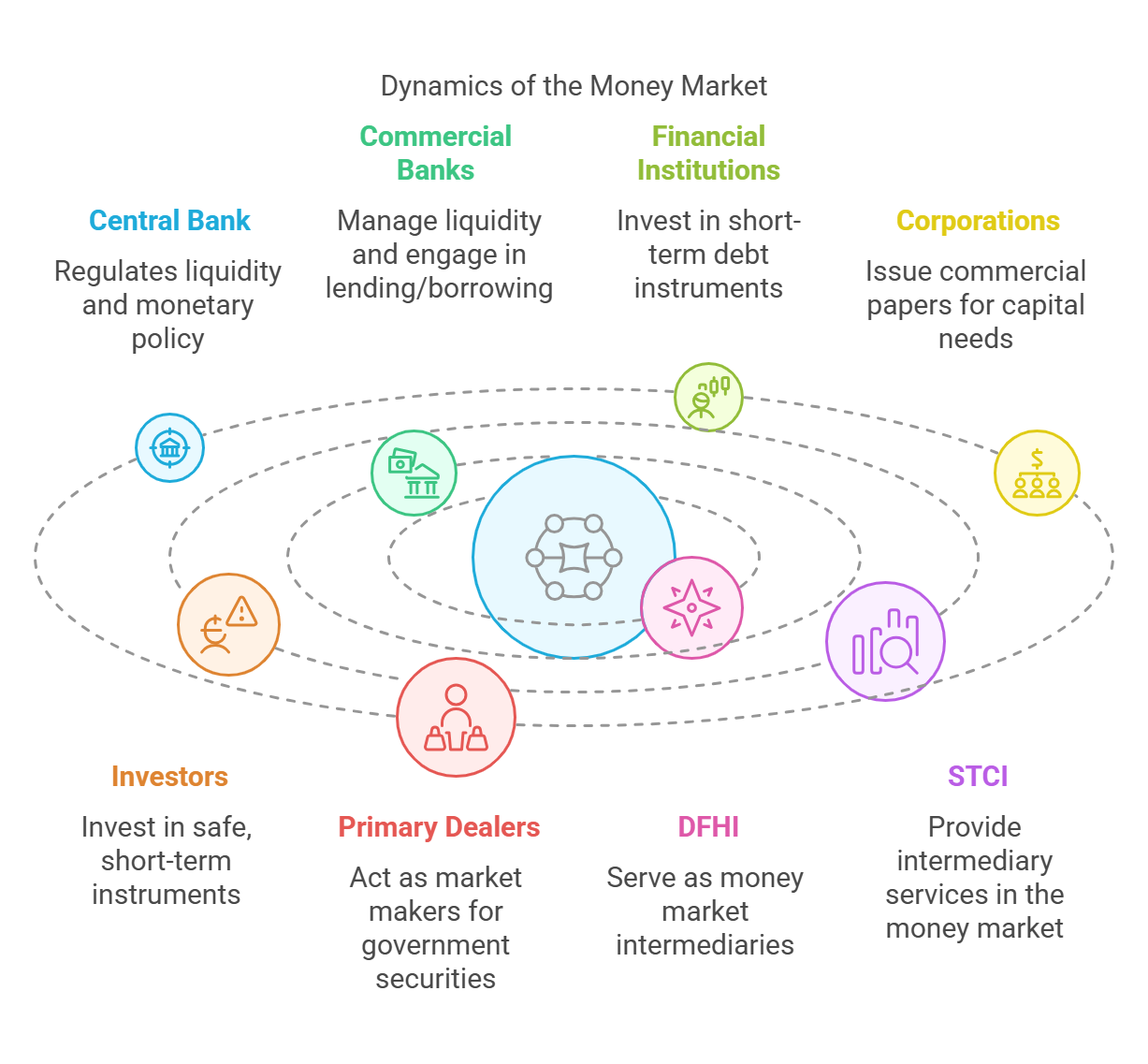

Participants in the Money Market:

The money market involves various participants, each playing a specific role:

- Central Bank (RBI): Regulates liquidity through monetary policy instruments like the repo rate, reverse repo rate, and cash reserve ratio (CRR).

- Commercial Banks: Actively manage short-term liquidity needs and excess funds through call money transactions, interbank lending/borrowing, and participation in T-bill and CD markets.

- Financial Institutions: Insurance companies, pension funds, mutual funds, and NBFCs participate by buying short-term debt instruments to manage surplus funds.

- Corporations: Issue commercial papers (CPs) to raise short-term capital for working capital requirements and invest in money market instruments for liquidity management.

- Investors: Retail and institutional investors participate by investing in instruments like T-bills, CDs, or CPs for safe, liquid, and short-term investment options.

- Primary Dealers: Market makers for government securities.

- Discount and Finance House of India (DFHI): Money market intermediaries.

- Securities Trading Corporation of India (STCI): Money market intermediaries.

- Public Sector Undertakings (PSUs): Manage their short term funds.

- Non-Resident Indians: Invest in money market instruments.

- State Governments: Manage their short term funds.

-

Provident Funds: Invest their short term funds.Dynamics of the

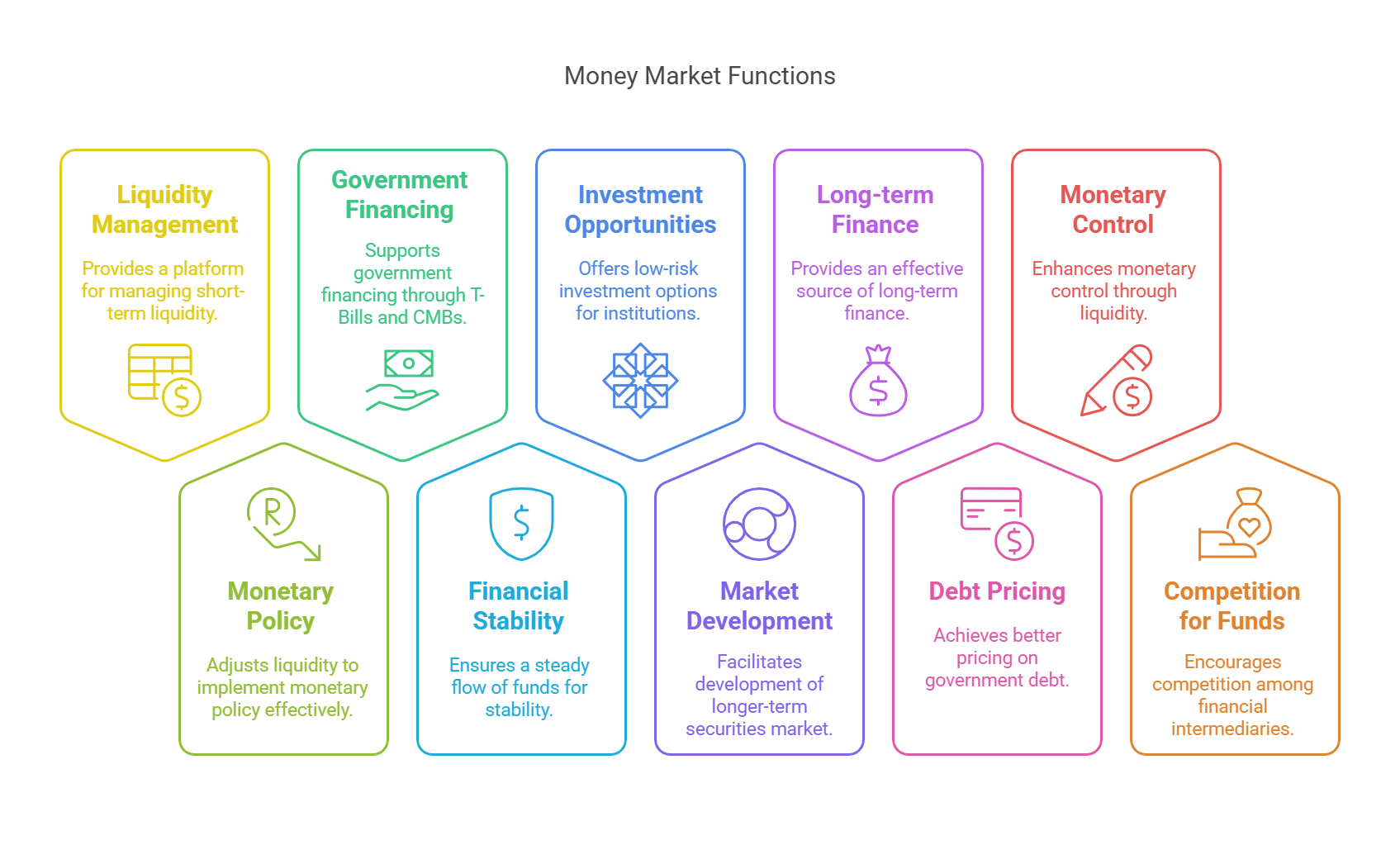

Importance of the Money Market in India:

- Liquidity Management: Provides a crucial platform for financial institutions and corporations to manage their short-term liquidity, ensuring sufficient liquidity in the system.

- Monetary Policy Implementation: Facilitates the RBI's implementation of monetary policy by adjusting liquidity in the banking system through tools like repo and reverse repo operations, helping control inflation and manage interest rates.

- Financing Government's Short-Term Needs: Supports government financing through Treasury Bills (T-Bills) and Cash Management Bills (CMBs).

- Support for Financial Stability: Promotes financial stability by ensuring a steady flow of funds within the banking and financial system, providing a safe haven for low-risk, short-term investments.

- Facilitating Investment Opportunities: Offers investment opportunities for institutional investors like mutual funds, insurance companies, and pension funds, benefiting from the liquidity and low-risk nature of money market instruments.

- Development of other markets: Facilitates the development of a market for longer-term securities. The interest rates for extremely short-term use of money serve as a benchmark for longer-term financial instruments.

- Source of long-term Finance: Provides an effective source of long-term finance to borrowers. Large borrowers can lower the cost of raising funds and manage short-term funding or surplus efficiently.

- Better pricing on debt: The government can achieve better pricing on its debt as it provides access to a wide range of buyers and facilitates the government market borrowing programme.

- Monetary control: Monetary control through indirect methods (repos and open market operations) is more effective if the money market is liquid.

- Competition for funds: It encourages the development of non-bank intermediaries thus increasing the competition for funds. Savers get a wide array of savings instruments to choose from and invest their savings.

Conclusion:

The money market is a vital component of the Indian financial system, playing a central role in managing short-term liquidity, supporting government borrowing, implementing monetary policy, and facilitating investment opportunities. Its stability and efficiency are crucial for the overall health of the financial system and the broader economy.

No Comments