Primary Market and Book building process

1. Instruments in the Primary Market

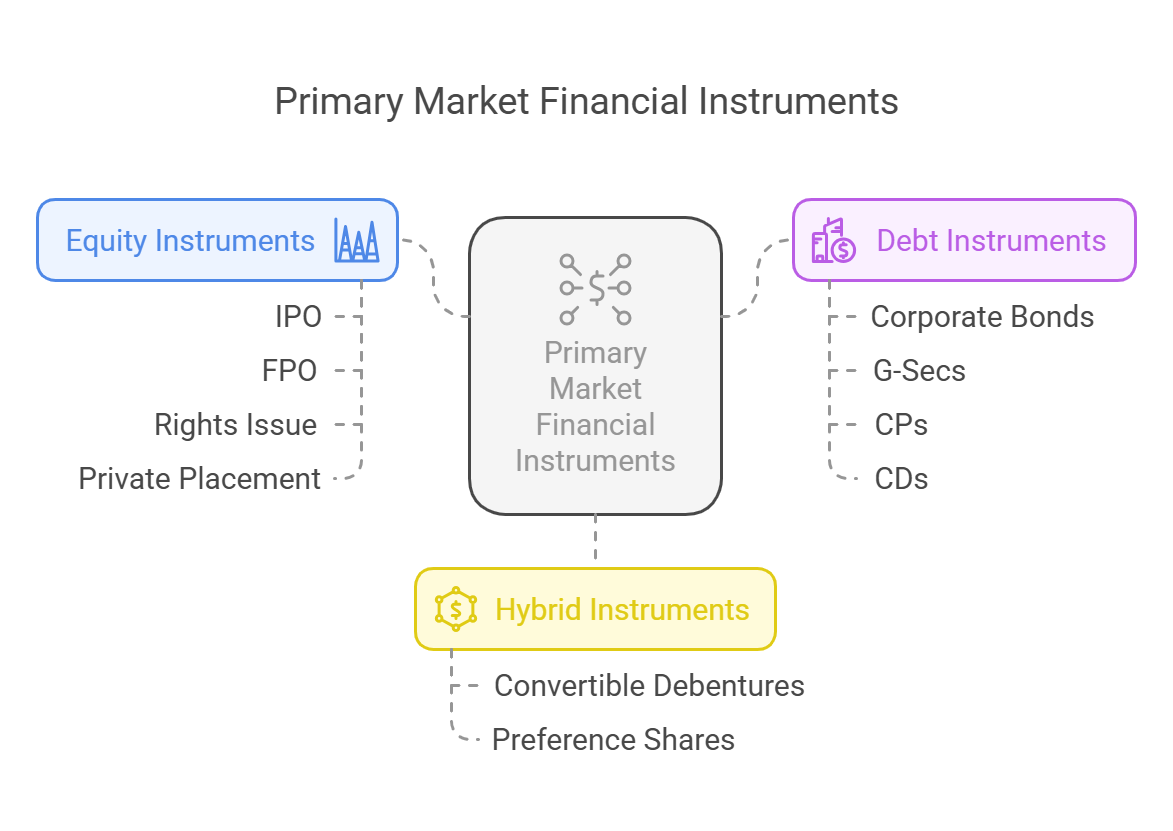

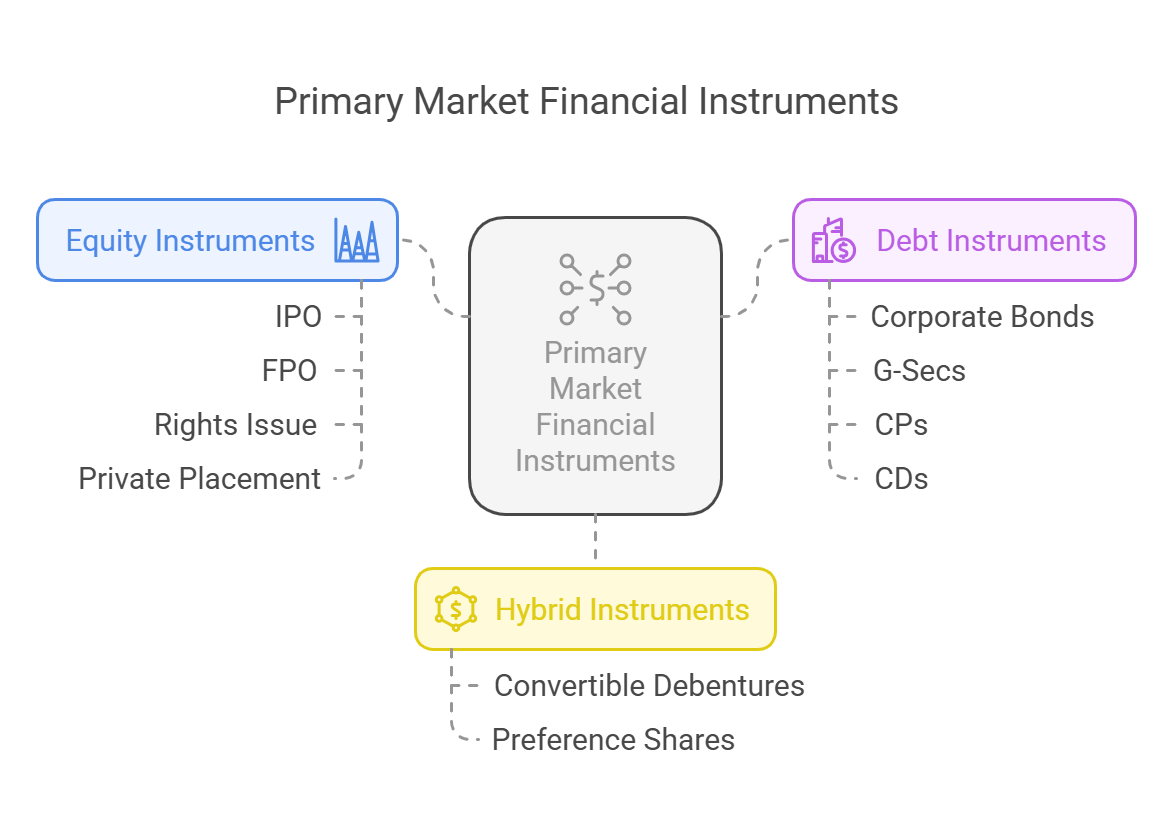

The primary market issues various financial instruments to raise capital. These can be broadly classified into equity, debt, and hybrid securities.

A. Equity Instruments

-

Initial Public Offering (IPO):

- Definition: The first time a company offers its shares to the public to raise capital.

- Outcome: Investors become shareholders and gain ownership in the company.

- Pricing: Can be through fixed-price or book-building methods.

-

Follow-on Public Offering (FPO):

- Definition: Additional shares issued by a company that is already publicly listed.

-

Rights Issue:

- Definition: Existing shareholders are offered additional shares at a discounted price, in proportion to their current holdings.

-

Private Placement:

- Definition: Securities are sold directly to institutional investors rather than the general public.

- Example: Qualified Institutional Placement (QIP) for raising funds from Foreign Institutional Investors (FIIs).

B. Debt Instruments

-

Corporate Bonds/Debentures:

- Definition: Companies issue bonds to raise long-term funds with fixed interest payments (coupon).

-

Government Securities (G-Secs):

- Definition: The government raises funds by issuing treasury bills, bonds, or sovereign gold bonds.

-

Commercial Papers (CPs):

- Definition: Short-term unsecured debt issued by corporations to meet working capital needs.

-

Certificate of Deposits (CDs):

- Definition: Time deposits issued by banks with a fixed maturity period.

C. Hybrid Instruments

-

Convertible Debentures:

- Definition: A mix of equity and debt, allowing conversion into equity shares at a later date.

-

Preference Shares:

-

Definition: Shareholders receive fixed dividends before common shareholders but have limited voting rights.

-

Definition: Shareholders receive fixed dividends before common shareholders but have limited voting rights.

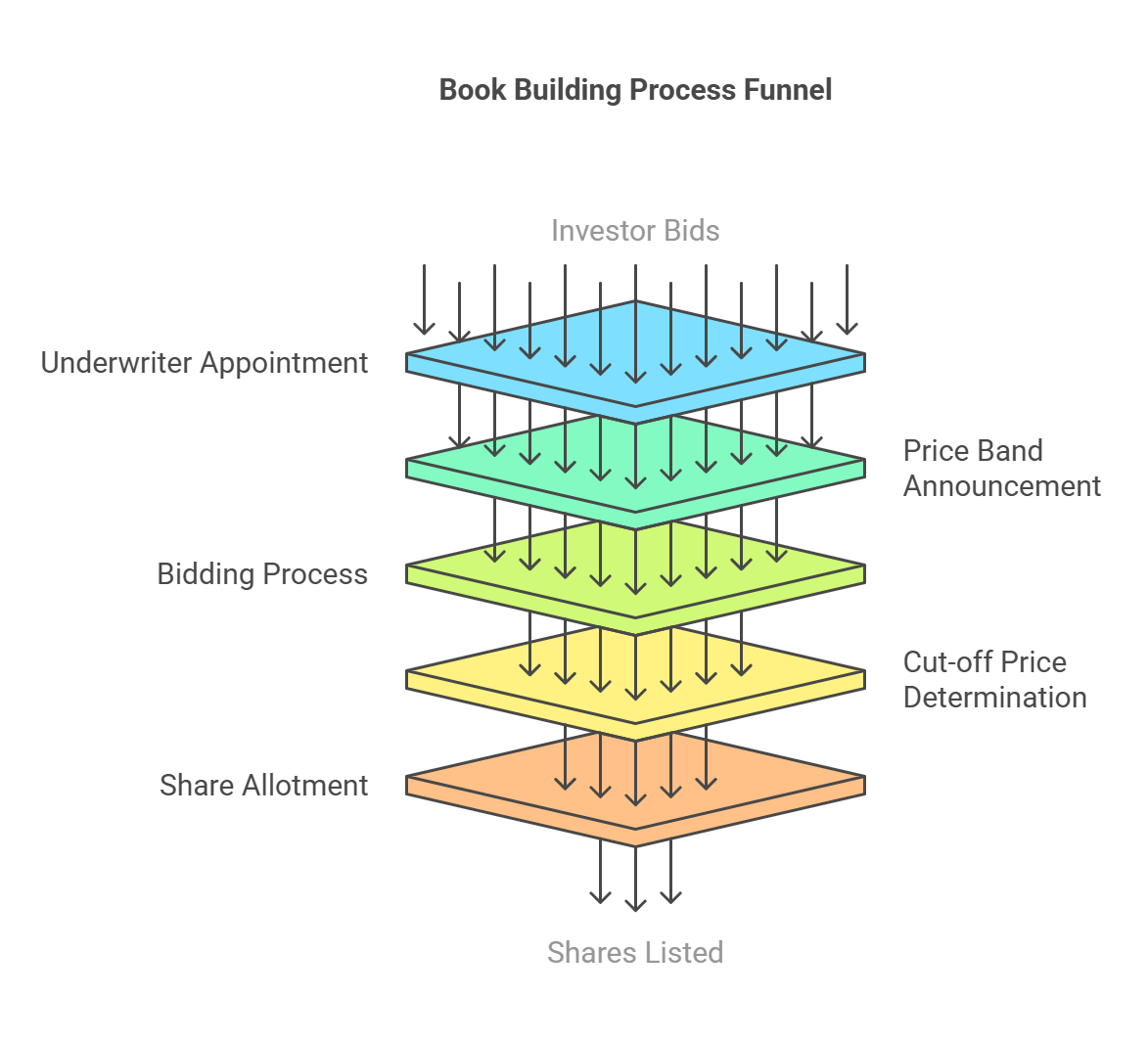

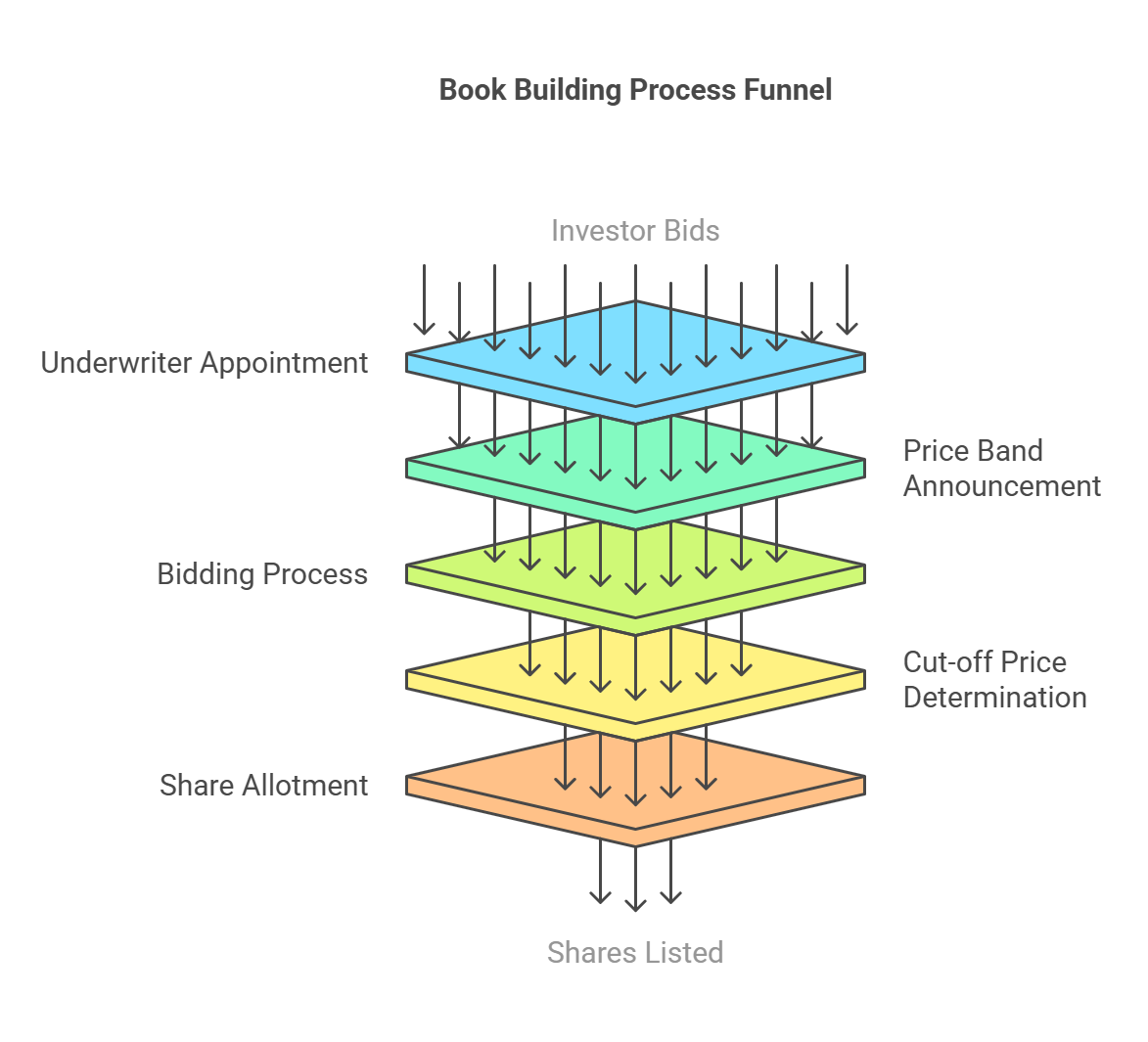

2. Book Building Process in the Primary Market

Book building is a price discovery mechanism used during an IPO or FPO, where investors bid for shares at different price levels within a specified range. The final issue price is determined based on demand.

Steps in the Book Building Process

-

Appointing Underwriters and Merchant Bankers:

- The company hires an investment bank to manage the issue.

- The lead manager files a Draft Red Herring Prospectus (DRHP) with SEBI.

-

Price Band Announcement:

- The issuer announces a floor price (minimum) and a cap price (maximum) for bids.

- Example: If a company sets a price band of ₹100-120, investors can bid within this range.

-

Bidding Process:

- Investors submit bids, mentioning the number of shares and the price they are willing to pay.

-

Determining the Cut-off Price:

- The cut-off price is decided based on demand (highest subscription level).

- Investors who bid below this price do not get shares.

-

Allotment of Shares:

- Shares are allotted to investors who bid at or above the cut-off price.

- The final price is determined based on the weighted average of successful bids.

-

Listing on Stock Exchange:

- After allotment, shares are listed on NSE/BSE for secondary market trading.

- After allotment, shares are listed on NSE/BSE for secondary market trading.

Advantages of the Book Building Process:

- Market-Driven Pricing: Prevents overpricing or underpricing of shares.

- Transparency: Demand-based price discovery ensures fairness.

- Efficient Allocation: Ensures shares go to those who value them the most.

- Better Investment Decision: Investors can assess demand before subscribing.

Conclusion

The primary market is crucial for capital formation in the economy, providing businesses with long-term financing. Book building has largely replaced fixed-price issues due to its efficient, transparent, and demand-driven pricing mechanism. It facilitates better price discovery and allocation of shares, benefiting both issuers and investors.

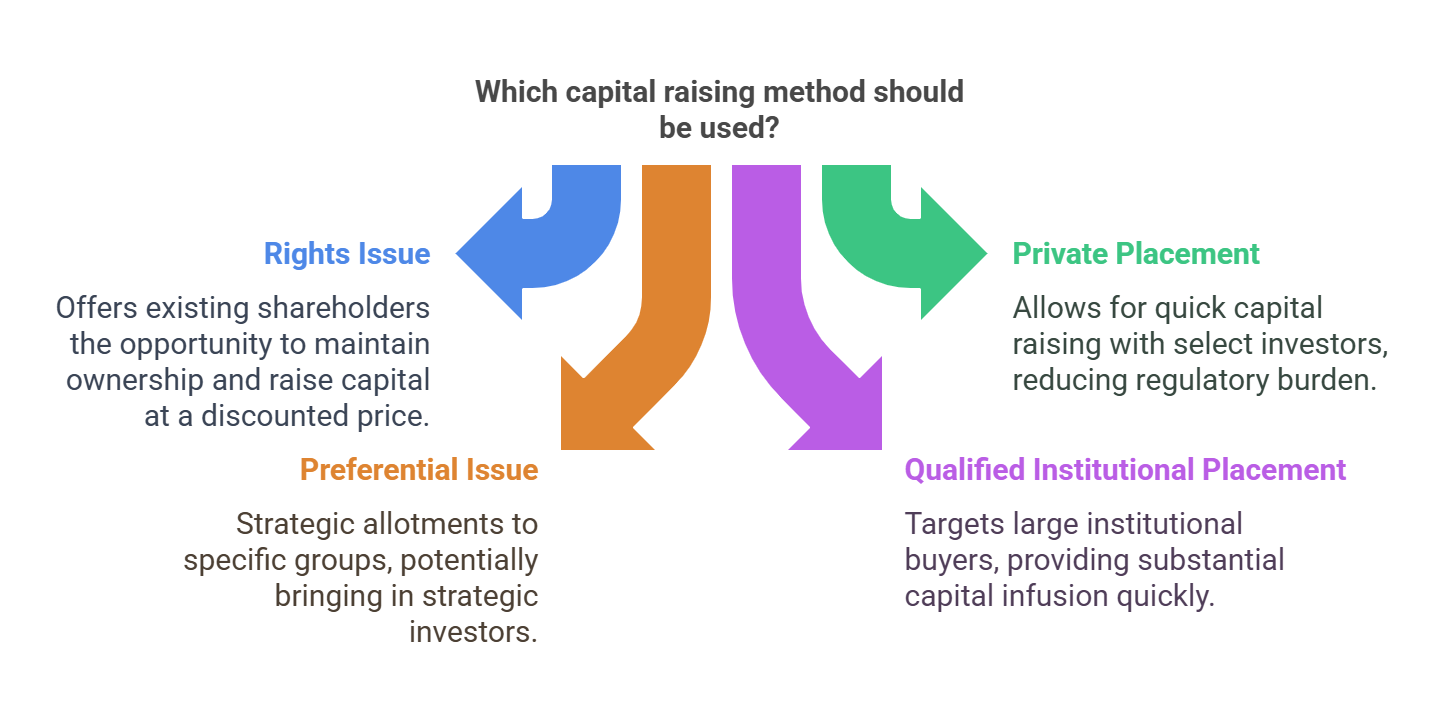

Alternative Capital Raising Methods: Rights Issue, Private Placement, Preferential Issue, and QIP

This document explores various alternative methods used by companies to raise capital in the primary market: Rights Issue, Private Placement, Preferential Issue, and Qualified Institutional Placement (QIP). It also clarifies the nature of Non-Government Public Limited Companies.

1. Rights Issue: Offering Opportunities to Existing Shareholders

A Rights Issue is a method by which a company raises additional capital by offering new shares to its existing shareholders in proportion to their current holdings. These shares are offered at a predetermined price and within a fixed subscription period.

-

Key Features:

- Discounted Price: Typically offered at a price lower than the prevailing market price, incentivizing shareholders to subscribe.

- No Dilution (If Subscribed): Existing shareholders who subscribe to the rights issue maintain their proportionate ownership in the company, preventing dilution of their stake.

- Tradable Rights: Shareholders have the option to accept, reject, or trade their rights entitlement (the right to purchase the new shares) in the market. This allows shareholders who do not wish to subscribe to still benefit from the issue by selling their rights to others.

-

Example:

- A company announces a 1:5 Rights Issue at ₹80 per share, while the market price is ₹100.

- An investor holding 500 shares is entitled to buy 100 additional shares (1 new share for every 5 shares held) at ₹80 each.

- The investor can choose to buy these 100 shares, sell their entitlement to another investor, or let the rights lapse.

-

Advantages:

- Less Regulatory Burden: Compared to a full-fledged public offering (IPO or FPO), a rights issue involves fewer regulatory requirements and compliance procedures.

- Existing Shareholder Priority: Gives existing shareholders the first opportunity to invest in the company's growth.

- Cheaper Capital: Can be a more cost-effective method of raising capital compared to public issues, as it avoids extensive marketing and underwriting fees.

-

Disadvantages:

- Risk of Undersubscription: If existing shareholders do not subscribe to the issue, the company may fail to raise the desired capital. This can happen if shareholders lack confidence in the company's prospects or if the discounted price is not attractive enough.

- Potential Stock Price Decline: The stock price may fall due to the increased supply of shares in the market (dilution effect), especially if the rights issue is not well-received by investors.

2. Private Placement Market: Targeting Select Investors

The Private Placement Market involves the direct sale of securities (shares, bonds, or debentures) by a company to a pre-selected group of investors, rather than offering them to the general public. These investors typically include institutions, high-net-worth individuals (HNIs), or mutual funds.

-

Types of Private Placement:

- Institutional Private Placement: Offered to large institutional investors, such as pension funds, insurance companies, or mutual funds.

- Retail Private Placement: Offered to wealthy individuals or accredited investors who meet specific income or net worth requirements.

-

Key Features:

- Faster Capital Raising: Significantly faster than conducting a public offering, as it avoids lengthy regulatory processes and marketing campaigns.

- Reduced Regulatory Burden: Less regulatory compliance and disclosure requirements compared to public offerings.

- Flexible Instruments: Can involve the issuance of equity, debt, or hybrid instruments, depending on the company's financing needs.

-

Advantages:

- Quick Fundraising: Allows companies to raise capital quickly when they need it most.

- Confidentiality: Financial details and strategic plans can be kept confidential, as the offering is not widely publicized.

- No Public Market Dilution: Avoids diluting ownership in the public markets.

-

Disadvantages:

- Limited Investor Base: Restricts the pool of potential investors, which may limit the amount of capital that can be raised.

- Higher Interest Rates (for Debt): For debt instruments, private placements may involve higher interest rates compared to public offerings to compensate investors for the reduced liquidity and higher risk.

3. Preferential Issue: Strategic Allotments to Specific Groups

A Preferential Issue is a method where a company allots shares or convertible securities to a specific group of investors at a pre-determined price. These investors can include promoters, strategic investors, institutional investors, or high-net-worth individuals.

-

Key Features:

- Fixed Price: Shares are issued at a fixed price, which may be at a premium or discount to the prevailing market price.

- SEBI Regulations: Subject to specific regulations by the Securities and Exchange Board of India (SEBI) to ensure fairness and transparency.

- Lock-in Period: Shares issued through a preferential allotment are typically subject to a lock-in period, during which the investors cannot sell their shares. The lock-in period is often longer for promoters (e.g., 3 years) compared to non-promoter investors (e.g., 1 year).

-

Example:

- A company issues 1 crore shares at ₹120 per share to select investors through a preferential allotment, when the market price is ₹130.

-

Advantages:

- Quick Capital: Helps the company raise capital relatively quickly compared to other methods.

- Strategic Investors: Can be used to bring in strategic investors who can provide expertise, access to new markets, or other valuable resources.

-

Disadvantages:

- Potential Dilution: Can dilute the ownership of existing shareholders if the shares are issued at a discount to the market price.

- Corporate Governance Concerns: If shares are issued at a significant discount, it may raise concerns about fairness and corporate governance practices.

4. Qualified Institutional Placement (QIP): Targeting Large Institutional Buyers

Qualified Institutional Placement (QIP) is a method by which a listed company raises capital from Qualified Institutional Buyers (QIBs) without going through lengthy regulatory processes. QIBs include mutual funds, insurance companies, pension funds, and foreign institutional investors who are registered with SEBI.

-

Key Features:

- Exclusive to QIBs: Shares are offered only to SEBI-registered Qualified Institutional Buyers (QIBs). Retail investors are not eligible to participate.

- Minimum QIB Participation: A minimum number of QIBs (typically 5) must participate in the issue to ensure broader participation.

- Reduced Foreign Capital Reliance: Aimed at reducing the Indian market's reliance on foreign capital by encouraging participation from domestic institutional investors.

-

Example:

- A company issues shares worth ₹500 crores to institutional investors through a QIP.

-

Advantages:

- Faster Process: Significantly faster than an IPO, with fewer regulatory requirements and lower transaction costs.

- Large Capital Infusion: Allows companies to raise substantial amounts of capital without extensive marketing efforts.

- No Minimum Pricing (Unlike Preferential Issues): More pricing flexibility compared to preferential issues, as there are no strict regulations on the issue price.

-

Disadvantages:

- Limited Investor Base: Only large institutional investors can participate, limiting the potential investor pool.

- May Not Suit All Companies: May not be suitable for smaller or mid-sized companies that may need to attract a broader base of investors.

Non-Government Public Limited Companies (Private Sector): Clarifying Ownership and Governance

A Non-Government Public Limited Company refers to a company that is:

-

Privately Owned: Not controlled by the government (i.e., the government does not hold a majority stake, typically 51% or more).

-

Publicly Listed: Its shares are publicly traded on stock exchanges, allowing anyone to buy and sell them.

-

Key Features:

- Publicly Traded Shares: Shares are traded on stock exchanges, providing liquidity and market-based valuation.

- Minimum Requirements: Must comply with requirements for public companies, such as having at least 7 shareholders and 3 directors.

- Regulatory Compliance: Subject to regulations set by SEBI and the Companies Act, ensuring transparency and investor protection.

- Capital Raising Options: Can raise capital through various methods, including IPOs, FPOs, Rights Issues, QIPs, and Private Placements.

-

Examples:

- Tata Consultancy Services (TCS)

- Reliance Industries Ltd. (RIL)

- Infosys Ltd.

-

Difference from Government-Owned Public Companies:

Feature Non-Government Public Company Government Public Company Ownership Private investors (majority ownership) Government (majority ownership, typically 51% or more) Control Managed by promoters, shareholders, and a board of directors Controlled by the government through appointed officials and policy directives Fundraising IPOs, FPOs, QIP, Private Placements Government budget allocations, disinvestment (selling government stake) Example Infosys, Reliance State Bank of India (SBI), Oil and Natural Gas Corporation (ONGC), NTPC Ltd.

Conclusion:

- Rights Issues and Preferential Issues are methods that prioritize existing shareholders or select investors when raising capital.

- Private Placements and QIPs offer companies quicker access to capital from a more targeted investor base with fewer regulatory hurdles.

- Non-Government Public Limited Companies represent the private sector while being publicly traded, distinguishing them from government-controlled entities.

- Understanding these alternative capital-raising methods is crucial for investors and businesses alike to make informed decisions about investing and raising capital.

No Comments