Retail Participation in Money and Debt Market

1. Introduction

Historically, the Indian government securities (G-Secs) and money market instruments have been primarily accessible to institutional investors such as banks, mutual funds, and insurance companies. However, in a move to broaden participation and promote financial inclusion, the Reserve Bank of India (RBI) launched the RBI Retail Direct platform in November 2021. This platform empowers individual investors (retail participants) to directly buy and sell government securities (G-Secs), Treasury Bills (T-Bills), and Sovereign Gold Bonds (SGBs), offering them a new avenue for safe and stable investments.

2. What is RBI Retail Direct?

The RBI Retail Direct Scheme is an initiative by the Reserve Bank of India to provide an online platform that allows retail investors to directly invest in government securities, bypassing intermediaries.

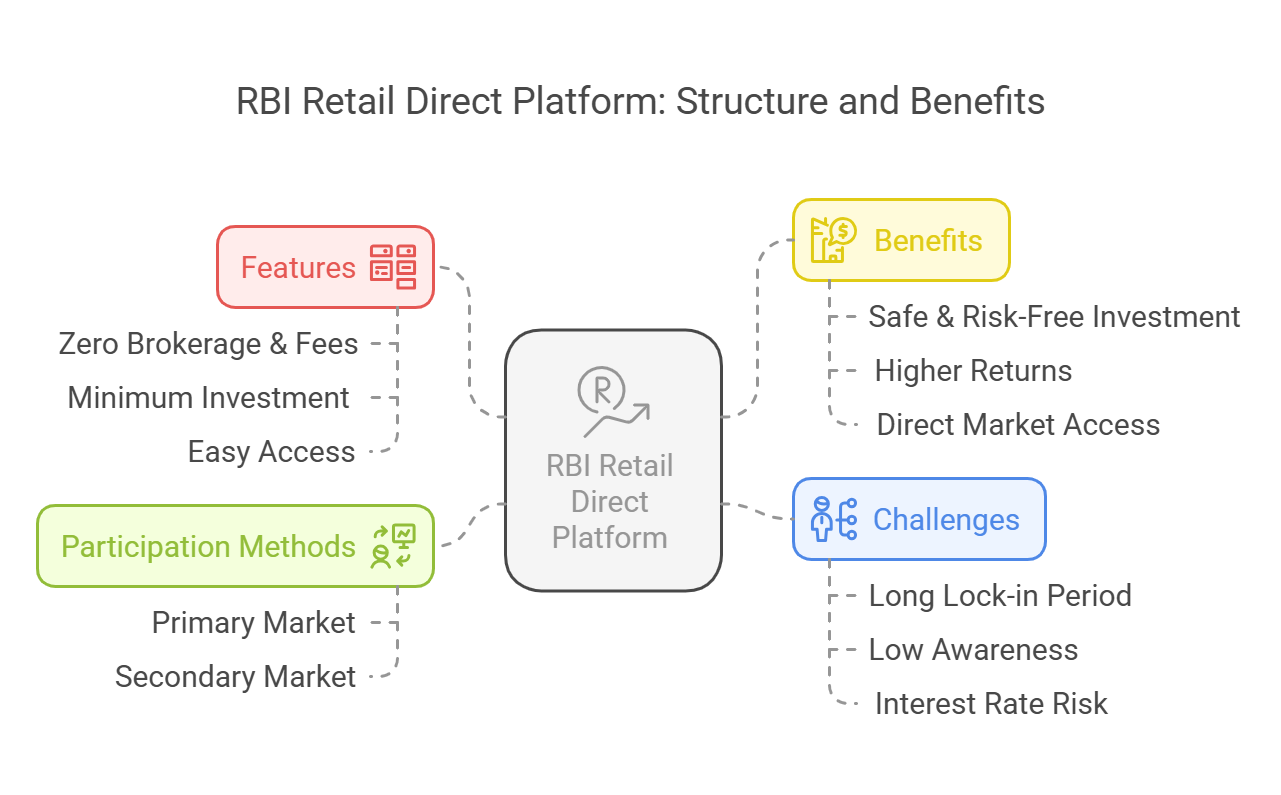

- Direct Access: Offers retail investors direct access to the primary and secondary markets for government securities.

- Simplified Investment: Simplifies the process of investing in G-Secs, T-Bills, SGBs, and State Development Loans (SDLs), making it more accessible to individual investors.

- Risk-Free & Stable: Provides a risk-free, stable investment option backed by the sovereign guarantee of the Government of India.

Features of RBI Retail Direct:

- Zero Brokerage & Fees: Investors can invest in government securities without paying any brokerage fees or intermediary charges.

- Minimum Investment: The minimum investment amount is relatively low, starting at ₹10,000 for G-Secs and T-Bills, making it affordable for small investors.

- Easy Access: Operated via a dedicated online portal (RBI Retail Direct Portal), allowing investors to manage their investments from anywhere with internet access.

- Demat-Free Holding: Bonds are stored in an RBI-maintained account (Retail Direct Gilt Account), eliminating the need for a separate Demat account.

- Interest & Maturity Payments: Interest payments and maturity proceeds are credited directly to the investor's linked bank account, ensuring convenience and transparency.

3. How Does It Work?

A. Primary Market Participation (New Bonds/T-Bills):

Retail investors can participate in the primary market by bidding for:

- Treasury Bills (T-Bills): Short-term government securities with maturities of 91 days, 182 days, and 364 days.

- Government Bonds (G-Secs): Long-term securities with maturities ranging from 5 to 40 years.

- Sovereign Gold Bonds (SGBs): Government securities denominated in gold, offering investors a safe and convenient way to invest in gold.

- State Development Loans (SDLs): Securities issued by state governments to finance their development projects.

Process:

- Registration: Register on the RBI Retail Direct Portal (https://rbiretaildirect.org.in) by providing KYC details and linking a bank account.

- Auction Participation: Participate in auctions conducted by the RBI for the issuance of new G-Secs and T-Bills. Retail investors can participate through the Non-Competitive Bidding (NCB) route.

- Security Allocation: If the bid is successful, the securities are allocated to the investor's Retail Direct Gilt (RDG) Account, which is maintained with the RBI.

B. Secondary Market Trading (NDS-OM Platform):

Retail investors can also trade G-Secs in the secondary market through the NDS-OM (Negotiated Dealing System - Order Matching) platform.

- NDS-OM Access: The RBI Retail Direct platform provides access to the NDS-OM, allowing retail investors to buy and sell existing G-Secs.

- Trading Process: Investors can place buy and sell orders on the NDS-OM platform, and trades are executed based on price and time priority.

4. Benefits of RBI Retail Direct for Retail Investors:

- Safe & Risk-Free Investment: Government-backed securities offer virtually zero default risk, providing a safe haven for investors.

- Higher Returns vs. Bank Deposits: G-Secs typically offer better interest rates compared to traditional fixed deposits, enhancing the potential for higher returns.

- Regular Interest Payments: Long-term G-Secs provide semi-annual interest payments, offering a regular income stream for investors.

- Direct Market Access: Eliminates the need for intermediaries such as banks or brokers, reducing costs and increasing transparency.

5. Challenges & Limitations:

- Long Lock-in Period: G-Secs often have long tenures (5-40 years), which can limit liquidity and make them less suitable for investors with short-term investment horizons.

- Low Awareness: Retail participation in the debt market is still relatively low in India, and many investors are unaware of the opportunities offered by the RBI Retail Direct platform.

- Interest Rate Risk: Bond prices are inversely related to interest rates, meaning that rising interest rates can lead to a decline in the value of G-Secs.

Conclusion:

The RBI Retail Direct platform represents a significant step towards democratizing access to the Indian debt market and promoting financial inclusion. By offering a direct, transparent, and risk-free investment option, it empowers retail investors to participate in the growth of the Indian economy and build diversified portfolios. While challenges remain in terms of awareness and liquidity, the platform has the potential to transform the landscape of retail investment in India.

No Comments