Structure of Indian Financial System: An overview of the Indian financial system

1. Introduction

The financial system is the lifeblood of any modern economy. It acts as a conduit, channeling funds from those who have surplus capital (savers) to those who need it for investment and consumption (borrowers). Without a well-functioning financial system, economic growth would be severely hampered. Here's a breakdown of its crucial role:

- Efficient Resource Allocation: By connecting savers and borrowers, the financial system ensures that capital is directed towards its most productive uses. This maximizes economic output and fosters innovation.

- Investment Facilitation: It allows businesses to access the funds needed for expansion, research and development, and other crucial investments.

- Interest Rate Determination: The forces of supply and demand within the financial system determine interest rates, which act as a key signal for investment decisions.

- Risk Management: The financial system provides tools and mechanisms for managing various types of financial risks, such as credit risk, market risk, and liquidity risk.

-

Economic Stability: A stable financial system is essential for overall economic stability. Crises within the financial system can have devastating consequences for the entire economy.

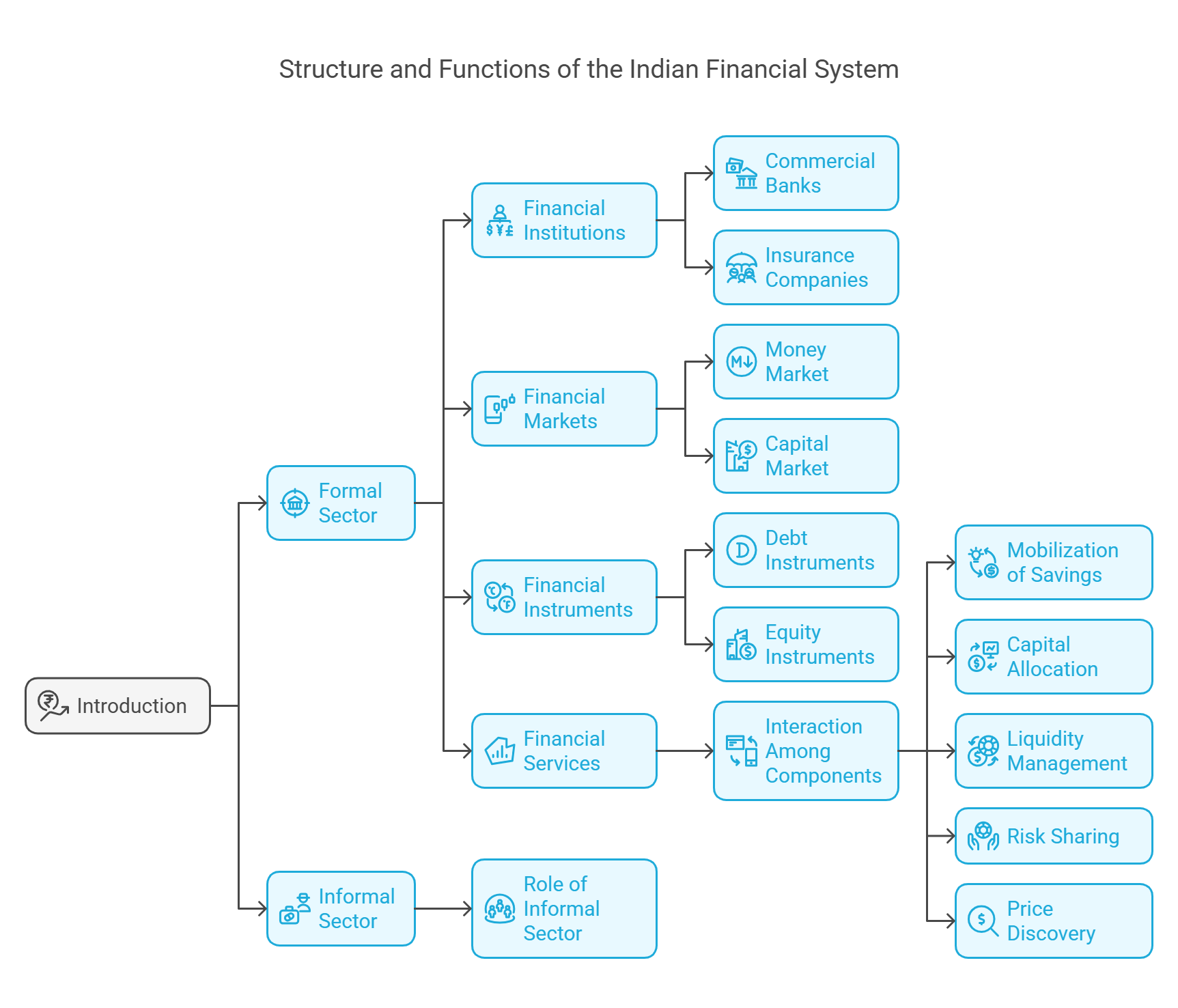

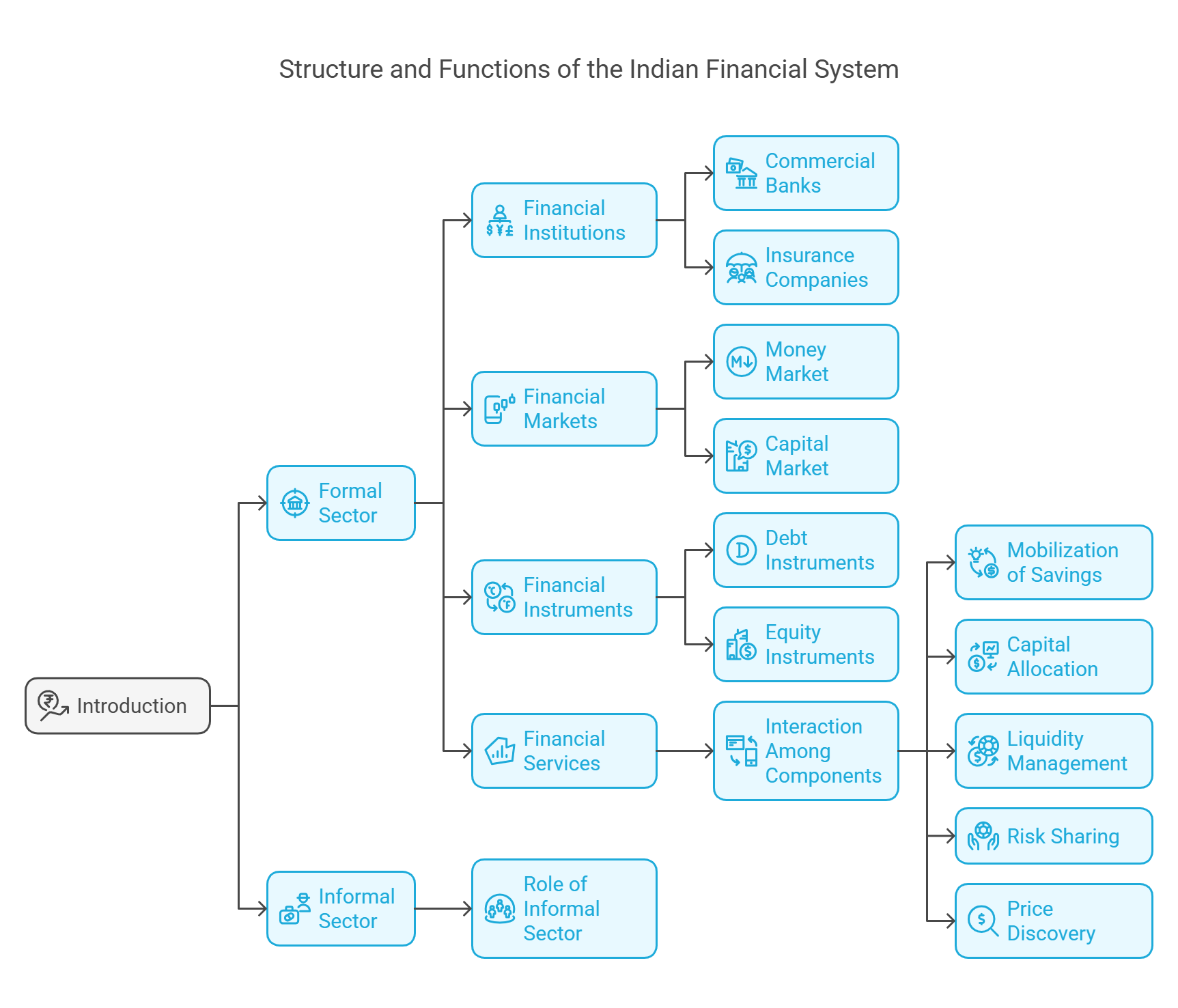

2. Formal and Informal Financial Sectors

The financial system can be broadly divided into two sectors: formal and informal.

Formal Financial Sector:

- Definition: This sector is characterized by regulated institutions and markets that adhere to established rules and regulations. It is overseen by regulatory bodies like the Reserve Bank of India (RBI), the Securities and Exchange Board of India (SEBI), and other relevant authorities.

-

Key Players:

- Commercial Banks: These are the most common type of financial institution, offering a wide range of services including accepting deposits, providing loans, and facilitating payment systems. (e.g., State Bank of India, HDFC Bank).

- Non-Banking Financial Companies (NBFCs): These institutions provide financial services similar to banks but are not allowed to accept demand deposits. They specialize in areas like lending, leasing, and hire purchase. (e.g., Bajaj Finance, Mahindra Finance).

- Insurance Companies: These companies provide insurance products to protect individuals and businesses against various risks. (e.g., LIC, ICICI Prudential Life Insurance).

- Stock Markets: These markets provide a platform for trading stocks and other securities. (e.g., National Stock Exchange (NSE), Bombay Stock Exchange (BSE)).

-

Advantages:

- Transparency: Formal institutions are subject to regulatory scrutiny, promoting transparency and accountability.

- Stability: Regulations and oversight help to maintain the stability and soundness of the formal sector.

- Access to a Wider Range of Services: The formal sector offers a diverse array of financial products and services.

- Legal Protection: Customers have legal recourse if disputes arise with formal institutions.

Informal Financial Sector:

- Definition: This sector consists of unregulated entities and activities that operate outside the formal financial system.

-

Key Players:

- Moneylenders: Individuals who lend money, often at high interest rates.

- Chit Funds: Rotating savings and credit associations.

- Hawala Operators: Informal money transfer systems.

-

Characteristics:

- Lack of Regulation: The informal sector is not subject to the same regulations as the formal sector.

- Limited Transparency: Transactions in the informal sector are often conducted without proper documentation.

- High Interest Rates: Moneylenders often charge exorbitant interest rates.

- Risk of Default: Borrowers in the informal sector are more vulnerable to default.

- Role: While often criticized, the informal sector plays a significant role in providing financial services to underserved populations, particularly in rural areas, where access to formal financial institutions may be limited.

-

Disadvantages:

- High Risk: Lack of regulation makes it riskier for both borrowers and lenders.

- Exploitation: Moneylenders may exploit borrowers due to the lack of regulation.

- Limited Services: The range of services offered is significantly smaller than the formal sector.

3. The Indian Financial System

The Indian financial system is a complex and dynamic system that has evolved significantly over the years. It's characterized by:

- Constituent Elements: It encompasses institutions, markets, instruments, and services that work together to facilitate the mobilization of savings, the investment of funds, and the efficient allocation of capital across the economy.

- Segmentation: The system is segmented into various components, each with distinct but interconnected functions, contributing to the overall economic growth and stability of the nation. This segmentation allows for specialization and efficiency within the system.

- Growth and Evolution: The Indian financial system has undergone substantial reforms and modernization in recent decades, including deregulation, privatization, and the adoption of new technologies. These changes have made the system more efficient and resilient.

4. Components of the Formal Financial System

This section delves into the key components of the formal financial system.

Financial Institutions

These are the core intermediaries that connect savers and borrowers.

-

Commercial Banks: The most important type of financial institution.

- Functions: Accepting deposits, providing loans, facilitating payment systems, and offering other financial services.

- Types: Public Sector Banks (e.g., SBI, Bank of Baroda), Private Sector Banks (e.g., HDFC Bank, ICICI Bank), Foreign Banks (e.g., Citibank, HSBC).

-

Development Banks: Specialized institutions that provide long-term financing to specific sectors of the economy.

- SIDBI (Small Industries Development Bank of India): Focuses on financing and promoting small-scale industries.

- NABARD (National Bank for Agriculture and Rural Development): Focuses on promoting agriculture and rural development.

-

Non-Banking Financial Companies (NBFCs): Provide financial services similar to banks but are not allowed to accept demand deposits.

- Functions: Leasing, hire purchase, microfinance, and investment services.

- Example: Muthoot Finance, Shriram Transport Finance.

-

Insurance Companies: Protect individuals and businesses against various risks.

- Types: Life Insurance (e.g., LIC), General Insurance (e.g., New India Assurance).

-

Pension Funds: Manage retirement funds for individuals.

- Example: Pension Fund Regulatory and Development Authority (PFRDA).

Financial Markets

Platforms where buyers and sellers trade financial instruments.

-

Money Market: Deals with short-term debt instruments (maturity of less than one year).

- Instruments: Treasury Bills (T-Bills), Certificates of Deposit (CDs), Commercial Paper (CP), Call Money.

- Purpose: Meeting short-term liquidity needs of businesses and governments.

-

Capital Market: Facilitates long-term financing through the issuance and trading of stocks and bonds (maturity of more than one year).

- Instruments: Stocks (equity), Bonds (debt), Debentures.

- Purpose: Raising capital for long-term investments.

-

Foreign Exchange Market (Forex Market): Where currencies are traded.

- Purpose: Facilitating international trade and investment. Determining exchange rates.

-

Derivatives Market: Where financial contracts whose value is derived from an underlying asset are traded.

- Instruments: Futures, Options, Swaps.

- Purpose: Hedging risks, speculation.

Financial Instruments

Contracts that represent a claim to future cash flows.

-

Debt Instruments: Represent a loan made by an investor to a borrower.

- Examples: Bonds, Debentures, Treasury Bills.

-

Equity Instruments: Represent ownership in a company.

- Examples: Shares (stocks).

-

Derivatives: Financial contracts whose value depends on the price of an underlying asset.

- Examples: Futures, Options, Swaps. The underlying asset could be a stock, bond, commodity, or currency.

Financial Services

Support financial activities and facilitate the smooth functioning of the system.

- Banking Services: Accepting deposits, providing loans, and facilitating payment systems.

- Investment Services: Mutual funds, portfolio management, wealth advisory, stock brokerage.

- Insurance Services: Providing risk management products, such as life insurance and health insurance.

- Pension Services: Managing and providing retirement funds.

5. Interaction Among Financial System Components

The various components of the financial system are not isolated; they are intricately linked and interact in several ways:

- Institutions and Markets: Financial institutions often participate in financial markets by issuing stocks and bonds to raise capital or by investing in securities. For example, a bank might issue bonds to raise funds for lending.

- Markets and Price Discovery: Financial markets play a critical role in price discovery, ensuring that financial assets are priced efficiently based on supply and demand. This allows resources to be allocated to their most productive uses.

- Instruments and Risk Management: Financial instruments, particularly derivatives, are used to manage risk and finance activities. For instance, a company might use futures contracts to hedge against fluctuations in commodity prices.

- Services and Access: Financial services help consumers and businesses access financial products, manage their wealth, and protect against risks. A financial advisor, for instance, can help an individual choose the right investment options.

6. Functions of a Financial System

A well-functioning financial system performs several essential functions:

- Mobilization of Savings: Collecting savings from households and institutions and channeling them into productive investments. This increases the availability of capital for businesses and economic growth.

- Capital Allocation: Efficiently directing funds to the most promising investment opportunities. This ensures that resources are used where they will generate the highest returns.

- Liquidity Management: Ensuring that assets can be converted into cash quickly and easily with minimal loss of value. This promotes stability and confidence in the system.

- Risk Sharing: Facilitating the management of risks through financial instruments such as insurance and derivatives. This allows businesses and individuals to transfer risk to those who are willing to bear it.

- Price Discovery: The process of determining the price of financial assets based on market demand and supply dynamics. This provides valuable information to investors and businesses.

7. Key Elements of a Well-Functioning Financial System

A healthy financial system requires the following key elements:

- Efficient Markets: Markets that are transparent, liquid, and characterized by competitive pricing. This ensures that resources are allocated efficiently and that investors receive fair prices.

- Robust Institutions: Sound and well-regulated financial institutions capable of managing risks and providing services effectively. This is essential for maintaining stability and confidence in the system.

- Effective Regulation and Supervision: Strong regulatory bodies (like the RBI and SEBI) to ensure market integrity, protect investors, and prevent financial crises.

- Availability of Financial Products: A diverse range of financial products to meet the diverse needs of individuals and businesses. This includes products for saving, investing, borrowing, and managing risk.

- Investor Confidence: A system that instills trust among investors, enabling the growth of financial markets and institutions. Without investor confidence, the financial system will struggle to function effectively.

India's financial system has evolved towards a more advanced design over the past few decades, reflecting the country's economic growth and increasing sophistication.

No Comments