Segments of money market- Call money market

Segments of the Money Market & Call Money Market: An In-Depth Look

This document provides a detailed exploration of the various segments within the Indian money market and a closer examination of the Call Money Market, a critical component for short-term liquidity management.

1. Segments of the Money Market

The Indian money market is composed of several distinct segments, each catering to specific participants and addressing unique short-term funding needs:

A. Call Money Market:

- Definition: The Call Money Market is an interbank lending market where commercial banks, cooperative banks, and primary dealers (PDs) borrow and lend funds for very short durations.

- Maturity: Loans in the call money market typically range from overnight (1 day) to a maximum of 14 days.

-

Participants:

- Borrowers: Commercial banks, cooperative banks, and primary dealers that need to cover short-term liquidity shortfalls or meet regulatory reserve requirements.

- Lenders: Commercial banks, insurance companies, and mutual funds that have surplus funds available for short-term lending.

- Interest Rate: The interest rate charged on these overnight loans is known as the Call Rate, which is highly sensitive to changes in the supply and demand for funds in the banking system.

B. Treasury Bill Market:

- Definition: Treasury Bills (T-Bills) are short-term debt instruments issued by the Government of India to raise funds for its short-term financing needs.

- Maturity: T-Bills are typically issued with maturities of 91 days, 182 days, or 364 days.

- Issuance: T-Bills are issued at a discount to their face value and are redeemed at par upon maturity.

- Risk and Liquidity: T-Bills are considered virtually risk-free due to the government's backing and are highly liquid, making them attractive to investors seeking safe and short-term investment options.

C. Commercial Paper (CP) Market:

- Definition: Commercial Papers (CPs) are unsecured, short-term promissory notes issued by corporations, non-banking financial companies (NBFCs), and other entities to raise funds for their working capital requirements.

- Maturity: CPs typically have maturities ranging from 7 days to 1 year.

- Issuance: CPs are issued at a discount to their face value and are rated by credit rating agencies to assess the creditworthiness of the issuer.

- Credit Rating: The interest rate on CPs reflects the issuer's credit rating, with higher-rated CPs commanding lower interest rates.

D. Certificate of Deposit (CD) Market:

- Definition: Certificates of Deposit (CDs) are negotiable, interest-bearing instruments issued by banks and financial institutions to raise short-term funds from the market.

-

Maturity:

- CDs issued by banks typically have maturities ranging from 7 days to 1 year.

- CDs issued by financial institutions can have maturities ranging from 1 year to 3 years.

- Interest Rates: CDs generally offer higher interest rates compared to savings deposits, making them an attractive option for investors seeking short-term returns.

E. Repo (Repurchase) Market:

- Definition: The Repo (Repurchase Agreement) market involves the short-term borrowing of funds by selling securities with an agreement to repurchase them at a higher price on a specified future date.

- Participants: Used by banks, the RBI, and other financial institutions to manage liquidity and access short-term funding.

- Repo Rate: The interest rate at which the RBI lends funds to banks through repo transactions is known as the Repo Rate.

- Reverse Repo Rate: The interest rate at which the RBI borrows funds from banks through reverse repo transactions is known as the Reverse Repo Rate.

F. Inter-Corporate Deposits (ICDs):

- Definition: Inter-Corporate Deposits (ICDs) are unsecured, short-term loans made between companies.

- Maturity: ICDs typically have maturities ranging from 7 days to 6 months.

- Purpose: Used by corporations to meet temporary liquidity needs and bridge short-term funding gaps.

2. Call Money Market

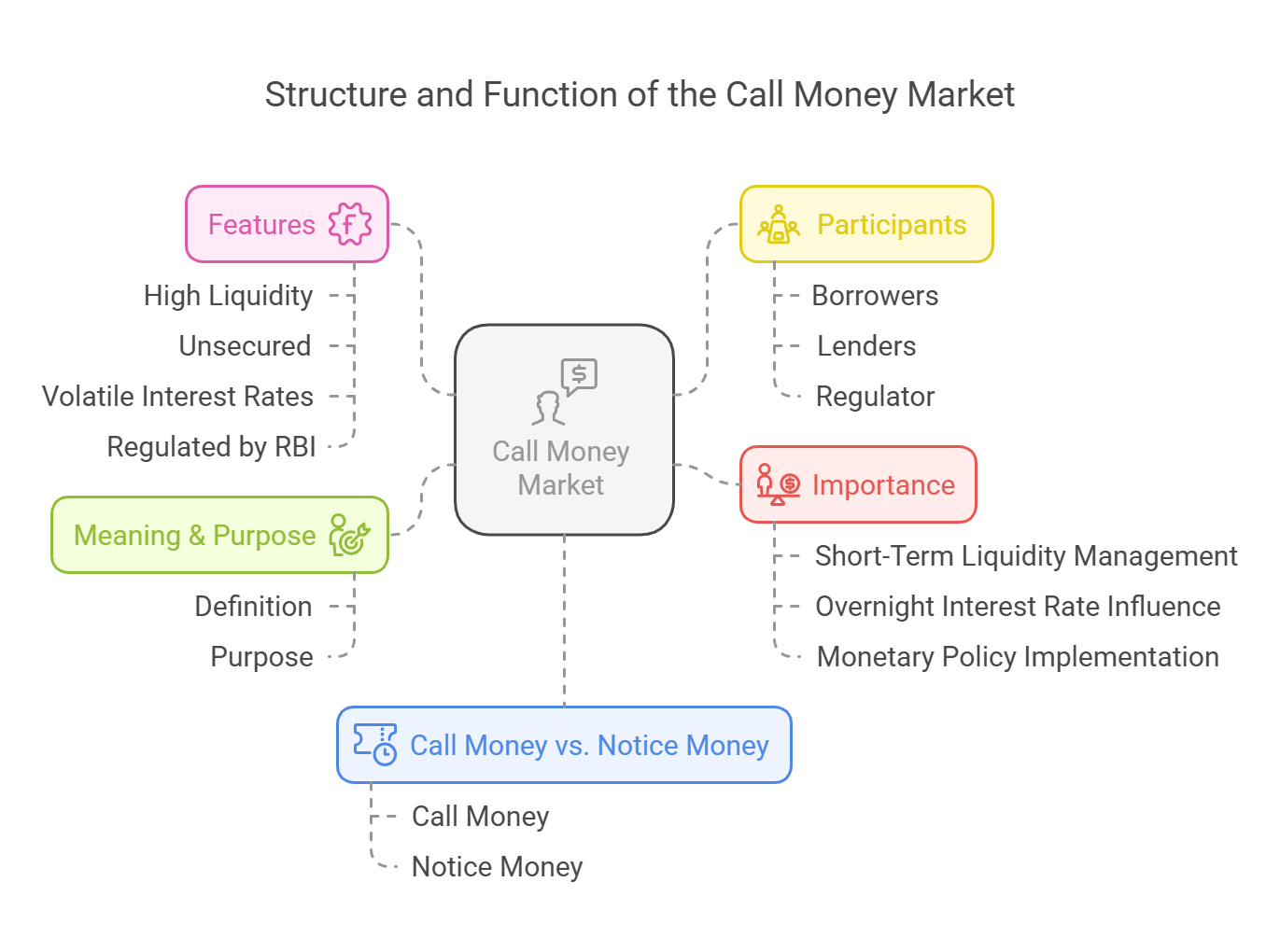

A. Meaning & Purpose:

-

Definition: The Call Money Market is a critical segment of the money market where banks and financial institutions borrow and lend funds for very short durations, primarily on an overnight basis.

-

Purpose:

- Helps banks manage their day-to-day liquidity positions and meet regulatory reserve requirements.

- Provides a mechanism for adjusting short-term cash balances and responding to unexpected inflows or outflows of funds.

B. Features of the Call Money Market:

- High Liquidity: Funds are borrowed and lent for extremely short periods, ensuring quick access to liquidity.

- Unsecured: Transactions are typically unsecured, meaning that no collateral is required to secure the loan.

- Volatile Interest Rates: The call rate fluctuates daily based on the supply and demand for funds in the banking system, reflecting the overall liquidity conditions in the market.

- Regulated by RBI: The Reserve Bank of India (RBI) closely monitors and regulates call money market operations to ensure stability and prevent excessive volatility.

C. Participants in the Call Money Market:

- Borrowers: Commercial Banks, Cooperative Banks, and Primary Dealers who need to cover short-term funding deficits.

- Lenders: Commercial Banks, Insurance Companies, and Mutual Funds that have surplus funds available for short-term lending.

- Regulator: The RBI plays a supervisory role, monitoring transactions and intervening to maintain stability.

D. Call Money vs. Notice Money:

| Type | Maturity Period |

|---|---|

| Call Money | Overnight (1 day) |

| Notice Money | 2 to 14 days |

E. Importance of the Call Money Market:

- Short-Term Liquidity Management: Helps banks efficiently manage their short-term liquidity needs and meet regulatory requirements.

- Overnight Interest Rate Influence: Influences the overnight interest rates in the economy, serving as a benchmark for other short-term interest rates.

- Monetary Policy Implementation: Used by the RBI to transmit monetary policy signals and influence the overall level of liquidity in the banking system.

Conclusion:

The money market is a dynamic and multifaceted component of the Indian financial system, consisting of various segments each with its own characteristics and functions. The Call Money Market is a vital segment for short-term liquidity management, facilitating overnight borrowing and lending between banks and influencing the overall interest rate environment.

No Comments