Universal Banking and Core Banking Solution (CBS)

This document delves into two essential concepts in modern banking: Universal Banking and Core Banking Solution (CBS). Understanding these concepts is crucial for grasping the evolution of the financial services landscape and the ways in which banks strive to meet the diverse needs of their customers in an efficient and secure manner.

Universal Banking: A One-Stop Shop for Financial Needs

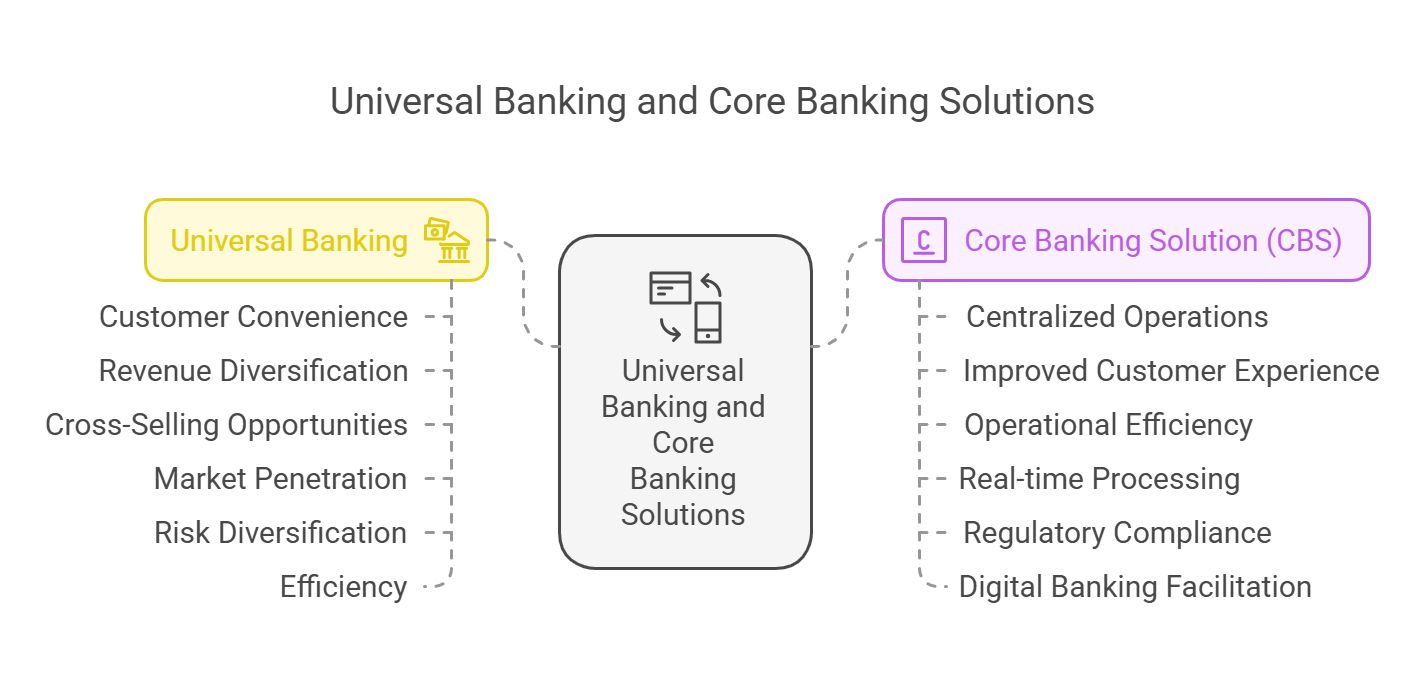

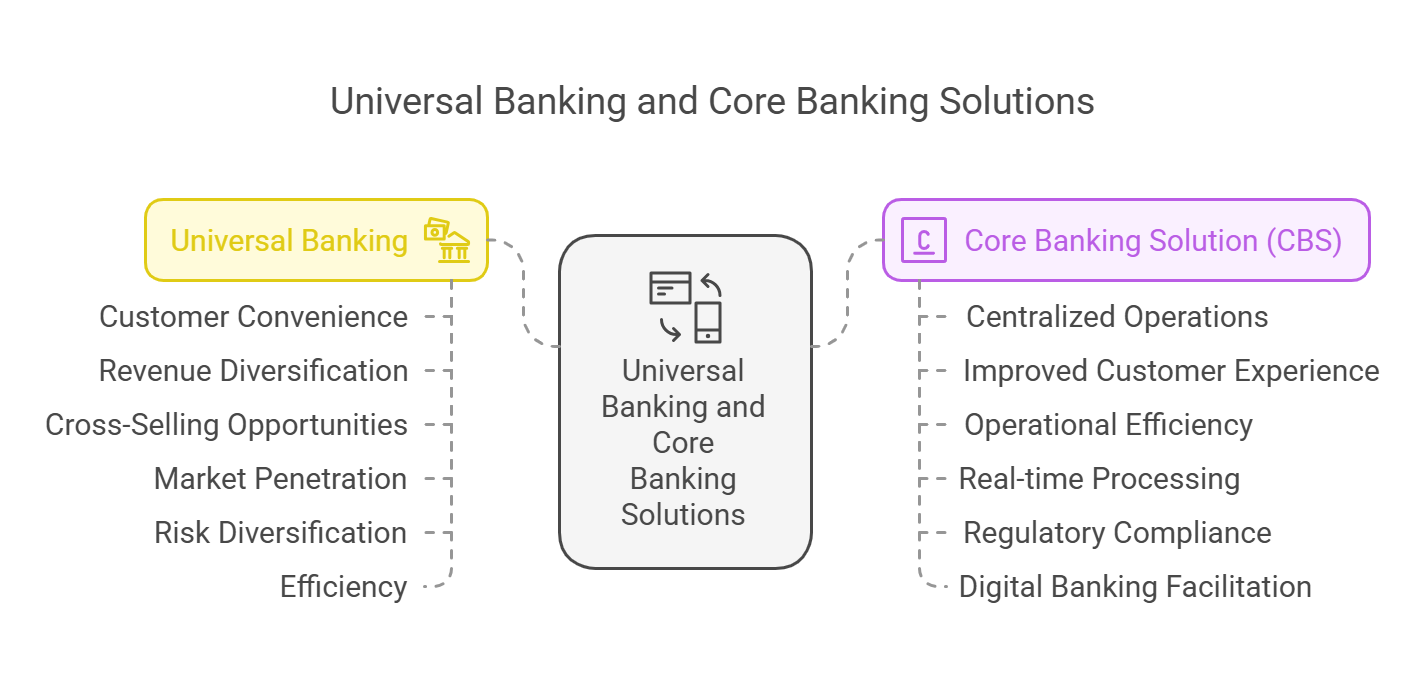

Universal Banking signifies a model where a single financial institution offers a broad spectrum of financial services, blurring the lines between traditional commercial banking activities and investment banking, insurance, and asset management. The goal is to provide customers with a "one-stop shop" for all their financial requirements.

-

Need for Universal Banking:

-

Customer Convenience and Satisfaction:

- Customers increasingly prefer the convenience of managing all their financial affairs under one roof. Universal banks eliminate the need to interact with multiple institutions for different services, streamlining the financial experience and saving time and effort.

- This integrated approach fosters stronger customer relationships, as the bank gains a deeper understanding of the customer's overall financial situation and can offer more personalized advice and solutions.

-

Increased Revenue Streams:

- Universal banks diversify their revenue base by offering a wide array of products and services. This diversification reduces their reliance on traditional lending activities and makes them more resilient to economic downturns that might negatively impact specific sectors.

- Revenue sources can include:

- Interest Income: From loans and other lending products.

- Fees: From advisory services, investment banking activities, and wealth management.

- Commissions: From selling insurance policies and other financial products.

- Trading Profits: From trading securities and other financial instruments.

-

Cross-Selling Opportunities:

- Universal banks can effectively leverage their customer base by cross-selling products and services. This involves offering additional products or services to existing customers based on their individual needs and financial profiles.

- Examples include:

- Offering insurance policies to customers with savings accounts or mortgages.

- Providing investment banking services to corporate clients with existing loan relationships.

- Promoting wealth management services to high-net-worth individuals with deposit accounts.

-

Market Penetration and Customer Retention:

- The comprehensive range of services offered by universal banks attracts a wider customer base, including both retail and corporate clients.

- Customers are more likely to remain loyal to a bank that can meet all their financial needs, leading to increased customer retention rates and a stronger market position.

-

Risk Diversification:

- By engaging in diverse business activities, universal banks can reduce their exposure to any single market or financial product. If one sector faces challenges, the bank can continue to generate revenue from other sectors, mitigating overall risk.

-

Efficiency and Economies of Scale:

- Universal banks can achieve significant operational efficiencies by sharing resources and infrastructure across different business units. This leads to economies of scale and reduces overall costs.

- For example, a bank's customer service infrastructure, IT systems, and branch network can be used to support both retail banking and investment banking activities.

-

Regulatory Support and Systemic Stability:

- In many countries, regulators encourage universal banking to enhance the stability of the financial system. By allowing banks to diversify their activities, regulators aim to make them more resilient to economic shocks and reduce the risk of systemic crises.

-

Customer Convenience and Satisfaction:

-

Importance of Universal Banking:

-

Comprehensive Financial Solutions:

- Universal banks can provide integrated financial solutions tailored to the specific needs of individual and corporate clients. This may involve combining different products and services to create customized solutions that address complex financial challenges.

-

Promotes Financial Inclusion:

- Universal banks can play a significant role in promoting financial inclusion by extending access to a wide range of financial services to underserved communities.

- This includes offering micro-insurance, micro-loans, basic banking services, and financial literacy programs to individuals and small businesses that may not have access to traditional banking services.

-

Economic Growth and Development:

- By providing diverse financial products and services, universal banks contribute to the overall economic development of a country.

- They support businesses by providing working capital, financing infrastructure projects, and investing in various sectors that stimulate growth.

-

Enhanced Financial Literacy:

- Universal banks often provide educational resources and advisory services to customers, helping them understand the full range of financial products available and make informed financial decisions.

- This enhances financial literacy across different segments of the population and empowers individuals to take control of their financial well-being.

-

Comprehensive Financial Solutions:

Core Banking Solution (CBS): The Technological Backbone of Modern Banking

Core Banking Solution (CBS) refers to the centralized banking system that enables banks to provide seamless and integrated services to their customers across all branches and digital platforms. It integrates all the bank's functions into a single IT system, improving efficiency, customer service, and regulatory compliance.

-

Need for CBS:

-

Centralized Operations:

- CBS allows for centralized processing and real-time updating of customer accounts across all branches of a bank. This means that customers can access their accounts and perform transactions from any branch or digital platform, regardless of where their account was originally opened.

- This eliminates the need for manual reconciliation and ensures that all customer data is consistent and up-to-date.

-

Improved Customer Experience:

- CBS enhances the customer experience by providing a seamless and consistent banking experience across all channels.

- Customers can check their balance, transfer funds, pay bills, and avail of other banking services from any branch, ATM, mobile app, or online banking platform.

-

Operational Efficiency:

- By automating most banking operations and centralizing data, CBS reduces manual interventions, streamlines processes, and improves efficiency.

- This leads to lower operational costs, faster turnaround times, and improved accuracy.

-

Real-time Processing:

- CBS enables real-time processing of transactions, meaning that updates to customer accounts (such as deposits, withdrawals, and transfers) are reflected immediately.

- This ensures accurate and timely information for both the bank and the customer.

-

Regulatory Compliance:

- Core banking systems facilitate compliance with regulatory requirements by ensuring that customer data is stored securely, transaction records are maintained accurately, and audit trails are available for scrutiny.

- This helps banks adhere to national and international banking standards and regulations.

-

Facilitates Digital Banking:

- CBS provides the backbone for digital banking platforms, such as mobile banking, internet banking, and ATMs. These services rely on CBS for real-time data synchronization and customer interactions, allowing banks to offer 24/7 banking services.

-

Data Analytics and Reporting:

- CBS helps banks gather and analyze large volumes of customer data, providing valuable insights that can be used to improve services, identify trends, and offer personalized products.

- This also supports decision-making, risk management, and regulatory reporting.

-

Centralized Operations:

-

Key Features of Core Banking Solutions (CBS):

- Centralized Database: All customer data, including account details, transaction history, and loan information, is stored in a central repository that can be accessed across multiple branches and channels.

- Online Transaction Processing (OLTP): CBS enables real-time updates to customer accounts, allowing for online banking, mobile banking, and inter-branch transactions.

- Inter-Branch Banking: Customers can avail themselves of banking services at any branch of the bank, regardless of where their account was originally opened.

- 24/7 Accessibility: With CBS, customers can access their accounts and perform transactions at any time, from anywhere, through online banking, ATMs, and mobile apps.

- Enhanced Security Features: Core banking systems are equipped with advanced security protocols, such as encryption, multi-factor authentication, and secure access controls, to protect sensitive customer data.

- Multi-Channel Support: CBS enables banks to offer services through various channels, such as physical branches, mobile apps, ATMs, and online platforms, ensuring accessibility for all customers.

- Efficient Loan and Payment Management: CBS helps in managing loans, repayments, and other payment-related activities effectively, ensuring accuracy in disbursement and collection.

-

Importance of Core Banking Solutions (CBS):

-

Scalability and Growth:

- As banks expand and open new branches or offer new products and services, CBS allows them to scale their operations without the need for significant infrastructure changes.

-

Cost Savings:

- CBS reduces operational costs by minimizing manual processes and enabling digital channels. It streamlines various banking functions, reducing overhead costs and improving profitability.

-

Improved Risk Management:

- CBS enhances the bank's ability to manage risks, such as fraud detection and compliance, through centralized control, data analytics, and monitoring tools.

-

Faster Service Delivery:

- Real-time processing of transactions ensures that customers experience faster and more efficient banking services, from fund transfers to loan disbursals.

-

Enhances Competitive Advantage:

- With the integration of CBS, banks can offer more innovative services, improve customer satisfaction, and keep pace with the evolving financial landscape.

-

Scalability and Growth:

Summary:

- Universal Banking: A model that provides a wide range of financial services under one roof, enhancing customer convenience, diversifying revenue sources, and promoting financial stability.

-

Core Banking Solution (CBS): A centralized IT system that enables real-time, seamless banking services across all branches and digital platforms, improving operational efficiency, customer service, and regulatory compliance.

In conclusion, Universal Banking and Core Banking Solutions are both essential elements in the evolution of modern banking. While Universal Banking defines the scope of services offered by a financial institution, CBS provides the technological infrastructure that enables efficient and customer-centric delivery of those services. Together, they empower banks to thrive in an increasingly competitive and dynamic financial landscape.

No Comments