Non-Banking Financial Companies (NBFCs)

Non-Banking Financial Companies (NBFCs) are financial institutions that provide a range of banking services without holding a full-fledged banking license. While they are regulated by the Reserve Bank of India (RBI), they operate under a different regulatory framework than commercial banks, allowing them greater flexibility and specialization. NBFCs are instrumental in promoting financial inclusion by extending credit to various sectors, particularly those that are underserved by traditional banks.

-

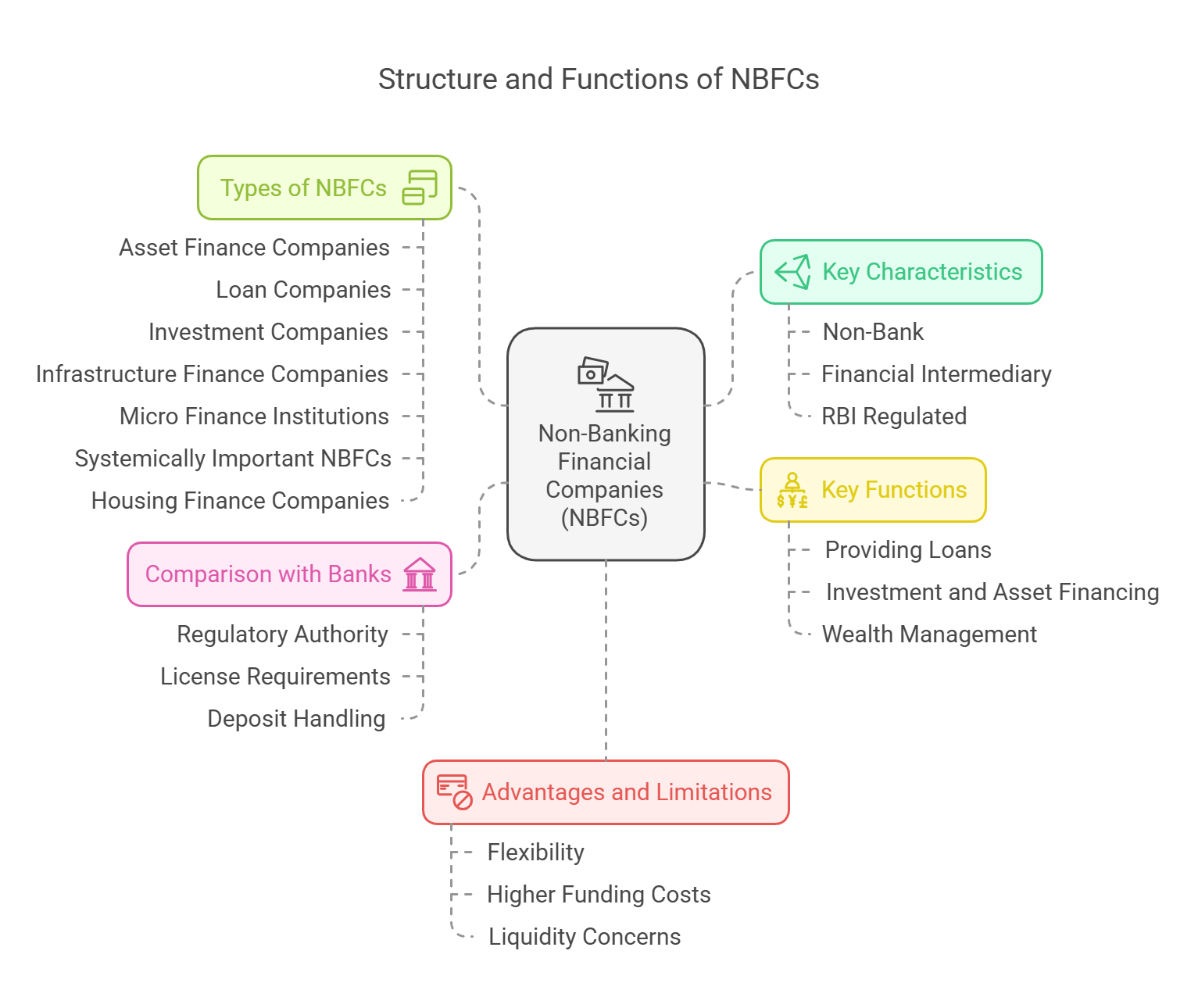

Key Characteristics of NBFCs:

- Non-Bank: They do not have a banking license and cannot accept demand deposits from the public.

- Financial Intermediary: They provide financial services, such as lending, leasing, and investment.

- RBI Regulated: They are regulated and supervised by the RBI, which sets guidelines on capital adequacy, asset quality, and risk management.

- Specialized Services: They often specialize in specific sectors or types of lending, such as asset finance, microfinance, or infrastructure finance.

- Complementary Role: They complement the role of banks by providing access to credit to segments that may not be easily served by banks.

Types of NBFCs:

The RBI categorizes NBFCs based on their principal business activity:

-

Asset Finance Companies (AFCs):

- Definition: AFCs are NBFCs that primarily finance physical assets that support productive economic activity, such as vehicles, machinery, and equipment.

- Function: They provide loans for the purchase of these fixed assets to individuals and businesses.

- Example: NBFCs that provide loans for commercial vehicles, construction equipment, or industrial machinery.

-

Loan Companies (LCs):

- Definition: LCs are NBFCs that provide a wide range of loans for various purposes, such as personal loans, working capital, and consumption loans.

- Function: They lend funds for general purposes and do not specialize in asset financing like AFCs.

- Example: Personal loan providers, payday loan companies, or small business lenders.

-

Investment Companies (ICs):

- Definition: ICs are NBFCs that primarily engage in the acquisition of securities, such as stocks, bonds, and debentures.

- Function: They hold these securities for investment purposes, deal in them for their own account or on behalf of their clients, and may provide investment advisory services.

- Example: Mutual funds, portfolio management services, or stock brokerage firms.

-

Infrastructure Finance Companies (IFCs):

- Definition: IFCs are NBFCs that provide financing for infrastructure projects, such as highways, ports, airports, power plants, and other large-scale infrastructure developments.

- Function: They provide long-term loans and other forms of financing to support the development of critical infrastructure projects.

- Example: Infrastructure-focused NBFCs that lend to the construction or energy sectors.

-

Micro Finance Institutions (MFIs):

- Definition: MFIs are specialized NBFCs that provide micro-loans to low-income individuals or groups, typically for small-scale businesses or entrepreneurial activities in rural and semi-urban areas.

- Function: They aim to promote financial inclusion and empower individuals to start or expand their businesses.

- Example: Micro-lenders that provide loans to small vendors, farmers, or artisans.

-

Systemically Important Non-Banking Financial Companies (SI-NBFCs):

- Definition: These are NBFCs identified by the RBI as being of significant importance to the financial system due to their size, scale, and interconnectedness.

- Function: Due to their potential impact on financial stability, SI-NBFCs are subject to more stringent regulations and supervision compared to other NBFCs.

- Example: Large NBFCs such as HDFC Ltd., Bajaj Finance Ltd., and Mahindra & Mahindra Financial Services Ltd.

-

Housing Finance Companies (HFCs):

- Definition: HFCs are a special category of NBFCs that specialize in providing housing loans to individuals and businesses for the construction or purchase of residential properties.

- Function: They play a key role in promoting homeownership and supporting the housing sector.

- Example: HDFC Ltd., LIC Housing Finance Ltd., and IndiaBulls Housing Finance Ltd.

Key Functions of NBFCs:

NBFCs perform a variety of functions that contribute to the overall financial system:

- Providing Loans and Advances: NBFCs offer various types of loans to individuals, businesses, and institutions.

- Investment and Asset Financing: They invest in securities and provide financing for physical assets.

- Wealth Management and Advisory Services: Some NBFCs offer financial advisory services and wealth management services.

- Microfinance and Financial Inclusion: MFIs extend small loans to underserved populations, promoting financial inclusion.

- Leasing and Hire Purchase: Some NBFCs engage in leasing and hire purchase activities, providing financing for the use of assets over a specified period.

Comparison Between Banks and NBFCs:

While both banks and NBFCs provide financial services, there are several key differences between them:

| Aspect | Banks | NBFCs |

|---|---|---|

| Regulatory Authority | Regulated by the Reserve Bank of India (RBI) and other regulators like SEBI (for capital markets). | Regulated by the Reserve Bank of India (RBI), but subject to fewer restrictions. |

| License | Banks must obtain a banking license from the RBI to operate. | NBFCs do not require a banking license. |

| Deposits | Can accept demand deposits from the public (savings, current, fixed deposits). | Cannot accept demand deposits from the public. They rely on borrowings from banks, other financial institutions, and capital markets. |

| Loan Disbursements | Banks can issue loans from deposits and have the ability to create money through credit creation. | NBFCs provide loans primarily through borrowed funds and their own capital. |

| Payment and Settlement Systems | Can offer a full range of payment services like RTGS, NEFT, IMPS, UPI, ATM services, and cheque clearing. | Cannot offer payment services like cheque books or ATM withdrawals. |

| Deposit Insurance | Deposits are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC) up to a certain limit (currently ₹5 lakh). | Deposits made with NBFCs are not insured. |

| Capital Requirement | Banks have a more stringent capital adequacy ratio (CAR) under Basel norms (minimum 9%). | NBFCs have a lower CAR requirement compared to banks, though it varies by type. |

| Types of Services | Offer a wide variety of services, including savings accounts, loans, foreign exchange, wealth management, and more. | Offer a more focused range of services, including loans, asset financing, investment services, and microfinance. |

| Risk of Liquidity | Banks generally have access to liquidity support from the RBI (lender of last resort). | NBFCs may face greater liquidity risk if their borrowings are not well-managed. |

| Access to Funds | Banks can access funding from the RBI through the repo window and other mechanisms. | NBFCs primarily rely on the capital markets, debentures, and borrowing from other financial institutions. |

| Focus on Lending | Banks lend to a broad range of sectors, including individuals, businesses, and governments. | NBFCs often focus on specific sectors, such as housing, microfinance, infrastructure, or vehicle finance. |

| Branch Network | Banks typically have extensive branch networks, providing widespread access to their services. | NBFCs may have fewer branches than banks, often relying on digital channels and partnerships to reach customers. |

| Customer Base | Banks serve a wide range of customers, from individuals to large corporations. | NBFCs often focus on serving specific segments, such as low-income individuals, small businesses, or specific industries. |

Advantages of NBFCs:

- Flexibility: NBFCs are more flexible in their operations and can offer products tailored to niche markets.

- Faster Processing: They can often process loans and approvals faster compared to banks due to less regulatory oversight.

- Specialized Expertise: They may have specialized expertise in specific sectors, allowing them to better assess risk and provide tailored financing solutions.

- Accessibility: They can reach underserved segments of the population that may not have access to traditional banking services.

Limitations of NBFCs:

- No Deposit Taking: The inability to accept demand deposits limits their ability to generate low-cost funds.

- Higher Funding Costs: They depend on borrowing or issuing securities to raise capital, which can be more expensive than deposit funding.

- Lower Regulation: While offering operational flexibility, it also means less protection for customers compared to regulated banks.

- Liquidity Concerns: They face potentially higher liquidity risks and do not have the same access to emergency liquidity support mechanisms as banks.

Summary:

- NBFCs are important financial intermediaries that play a crucial role in financial inclusion and lending to specific sectors. They complement the role of banks by providing access to credit to underserved segments of the economy.

- Banks are highly regulated and offer a broader range of financial services, including deposit-taking, lending, and payment systems.

- The key differences between banks and NBFCs lie in their ability to accept deposits, the regulatory framework they operate under, and the range of services they offer. Both types of institutions are essential for a well-functioning financial system.

No Comments