Barrier Options

Triggering Payoffs with Price Levels

Barrier options are options whose existence and/or payoff depend on whether the underlying asset's price reaches a pre-specified barrier level during the option's life. This introduces a path-dependent element, as the option's history matters.

-

What it is: A barrier option is a type of option contract with a payoff dependent on whether the underlying asset's price reaches or exceeds a certain price (the "barrier"). If the barrier is breached, the option can either become worthless ("knock-out") or come into existence ("knock-in").

-

Key Features:

- Barrier Level: The pre-defined price level that triggers a change in the option's status.

- Knock-Out or Knock-In: Determines whether the option ceases to exist or comes into existence when the barrier is hit.

- Monitoring: The barrier can be monitored continuously or discretely (e.g., only at the end of each day).

- Rebate: Some barrier options offer a rebate if the barrier is hit and the option knocks out.

-

Types:

-

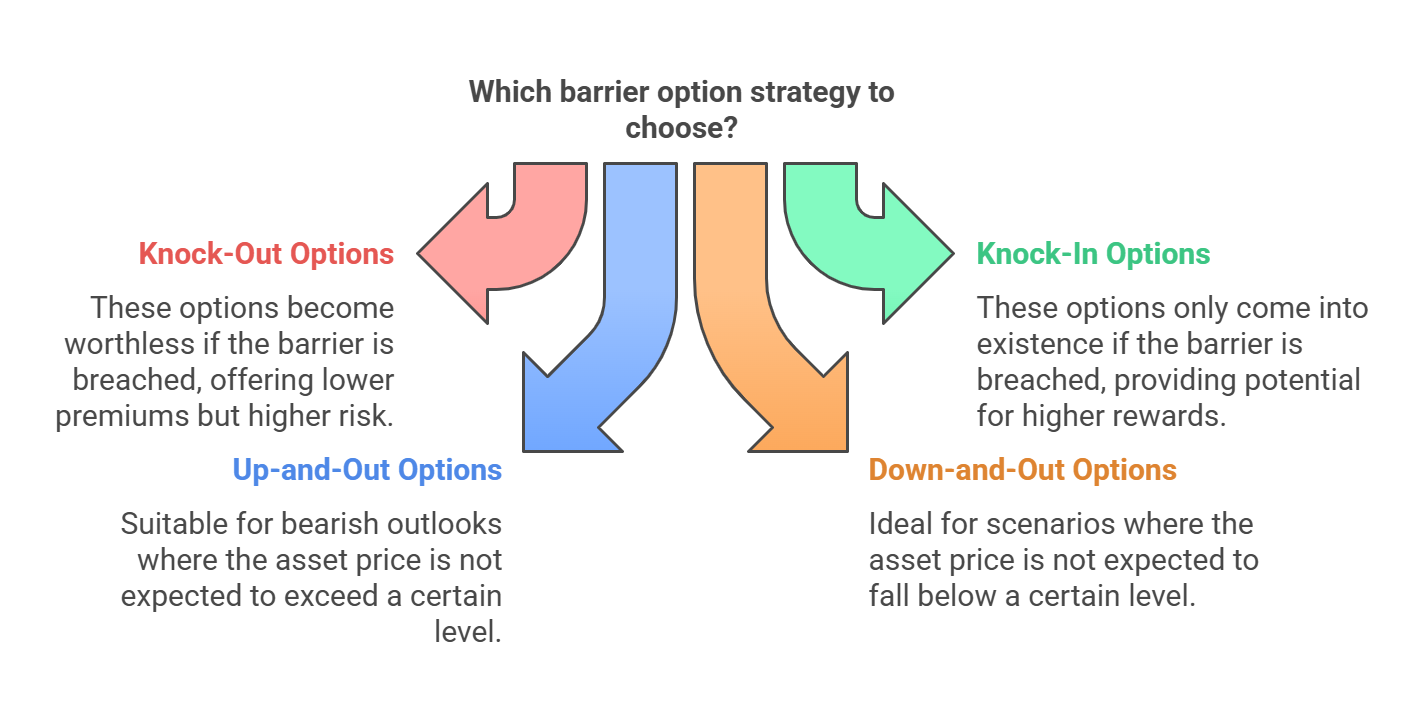

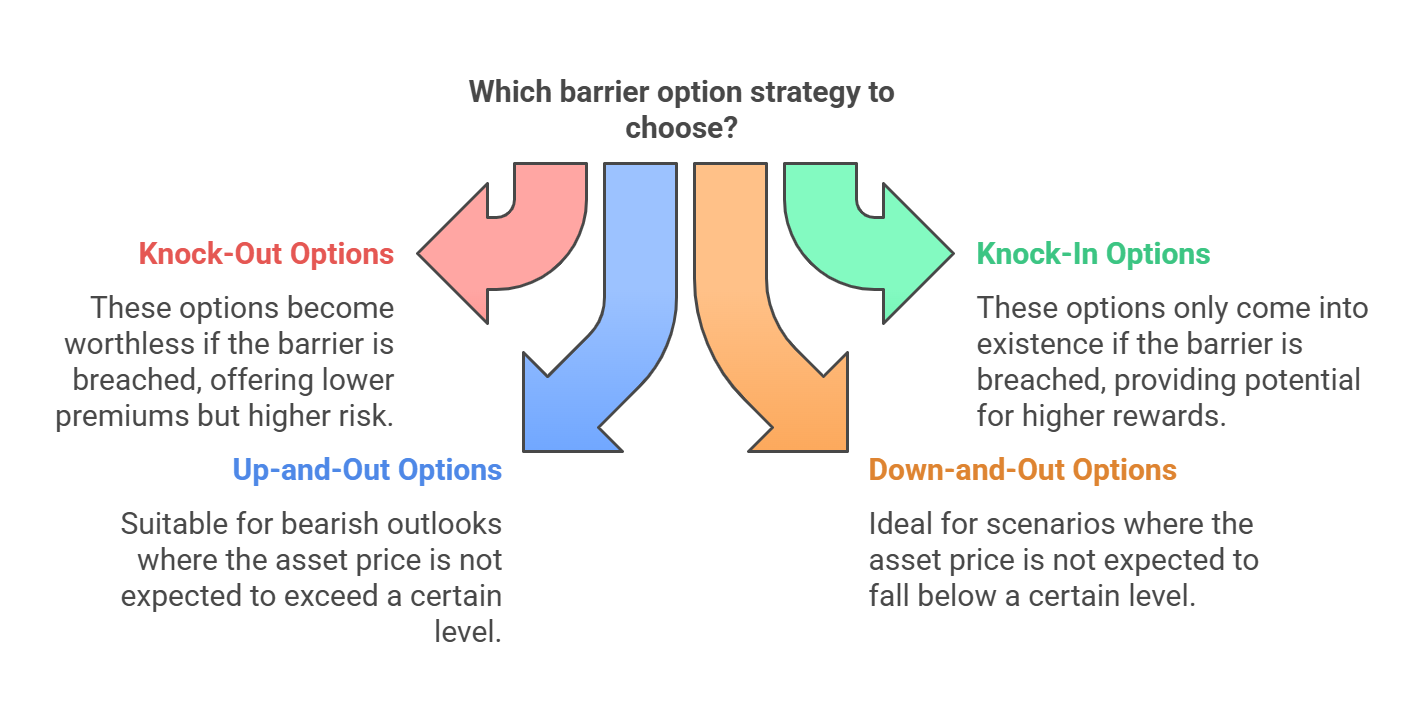

Knock-Out Options:

- Up-and-Out Call: Behaves like a standard call option, unless the underlying asset's price reaches the barrier level from below. If the barrier is hit, the option becomes worthless.

- Down-and-Out Call: Behaves like a standard call option, unless the underlying asset's price reaches the barrier level from above. If the barrier is hit, the option becomes worthless.

- Up-and-Out Put: Behaves like a standard put option, unless the underlying asset's price reaches the barrier level from below. If the barrier is hit, the option becomes worthless.

- Down-and-Out Put: Behaves like a standard put option, unless the underlying asset's price reaches the barrier level from above. If the barrier is hit, the option becomes worthless.

-

Knock-out options are cheaper than standard options because the barrier provides a limit to the option's life

-

Knock-In Options:

- Up-and-In Call: Only comes into existence if the underlying asset's price reaches the barrier level from below. After the barrier is hit, it behaves like a standard call option.

- Down-and-In Call: Only comes into existence if the underlying asset's price reaches the barrier level from above. After the barrier is hit, it behaves like a standard call option.

- Up-and-In Put: Only comes into existence if the underlying asset's price reaches the barrier level from below. After the barrier is hit, it behaves like a standard put option.

- Down-and-In Put: Only comes into existence if the underlying asset's price reaches the barrier level from above. After the barrier is hit, it behaves like a standard put option.

-

-

Purpose:

- Reduced Premium: Barrier options are typically cheaper than standard options because of the barrier feature.

- Specific Market Views: Allow traders to express specific views on price levels and volatility.

-

Examples:

- An up-and-out call option on XYZ stock with a strike price of $50 and a barrier level of $60. If the stock price reaches $60 before expiration, the option becomes worthless.

-

Payoff (at Expiration):

- The payoff depends on whether the barrier has been hit and whether the option is knock-in or knock-out.

-

Valuation:

- Barrier options can be valued using analytical formulas or numerical methods (e.g., binomial trees, Monte Carlo simulation). The valuation is more complex than for standard options due to the barrier feature.

-

Relationship between Knock-in and Knock-out Options

-

European Style:

-

Call = Down-and-Out Call + Down-and-In Call

-

Put = Up-and-Out Put + Up-and-In Put

-

Hedging

-

Static hedge is typically used for the barrier options, as opposed to dynamic hedging used for the vanilla options

In summary, barrier options offer a way to fine-tune option strategies by adding a condition based on price levels.

No Comments