Path-Dependent Options

The Journey Matters

These exotic options have payoffs that depend not only on the underlying asset's price at expiration, but also on the path the price takes over the option's life. This path dependency adds complexity to their valuation and risk management.

-

Asian Options (Average Options):

-

What it is: An Asian option (or average option) has a payoff that depends on the average price of the underlying asset over a specified period, rather than the price at expiration.

-

Key Features:

- Averaging Period: The period over which the average price is calculated.

- Averaging Method: Can be arithmetic (simple average) or geometric (the nth root of the product of prices).

- Lower Volatility Sensitivity: Generally less sensitive to volatility than standard options because the averaging process smooths out price fluctuations.

-

Types:

- Average Price Call: Pays max(0, Average Price - K) at expiration.

- Average Price Put: Pays max(0, K - Average Price) at expiration.

- Average Strike Call: Pays max(0, S - Average Price) at expiration.

- Average Strike Put: Pays max(0, Average Price - S) at expiration.

-

Purpose:

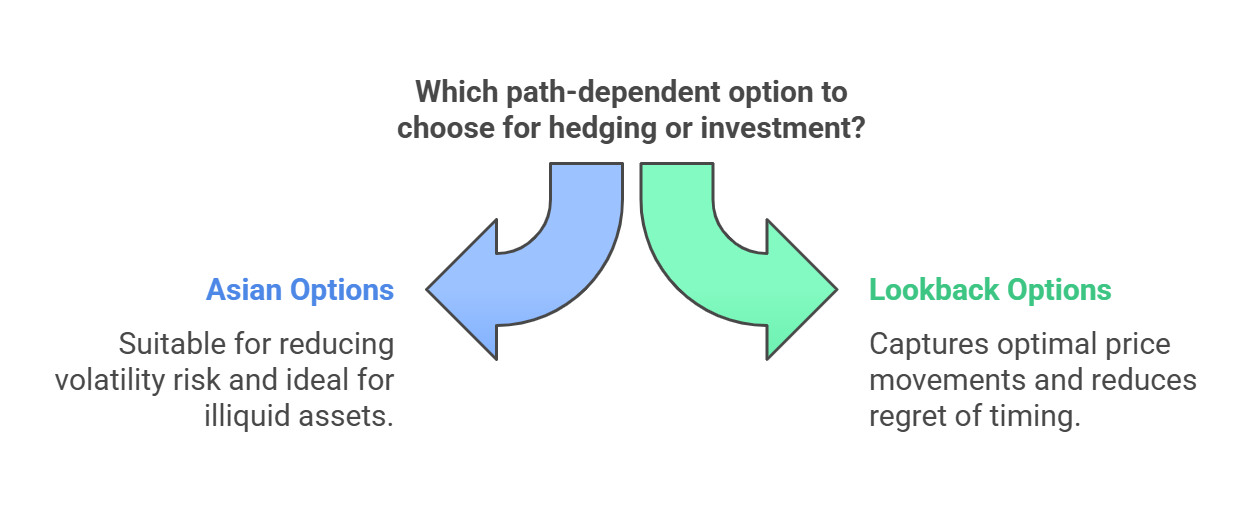

- Reducing Volatility Risk: The averaging feature reduces the impact of price volatility, making them attractive for hedging.

- Suitable for Illiquid Assets: Useful for assets that are traded infrequently, as the average price is less susceptible to manipulation.

-

Example:

- An average price call option on a stock with a strike price of $50. The average price is calculated daily over the last three months of the option's life. If the average price is $55 at expiration, the option pays $5.

-

Payoff Formulas:

- Average Price Call: max(0, Average Price - K)

- Average Price Put: max(0, K - Average Price)

- Average Strike Call: max(0, S - Average Price)

- Average Strike Put: max(0, Average Price - S)

-

-

Lookback Options:

-

What it is: A lookback option has a payoff that depends on the highest or lowest price of the underlying asset during the option's life.

-

Key Features:

- Retrospective Determination of Payoff: The payoff is determined by looking back at the asset's price history over the option's life.

- Higher Premium: Typically more expensive than standard options because they guarantee a favorable outcome.

-

Types:

- Fixed Strike Lookback Call: Pays max(0, Max Price - K) at expiration.

- Fixed Strike Lookback Put: Pays max(0, K - Min Price) at expiration.

- Floating Strike Lookback Call: Pays (S - Min Price) at expiration.

- Floating Strike Lookback Put: Pays (Max Price - S) at expiration.

-

Purpose:

- Capturing Optimal Price Movements: Allows holders to benefit from the most favorable price movements during the option's life.

- Reducing Regret: Eliminates the regret of not exercising at the optimal time.

-

Example:

- A floating strike lookback call option. At expiration, the payoff is the difference between the stock price at expiration and the lowest price reached during the option's life.

-

Payoff Formulas:

- Fixed Strike Lookback Call: max(0, Max Price - K)

- Fixed Strike Lookback Put: max(0, K - Min Price)

- Floating Strike Lookback Call: (S - Min Price)

- Floating Strike Lookback Put: (Max Price - S)

-

Comparison Table:

| Feature | Asian Option (Average Option) | Lookback Option |

|---|---|---|

| Payoff Dependence | Average price over a period | Highest or lowest price during the option's life |

| Volatility Sensitivity | Lower | Higher |

| Primary Use | Reducing volatility risk, illiquid assets | Capturing optimal price movements, reducing regret |

No Comments