Gamma Neutral

Shielding Your Portfolio from Delta's Mood Swings

Gamma neutrality takes risk management a step further than delta neutrality. While delta hedging protects against small price changes, gamma hedging aims to protect against changes in delta itself. In essence, you're trying to make your portfolio less sensitive to the speed at which your delta exposure changes.

Understanding the Need for Gamma Neutrality:

- Delta Hedging Isn't Perfect: Delta is a linear approximation of the option price's sensitivity to the underlying asset's price. This approximation is only accurate for small price movements.

- Gamma Measures the "Curve": Gamma quantifies the curvature of the option price function. It tells you how much the delta will change for each $1 move in the underlying asset.

- High Gamma = Unstable Delta: A high gamma means your delta hedge can quickly become ineffective if the stock price makes a significant move. You'll need to rebalance your hedge more frequently, incurring transaction costs and potential tracking error.

- Gamma Neutrality Reduces Rebalancing: A gamma-neutral portfolio is less sensitive to changes in delta, reducing the need for frequent rebalancing and improving the stability of your hedge.

How to Achieve Gamma Neutrality:

-

Determine Your Starting Position:

- Identify all options in your portfolio: Gamma hedging primarily involves options because they have the highest gamma.

- Calculate the Gamma of each option: Use the Black-Scholes model or a similar pricing model.

- Calculate the total portfolio Gamma: Sum the gammas of all your options, considering the number of units of each option you hold.

Formula:

- Portfolio Gamma = (Gamma of Option 1 * Number of Units of Option 1) + (Gamma of Option 2 * Number of Units of Option 2) + ...

-

Offset the Portfolio Gamma:

- Use other options to offset the existing Gamma: Since Gamma is always positive (or very close to it) for standard options, you typically need to combine different option positions to achieve gamma neutrality.

-

Common strategies:

- Buying and selling options with different strike prices: This is the most common approach.

- Using options with different expiration dates: This can also affect the overall portfolio gamma.

- Important Note: You cannot eliminate gamma risk simply by buying or selling the underlying asset. The underlying asset has zero gamma.

-

Rebalance Regularly:

- Gamma changes constantly: As the price of the underlying asset and other factors (like volatility) change, the gammas of your options will also change.

- Regularly recalculate your portfolio Gamma: Determine if you need to adjust your hedge.

- Rebalance your gamma hedge: Buy or sell additional options to maintain gamma neutrality. This will also affect your delta, so you will usually have to adjust both.

Example:

-

Your Portfolio:

- You own 10 Call Options on XYZ stock with a Gamma of 0.05 each (Total Gamma = 10 * 0.05 * (100 shares/option)^2 = 500)

-

Hedge Action:

- Sell 5 Call Options on XYZ stock with a Gamma of 0.10 each (Total Gamma = -5 * 0.10 * (100 shares/option)^2 = -500)

-

Result:

- Your portfolio is now Gamma-neutral (or very close to it). Large changes in the price of XYZ stock should have less impact on the stability of your delta hedge.

Important Considerations:

- Gamma Hedging is More Complex: Gamma hedging is significantly more complex and expensive than delta hedging. It requires a deeper understanding of options pricing and risk management.

- Transaction Costs: Trading multiple options to achieve gamma neutrality can generate substantial transaction costs.

- Vega Risk: Gamma hedging often increases your exposure to Vega risk (sensitivity to changes in volatility). This is because the options you use to hedge gamma will also have Vega. You need to carefully consider this trade-off.

- Theta (Time Decay): Gamma-neutral portfolios can also be more sensitive to time decay (Theta).

- Liquidity: You need to be able to buy and sell the required options easily and at reasonable prices.

- Model Risk: Gamma calculations rely on pricing models that make simplifying assumptions. The accuracy of your gamma hedge depends on the accuracy of the model.

Why Gamma Neutrality Matters:

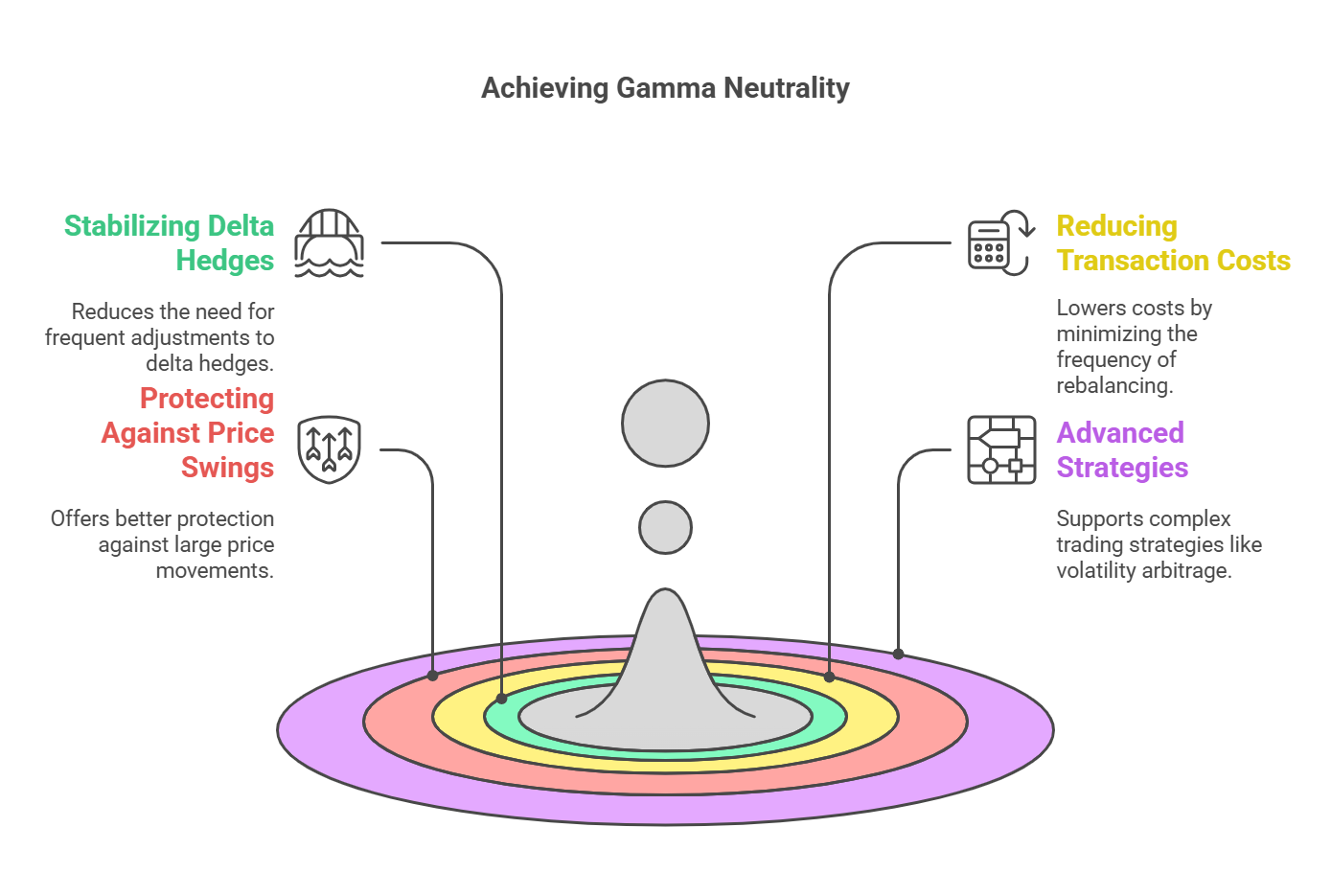

- Stabilizing Delta Hedges: Gamma neutrality helps to stabilize delta hedges, reducing the need for frequent rebalancing.

- Reducing Transaction Costs: By reducing rebalancing, gamma neutrality can help to lower transaction costs.

- Protecting Against Large Price Swings: Gamma neutrality provides better protection against large, unexpected price movements than delta hedging alone.

- Advanced Strategies: Gamma neutrality is a key component of many advanced options trading strategies, such as volatility arbitrage and dynamic hedging.

No Comments