Numerical example

Let's work through a complete numerical example for each Greek (Delta, Theta, Gamma, Vega, and Rho) for both a stock option (no dividend) and a currency option using the formulas.

Scenario:

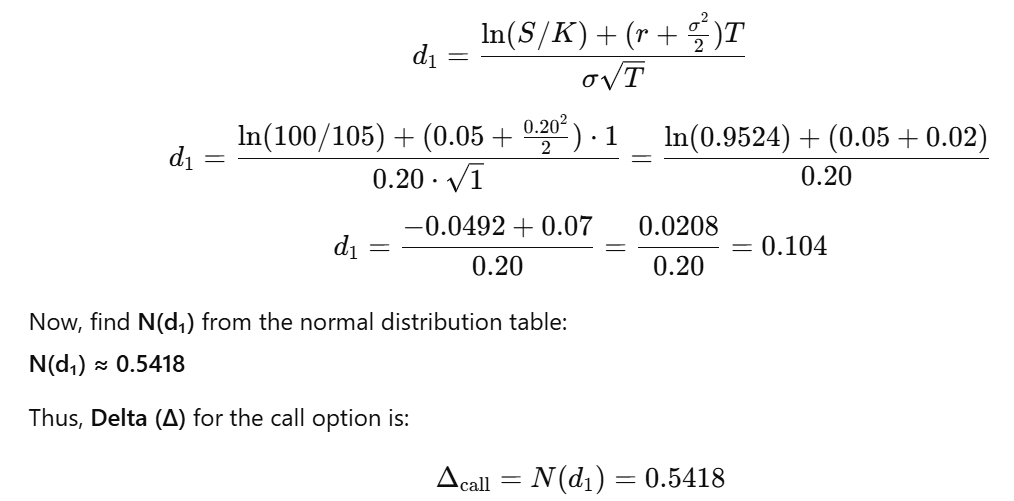

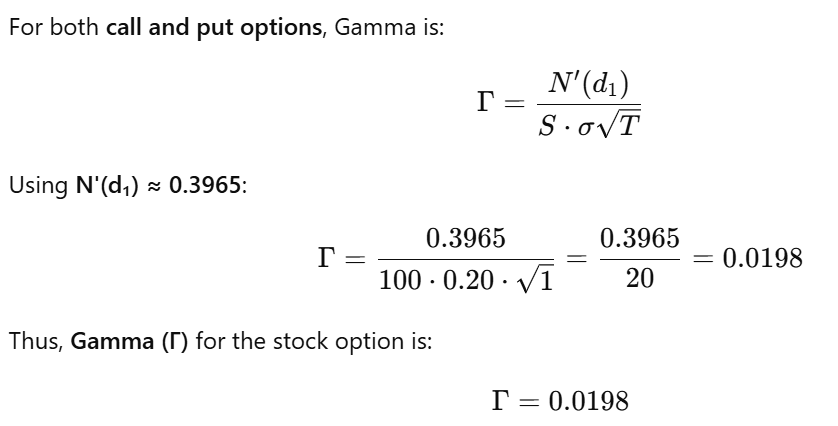

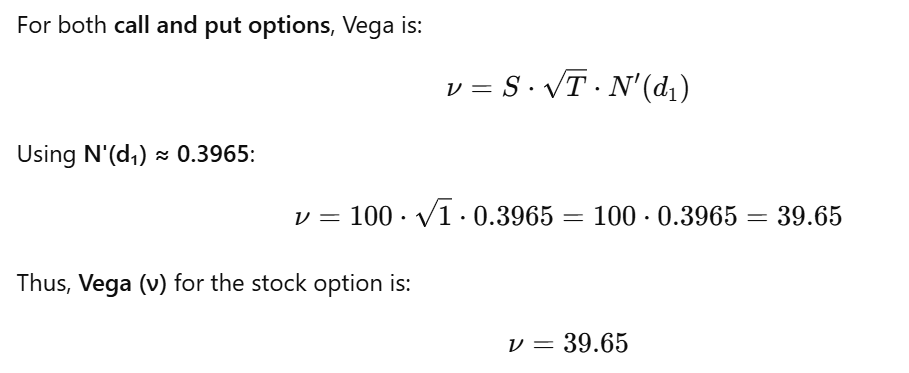

Stock Option (No Dividend):

- Stock Price (S) = ₹100

- Strike Price (K) = ₹105

- Time to Expiration (T) = 1 year

- Volatility (σ) = 20% (0.20)

- Risk-Free Interest Rate (r) = 5% (0.05)

- Dividend Yield (q) = 0%

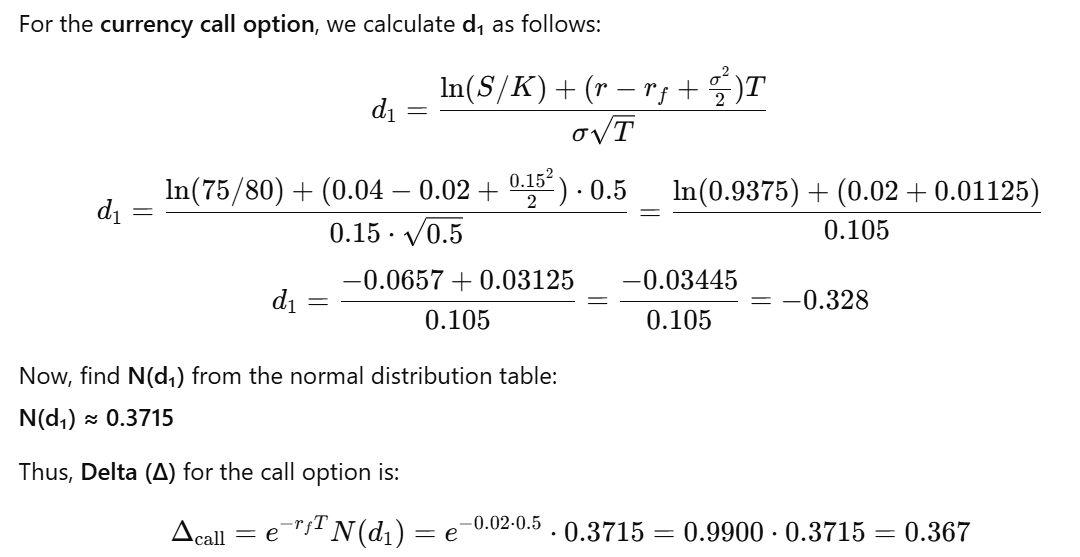

Currency Option:

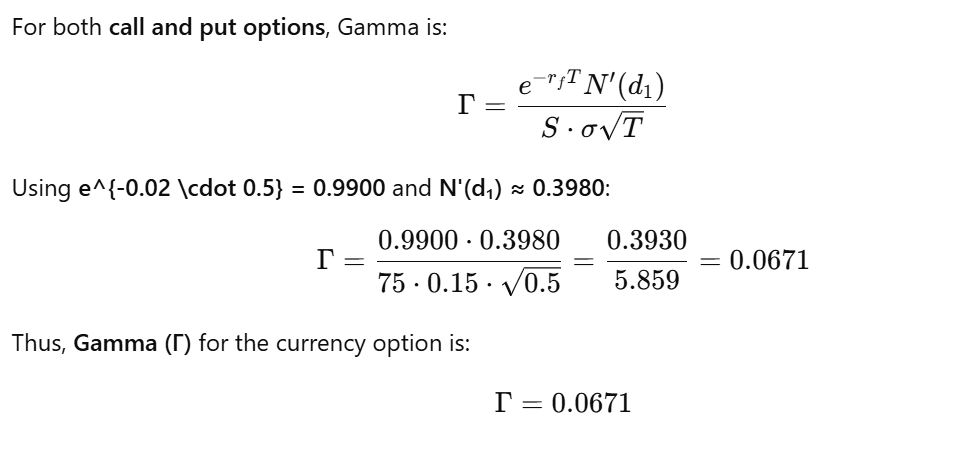

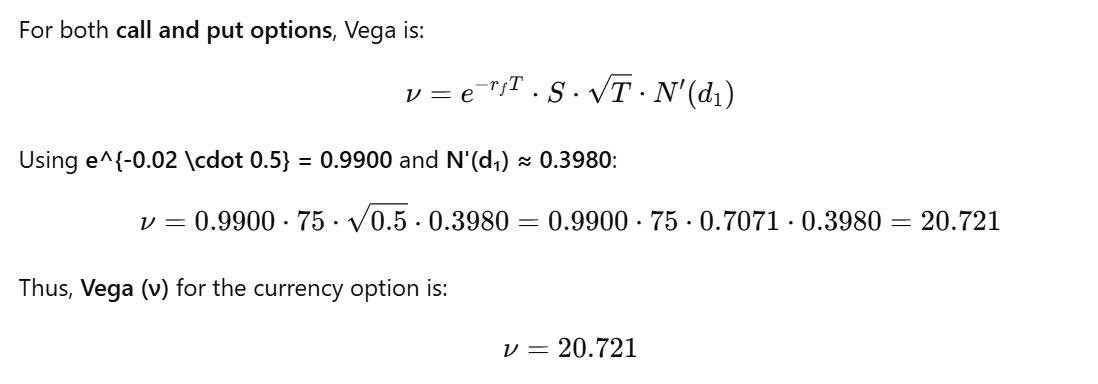

- Spot Price (S) = ₹75 (foreign currency per 1 unit)

- Strike Price (K) = ₹80

- Time to Expiration (T) = 0.5 years

- Volatility (σ) = 15% (0.15)

- Risk-Free Interest Rate (r) = 4% (0.04)

- Foreign Interest Rate (r_f) = 2% (0.02)

1. Delta (Δ)

Stock Option (No Dividend):

Currency Option:

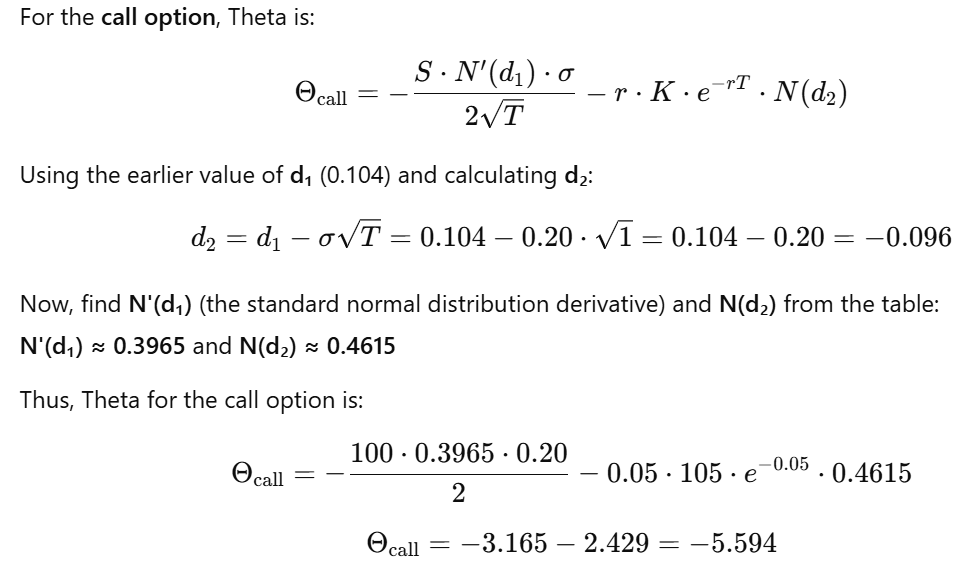

2. Theta (Θ)

Stock Option (No Dividend):

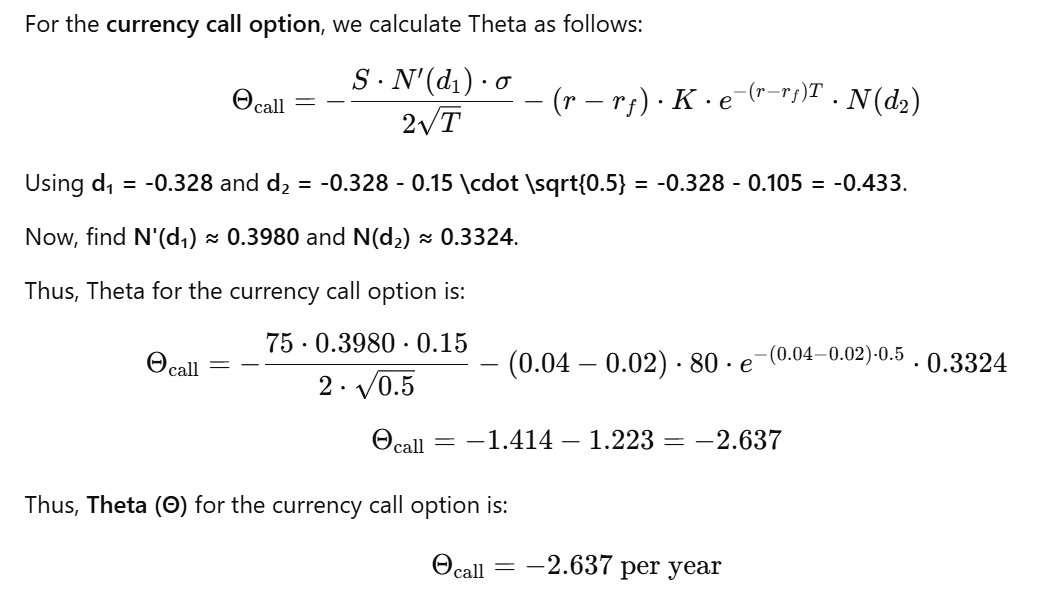

Currency Option:

3. Gamma (Γ)

Stock Option (No Dividend):

Currency Option:

4. Vega (ν)

Stock Option (No Dividend):

Currency Option:

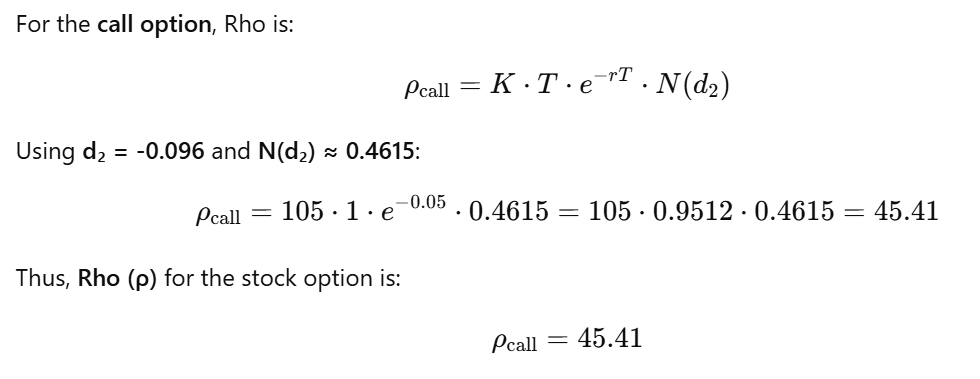

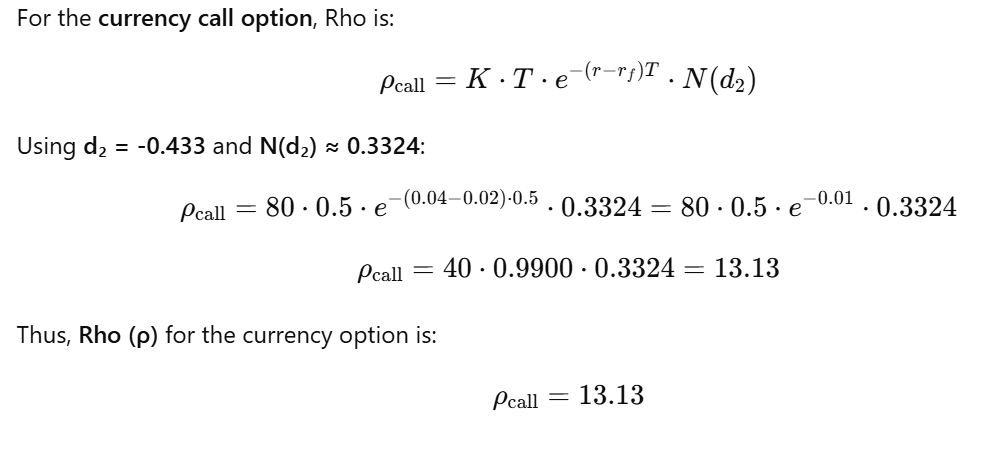

5. Rho (ρ)

Stock Option (No Dividend):

Currency Option:

Summary Table of Results:

| Greek | Stock Option (No Dividend) | Currency Option |

|---|---|---|

| Delta | 0.5418 | 0.367 |

| Theta | -5.594 | -2.637 |

| Gamma | 0.0198 | 0.0671 |

| Vega | 39.65 | 20.721 |

| Rho | 45.41 | 13.13 |

This is how you calculate each of the Greeks for both a stock option (no dividend) and a currency option.

No Comments