Gamma Positive Delta Neutral

Profiting from Big Swings, Regardless of Direction

A "Gamma Positive, Delta Neutral" portfolio is designed to profit from significant price movements in the underlying asset, regardless of whether the price goes up or down. It's a strategy for volatility trading, where you're betting on a large price swing but are unsure of the direction.

Understanding the Components:

- Delta Neutral: The portfolio is designed to be insensitive to small changes in the price of the underlying asset. Ideally, the portfolio's value remains relatively constant as the asset price makes minor fluctuations.

- Gamma Positive: The portfolio will benefit from larger price swings in either direction. The portfolio's delta will become more positive if the price increases and more negative if the price decreases, leading to a profit.

How to Construct a Gamma Positive Delta Neutral Portfolio:

The key is to have a net long position in options, meaning you've bought more options than you've sold. This gives you positive gamma. You then manage the portfolio's delta to keep it near zero.

-

Establish a Gamma Positive Position:

- Buy Options: Buying options (calls, puts, or a combination) creates positive gamma.

- Straddle: A classic strategy is a long straddle, where you buy an at-the-money call and an at-the-money put with the same strike price and expiration date.

- Strangle: A long strangle involves buying an out-of-the-money call and an out-of-the-money put with the same expiration date. This offers a lower initial cost but requires a larger price move to become profitable.

- Butterfly Spread (as an Adjustment): While a standard butterfly spread is Gamma neutral, a modified butterfly spread can be used to fine-tune Gamma and Delta.

-

Maintain Delta Neutrality:

- Hedge with the Underlying Asset: The gamma positive position will also have a delta, and this delta will change as the underlying asset price moves. You'll need to continuously hedge with the underlying asset (buying or selling shares) to keep the overall portfolio delta close to zero.

Example: Long Straddle

- Action: Buy one at-the-money call option and one at-the-money put option with the same strike price and expiration date.

- Initial Delta: Ideally, close to zero (delta neutral). In practice, there might be a small delta, which you would hedge.

- Gamma: Positive.

- Profit Scenario: The portfolio profits if the underlying asset price moves significantly in either direction before expiration.

Why Use a Gamma Positive Delta Neutral Strategy?

- Betting on Volatility (Without Directional Bias): This strategy is ideal when you expect a large price move in the underlying asset but are unsure of the direction. You're betting on volatility, not on a specific price trend.

- Profit from Uncertainty: You profit from increased market uncertainty and large price swings.

- Limited Risk (Potentially): The maximum loss is limited to the premium paid for the options (minus any proceeds from selling shares as part of delta hedging).

- Requires Active Management: This strategy requires continuous monitoring and rebalancing.

Important Considerations:

- Theta (Time Decay): Gamma positive strategies are significantly affected by time decay. The options lose value as they approach expiration, even if the underlying asset price doesn't move.

- Transaction Costs: Active delta hedging (buying and selling shares to maintain delta neutrality) can generate substantial transaction costs, which can erode profits.

- Volatility Risk (Vega): This strategy benefits from increasing volatility. If implied volatility decreases, the value of your options will decline.

- Breakeven Points: Straddles and strangles have two breakeven points (one above and one below the strike price). The underlying asset price needs to move beyond these points before expiration for the strategy to be profitable.

- Assignment Risk: If you are short any options as part of the Gamma Neutral strategy, you have assignment risk

- Continuous Monitoring: A Gamma Positive Delta Neutral Strategy requires a continuous and active monitoring

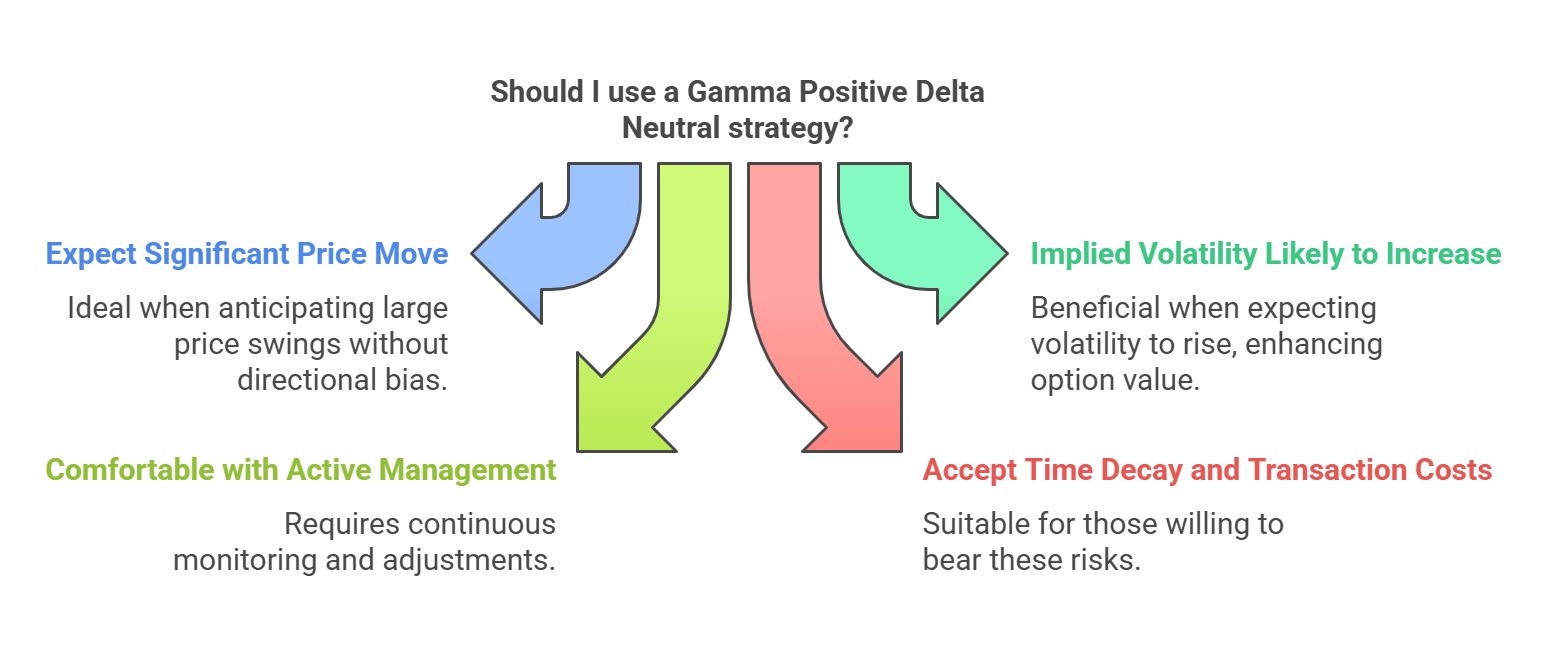

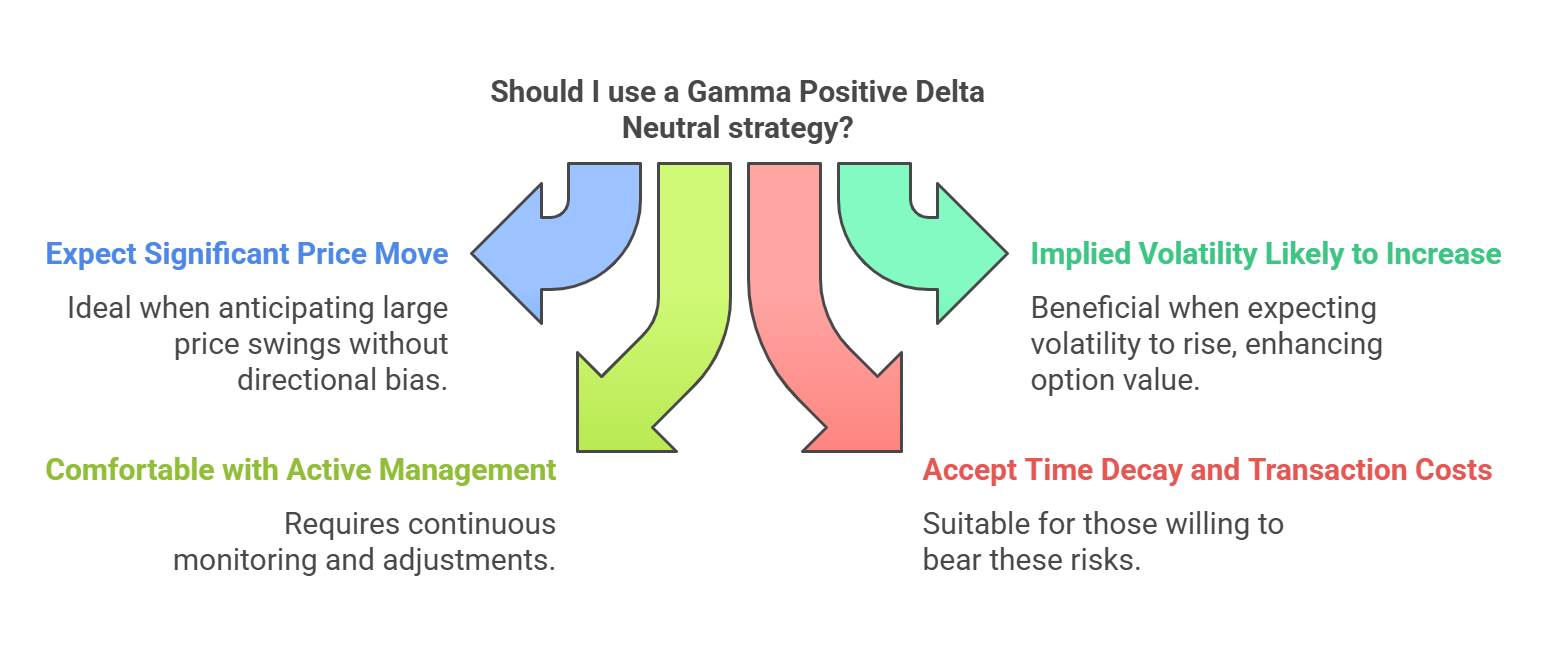

When to Use a Gamma Positive Delta Neutral Strategy:

- You expect a significant price move in the underlying asset, but you're unsure of the direction (e.g., before a major news announcement).

- You believe that implied volatility is low and likely to increase.

- You are comfortable with active portfolio management and monitoring.

-

You are willing to accept the risk of time decay and transaction costs.

No Comments