Introduction to Swaps

Exchanging Cash Flows

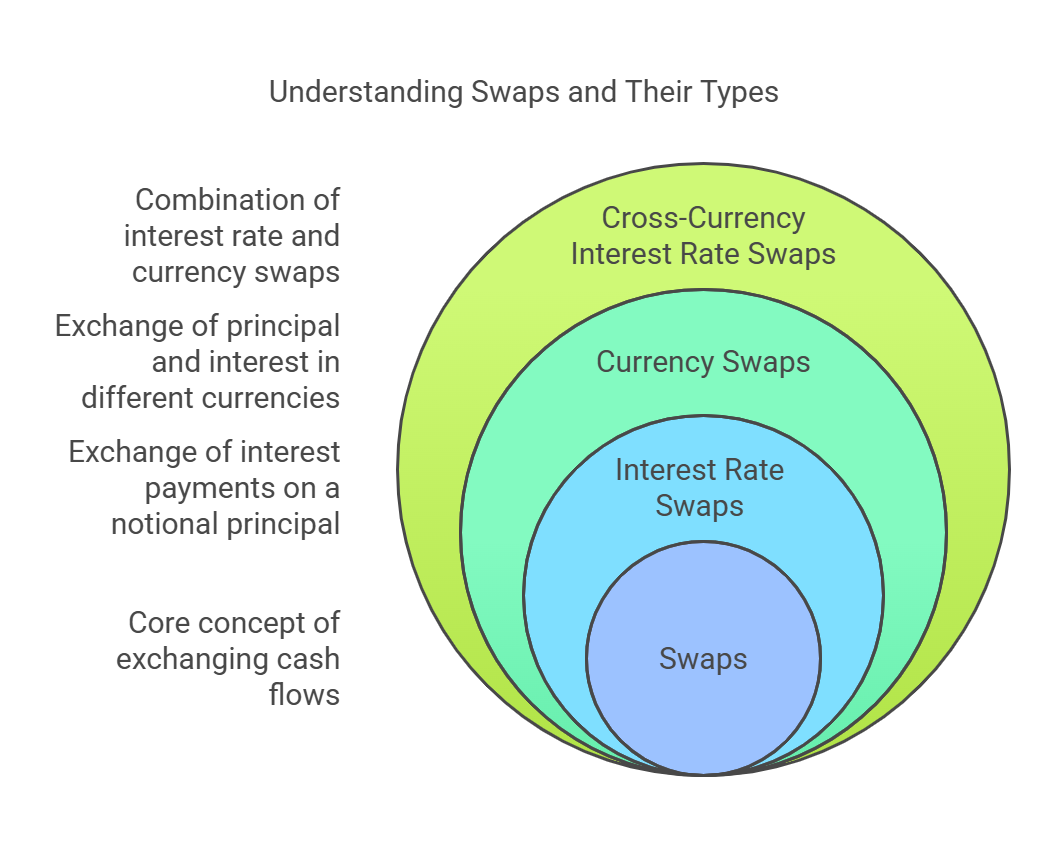

A swap is a derivative contract where two parties agree to exchange cash flows based on different financial instruments. Think of it as two companies agreeing to trade payment streams based on interest rates, currencies, or other assets. Swaps are typically customized agreements and are not exchange-traded.

Key Concepts:

- Notional Principal: This is a reference amount used to calculate the cash flows that are exchanged. It is not actually exchanged between the parties. Think of it as a measuring stick.

- Legs: Each side of the swap is called a leg. One leg typically pays a fixed rate, while the other pays a floating rate (or a different currency, etc.).

- Payment Dates: The dates on which the cash flows are exchanged.

- Netting: Typically, only the net difference between the two legs is paid on each payment date. This reduces the amount of cash that needs to be exchanged.

Types of Swaps:

-

Interest Rate Swaps (IRS):

-

What it is: An agreement to exchange interest rate payments on a notional principal. Typically, one party pays a fixed interest rate, and the other pays a floating interest rate (e.g., LIBOR, SOFR).

-

Purpose:

- Transforming Liabilities: A company with a floating-rate loan can use an IRS to convert it to a fixed-rate loan, providing more predictable interest expenses. Conversely, a company with a fixed-rate loan can convert it to a floating-rate loan.

- Speculation: Traders can use IRS to bet on the direction of interest rates.

-

Example:

- Company A pays Company B a fixed rate of 3% per year on a notional principal of $10 million.

- Company B pays Company A a floating rate equal to LIBOR + 1% per year on the same notional principal.

- If LIBOR is 2%, Company B would pay Company A 3% (LIBOR + 1%), while Company A would pay Company B 3%. The net payment is zero. If LIBOR is 4%, Company B would pay 5%, Company A would pay 3%, and the net payment would be $200,000 from Company B to Company A.

-

Formula (Simplified Net Payment Calculation):

- Net Payment = Notional Principal * (Floating Rate - Fixed Rate)

-

-

Currency Swaps:

- What it is: An agreement to exchange principal and interest payments in different currencies.

-

Purpose:

- Managing Currency Risk: Companies with revenues or expenses in different currencies can use currency swaps to hedge against exchange rate fluctuations.

- Accessing Foreign Capital Markets: Companies can use currency swaps to obtain financing in a foreign currency at a lower cost than they could obtain directly.

-

Example:

- Company A (based in the US) exchanges $10 million with Company B (based in the UK) for £8 million (the exchange rate is $1.25/£).

- Company A pays Company B interest on the £8 million at a fixed rate of 4% per year.

- Company B pays Company A interest on the $10 million at a fixed rate of 3% per year.

- At maturity, the principal amounts are exchanged back.

- Key Feature: Principal Exchange: Unlike interest rate swaps, currency swaps typically involve an exchange of principal at the beginning and the end of the swap. This is because the principal is in different currencies.

-

Cross-Currency Interest Rate Swaps:

- What it is: A combination of an interest rate swap and a currency swap. It involves exchanging both principal and interest payments in different currencies, where the interest payments are based on different interest rate benchmarks.

-

Purpose:

- Complex Risk Management: This type of swap is used for more complex risk management scenarios, such as hedging both interest rate risk and currency risk simultaneously.

-

Example:

- Company A (US) exchanges $10 million with Company B (Eurozone) for €9 million.

- Company A pays Company B a floating rate based on EURIBOR on the €9 million.

- Company B pays Company A a fixed rate on the $10 million.

- At maturity, the principal amounts are exchanged back.

Valuation of Swaps (Simplified):

- Swaps are typically valued as the present value of the expected future cash flows. This involves discounting the expected net payments using appropriate discount rates (based on the yield curve for each currency).

Why Use Swaps?

- Flexibility: Swaps can be customized to meet specific needs.

- Risk Management: Swaps are powerful tools for managing interest rate risk and currency risk.

- Cost Efficiency: Swaps can sometimes provide more cost-effective access to financing than direct borrowing.

- Speculation: Swaps can be used to speculate on the direction of interest rates or exchange rates.

No Comments