Understanding Credit Default Swaps (CDS)

Insurance Against Default

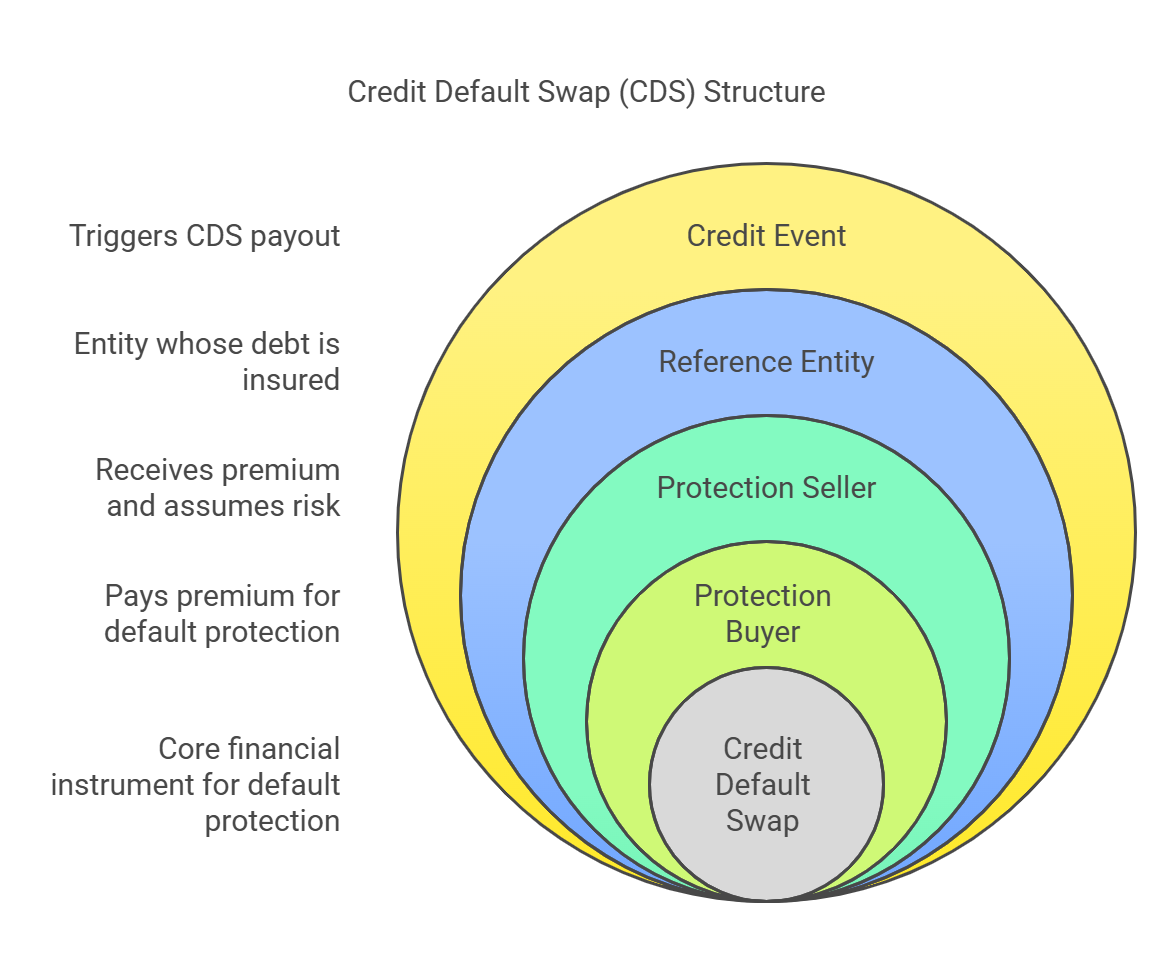

A Credit Default Swap (CDS) is essentially an insurance policy against the risk of a company or sovereign entity (the reference entity) defaulting on its debt. One party (the protection buyer) pays a premium to another party (the protection seller) in exchange for protection against a default event.

Key Concepts:

- Reference Entity: The company, sovereign, or other entity whose debt is being insured.

- Reference Obligation: The specific bond or loan of the reference entity that is covered by the CDS.

- Protection Buyer: The party that pays a premium (the CDS spread) to receive protection against default. They are hedging against the risk of the reference entity defaulting.

- Protection Seller: The party that receives the premium (the CDS spread) and agrees to pay the protection buyer if a default event occurs. They are taking on the credit risk of the reference entity in exchange for the premium.

- CDS Spread: The annual premium paid by the protection buyer to the protection seller, expressed as a percentage of the notional principal. This is the "price" of the CDS.

- Notional Principal: The reference amount used to calculate the payout in the event of a default.

- Credit Event: An event that triggers a payout under the CDS, such as bankruptcy, failure to pay, or restructuring of the debt.

-

Settlement: How the CDS is settled after a credit event:

- Physical Settlement: The protection buyer delivers the defaulted bond to the protection seller and receives the notional principal in return.

- Cash Settlement: The protection seller pays the protection buyer the difference between the notional principal and the market value of the defaulted bond.

How a CDS Works (Simplified):

- Protection Buyer Pays Premium: The protection buyer makes periodic payments (the CDS spread) to the protection seller.

- No Default: If the reference entity does not default, the protection buyer continues to pay the premium until the CDS contract expires.

- Default Event: If a credit event occurs, the protection seller pays the protection buyer the notional principal (in the case of physical settlement) or the difference between the notional principal and the market value of the defaulted bond (in the case of cash settlement).

- CDS Contract Terminates: After the settlement, the CDS contract terminates.

Valuation of CDS:

The valuation of a CDS is based on the probability of default of the reference entity. It involves calculating the present value of the expected premium payments and the expected payout in the event of default.

Simplified Valuation Approach:

- Estimate the Probability of Default: This is the most challenging part of the valuation process. It involves analyzing the creditworthiness of the reference entity and using credit risk models to estimate the probability of default over the life of the CDS. Credit ratings from agencies like Moody's, S&P, and Fitch are often used as a starting point.

- Estimate the Recovery Rate: This is the percentage of the notional principal that is expected to be recovered in the event of default.

- Calculate the Expected Payout: This is the notional principal multiplied by (1 - Recovery Rate) multiplied by the probability of default.

- Calculate the Present Value of Expected Cash Flows: Discount the expected premium payments and the expected payout using appropriate discount rates. The discount rates should reflect the risk-free rate plus a credit spread that reflects the riskiness of the CDS.

Formula (Simplified CDS Spread Calculation):

CDS Spread ≈ (Probability of Default * (1 - Recovery Rate)) / (1 + Discount Rate)

Important Considerations:

- Counterparty Risk: The protection buyer faces the risk that the protection seller will be unable to make the payout in the event of default. This is known as counterparty risk.

- Liquidity: The CDS market can be illiquid, especially for less creditworthy reference entities.

- Model Risk: The valuation of CDS relies on credit risk models that make simplifying assumptions. The accuracy of the valuation depends on the accuracy of the model.

- "Naked" CDS: It's possible to buy a CDS without owning the underlying debt. This is considered a speculative position.

Why Use CDS?

- Hedging Credit Risk: CDS are primarily used to hedge against the risk of default.

- Speculation: Traders can use CDS to speculate on the creditworthiness of a reference entity.

- Arbitrage: Traders can use CDS to exploit differences in pricing between the CDS market and the bond market.

No Comments