Estimation of a Multivariate Model

Estimating multivariate GARCH (MGARCH) models involves determining parameter values that best fit the observed data while satisfying constraints such as the positive definiteness of the conditional covariance matrix. This is typically achieved using Maximum Likelihood Estimation (MLE).

Maximum Likelihood Estimation (MLE) in a Multivariate Setting

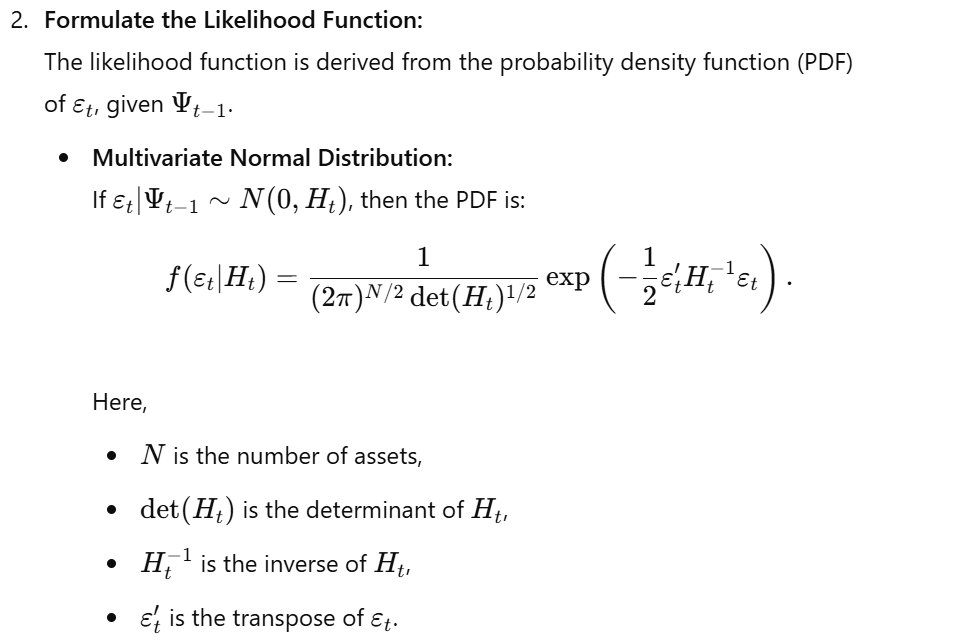

MLE is a statistical method that estimates the parameters of a probability distribution by maximizing a likelihood function. In MGARCH models, the likelihood function represents the probability of observing the given data, conditional on a set of parameters and a specific model specification.

Steps in Estimating MGARCH Models Using MLE

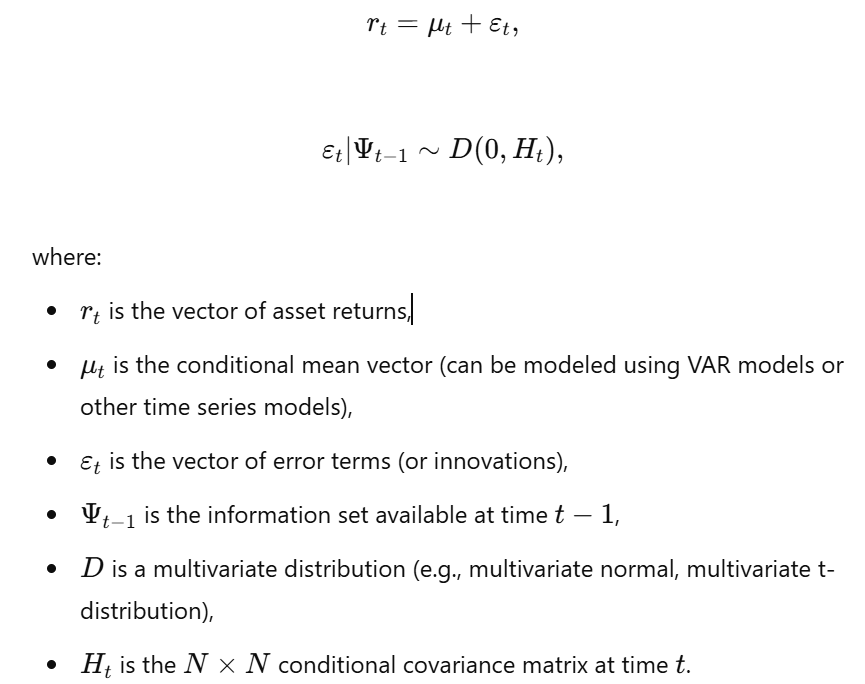

Specify the Model:

Choose the appropriate MGARCH model (e.g., VECH, Diagonal VECH, BEKK) and specify the error term distribution (e.g., multivariate normal, multivariate t-distribution). The general MGARCH model is:

Conclusion

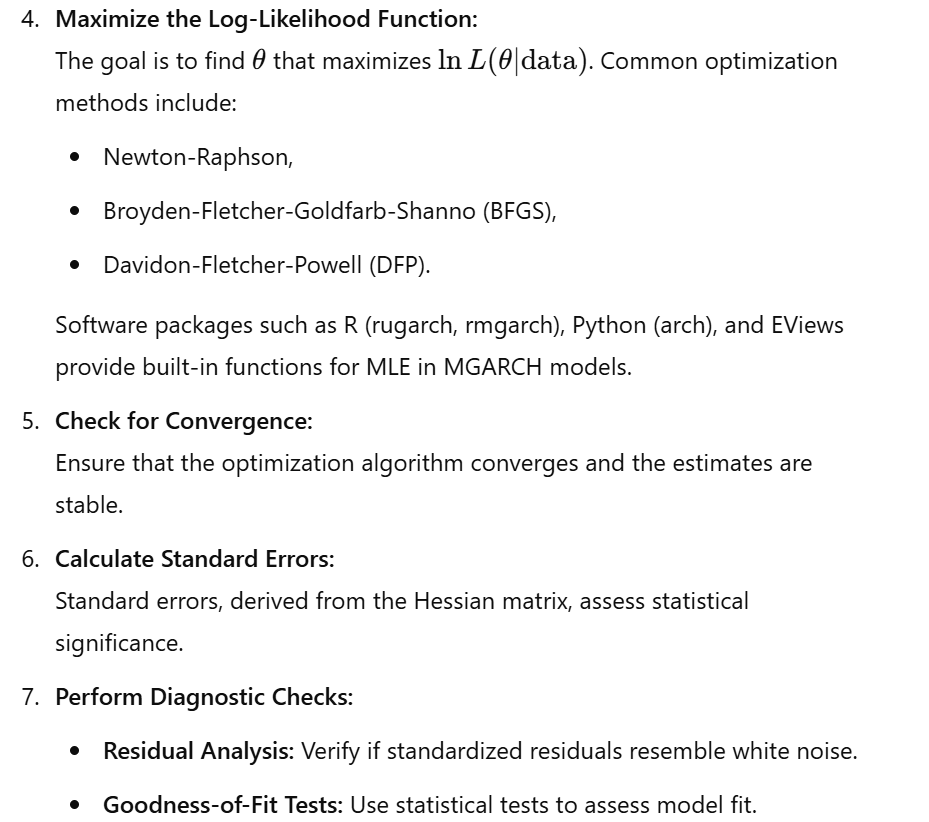

Estimating MGARCH models involves specifying the model, deriving the likelihood function, and maximizing the log-likelihood function. MLE is the primary estimation method, with optimization algorithms ensuring reliable results. Statistical software such as R, Python, and EViews facilitate estimation, but model specification, distributional assumptions, and computational feasibility must be carefully considered. Balancing model flexibility and computational efficiency is crucial in practical applications.

No Comments