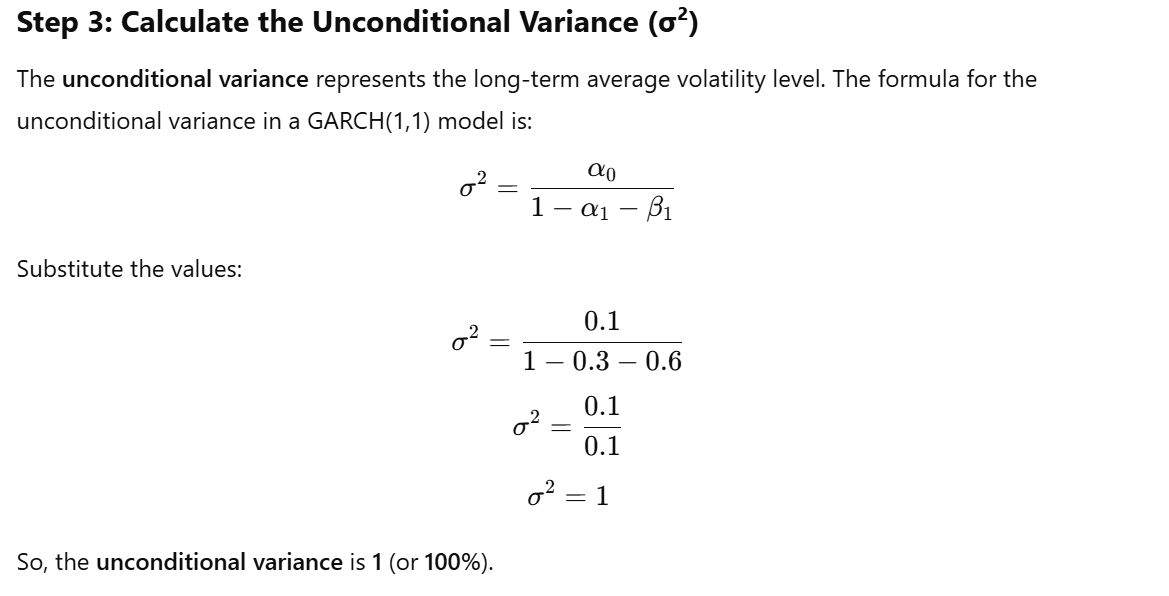

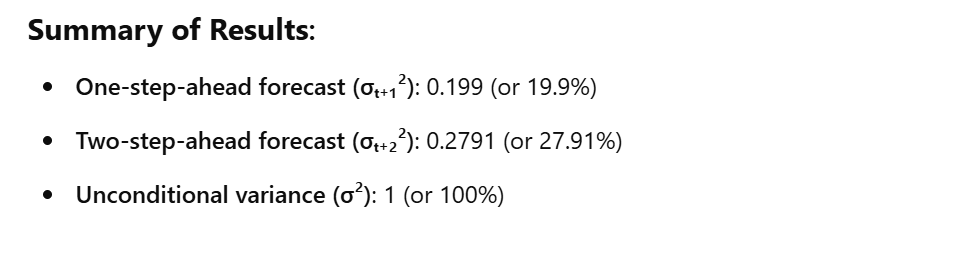

Numericals

These calculations give us a basic understanding of how volatility is forecasted using a GARCH(1,1) model based on some initial data. In practice, this process would be repeated with real financial time series data, and you would typically use software to perform these calculations more efficiently.

No Comments