Granger Causality Test (GCT)

The Granger Causality Test (GCT), developed by Clive Granger, is a statistical hypothesis test used to determine whether one time series can predict another. The fundamental idea is that if a time series X "Granger causes" another time series Y, then past values of X should contain information that improves the forecasting of Y beyond what is possible using only past values of Y.

Introduction to GCT

-

Definition: A time series X is said to Granger cause another time series Y if past values of X significantly enhance the prediction of Y when compared to a model using only past values of Y. Importantly, Granger causality refers to predictive capability rather than true causality in a philosophical sense.

-

Testing Framework: The GCT is commonly conducted within a Vector Autoregressive (VAR) model framework.

-

Basic Concept: If adding lagged values of X to a regression of Y improves the model's predictive accuracy, then X is said to Granger cause Y.

Understanding GCT in Depth

-

Predictive Nature: Granger causality deals with predictive relationships, not direct causal mechanisms. If X Granger causes Y, it means X helps in forecasting Y. However, an unobserved third variable Z may be responsible for changes in both X and Y, leading to a spurious causality result.

-

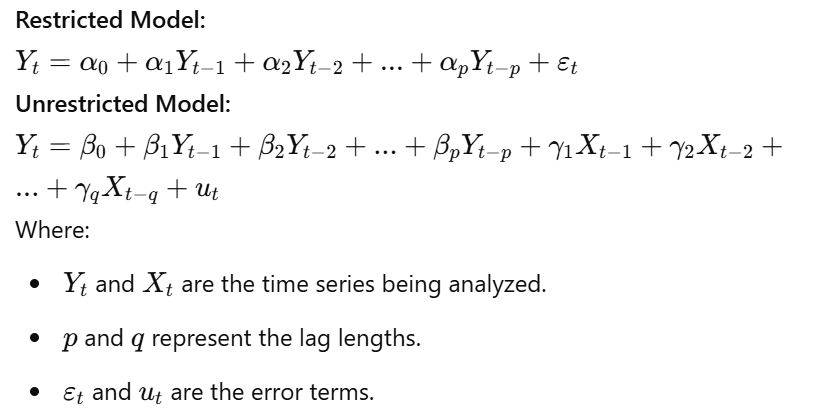

VAR Model Framework: The test typically operates within a VAR model, estimating two equations:

-

Null Hypothesis: The null hypothesis states that X does not Granger cause Y, meaning that all coefficients of lagged values of X in the unrestricted model are zero:

-

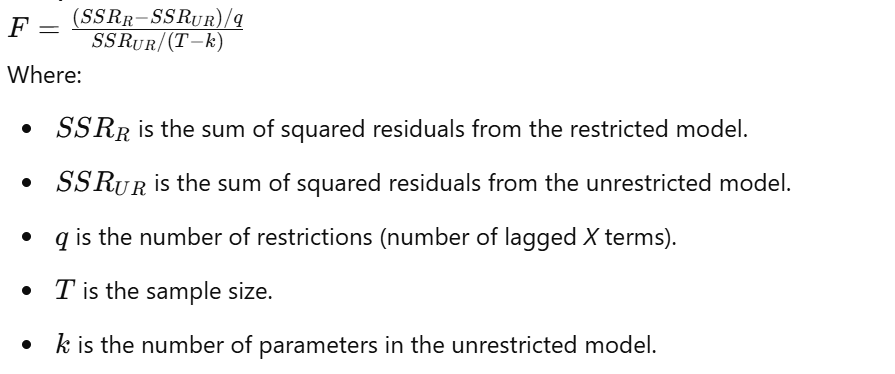

Test Statistic: The GCT uses an F-statistic or Wald statistic to measure the improvement in predictive power when lagged values of X are included.

Key Considerations in GCT

- Lag Order Selection: The choice of lag length (p and q) is crucial. Using too few lags can overlook causality, while too many can lead to overfitting. Information criteria such as AIC, BIC, and HQIC help determine optimal lag selection.

- Stationarity: GCT assumes stationary time series. If the data are non-stationary, differencing or transformations may be necessary, though these can remove long-term relationships.

- Spurious Causality: Granger causality does not imply true causation. A common external factor might drive both X and Y, creating misleading results.

- Omitted Variables: The test only considers variables included in the model. Excluding important factors can yield incorrect conclusions.

- Linearity Assumption: GCT assumes a linear relationship. If the actual relationship is nonlinear, alternative methods may be needed.

- Sample Sensitivity: Results can vary based on the time frame analyzed.

- Direction of Causality: The test can indicate unidirectional (X causes Y) or bidirectional causality (X causes Y and Y causes X). Both directions should be examined.

- Significance Level: Selecting an appropriate significance level is vital. A lower alpha value reduces Type I errors but increases Type II errors, while a higher alpha does the opposite.

Hypothesis Testing Procedure

- Select Lag Orders: Determine optimal lag lengths (p and q) for the VAR model using statistical criteria.

- Estimate the Restricted Model: Run a regression of Y on its own lagged values.

- Estimate the Unrestricted Model: Include lagged values of X in the regression.

- Compute the Test Statistic: The F-statistic is calculated as:

- Compare with Critical Value: Retrieve the critical value from the F-distribution based on degrees of freedom.

- Interpret the Results: If the F-statistic exceeds the critical value, reject the null hypothesis, concluding that X Granger causes Y.

- Robustness Check: Test robustness by altering lag lengths and model assumptions.

Software Implementation

Several statistical tools support the GCT, including:

-

Python:

statsmodels.tsa.stattools.grangercausalitytests() -

R:

grangertest()in thelmtestpackage - EViews: Built-in Granger causality test function

Conclusion

The Granger causality test is a powerful tool for determining whether one time series helps predict another. However, careful consideration is necessary regarding lag selection, stationarity, and potential spurious causality. While GCT provides valuable insights, it should not be mistaken for establishing true causation. Proper interpretation and supplementary analysis are crucial for drawing meaningful conclusions.

No Comments